News over the last 3 months paints a picture of a struggling economy. Revised data indicates the economy stalled in the third quarter of 2024. There was 0% growth, along with downward revisions to previous quarters. This signifies persistent challenges across various sectors, with declines in production and stagnation in services. Private sector output has also dropped, and businesses express concerns about declining demand and rising costs. While inflation has cooled somewhat, it remains a concern, and the labour market, though still tight, shows signs of weakening. Overall, the UK economy faces significant headwinds as it approaches the end of 2024.

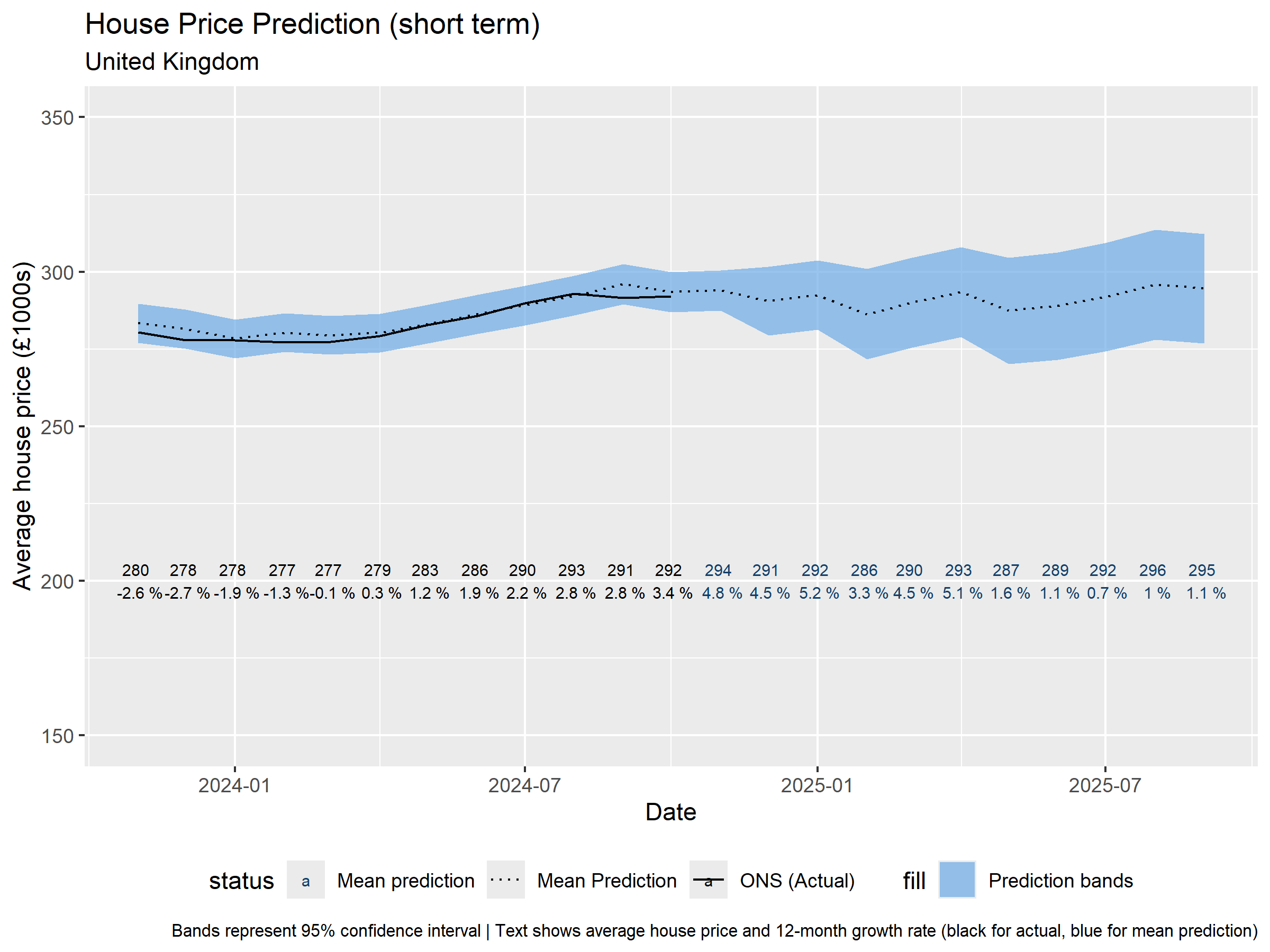

Short-term Forecast (UK)

Early in the forecast (around Q1–Q2 2024), prices dip slightly below £280k, with negative year-on-year growth rates (−2% to −3%). From mid-2024 onward, the model suggests a rebound above £290k, and year-on-year growth turns positive (reaching 4–5% at its peak).

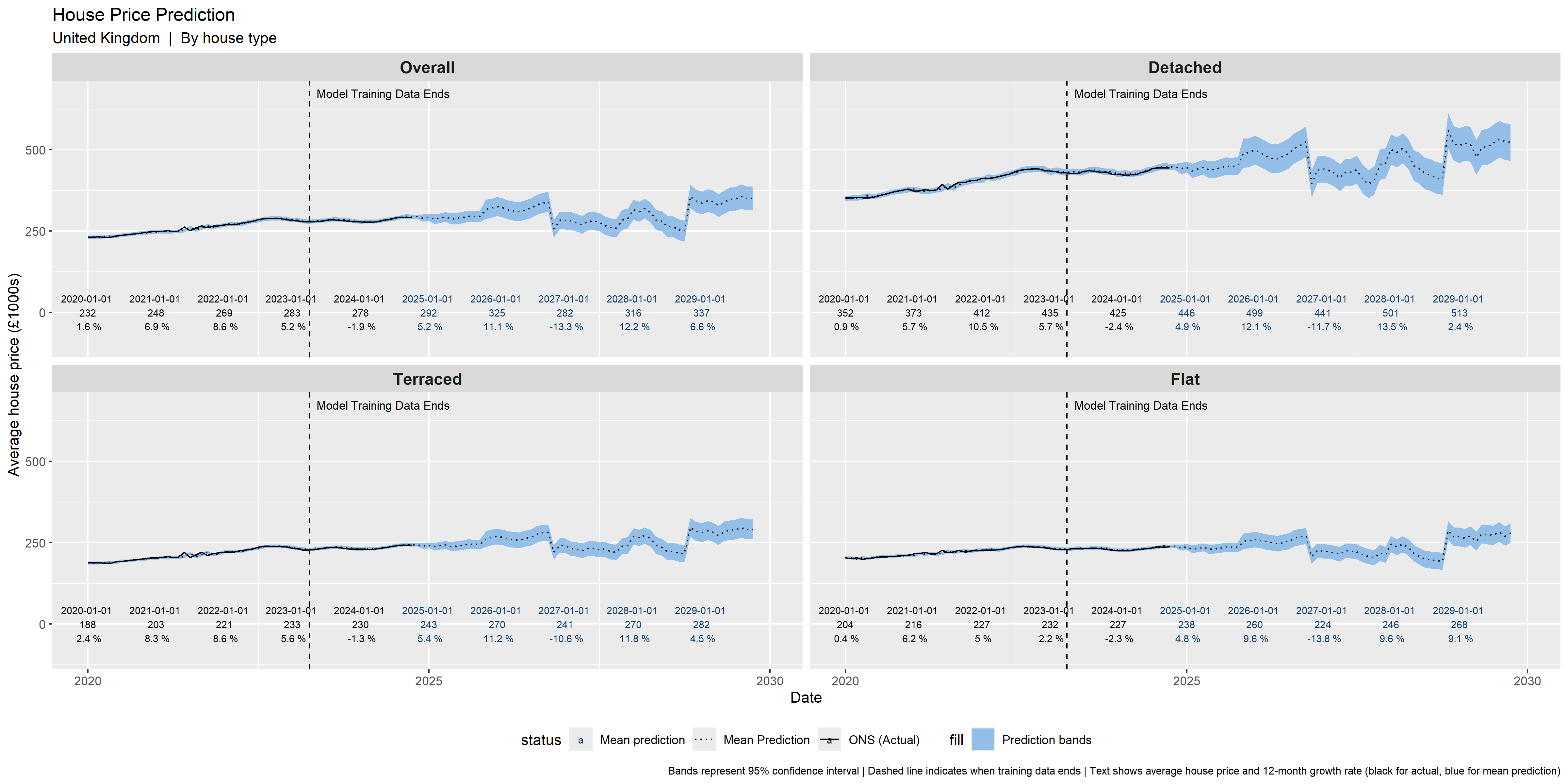

National Overview (UK)

Our national-level model suggests a modest softening for the remainder of 2024, followed by a gradual bounce back through mid-2025. By 2026 and beyond, we expect to see mild but steady annual gains. The magnitude of these gains varies by region and property type, reflecting the usual interplay of demand, supply, and local economic factors.

From the aggregated forecasts:

- Near-Term (6 months, by April 2025): A small dip or moderate growth in some areas, typically between -3% and +4%, depending on region.

- Medium-Term (12–24 months, late 2025 to late 2026): A general trend toward recovery, with most areas reverting to modest growth. Some places could see higher growth above 5%, while others remain flat to slightly negative.

- Long-Term (60 months, 2029): More substantial gains are forecast for certain areas, while others lag behind with slower growth.

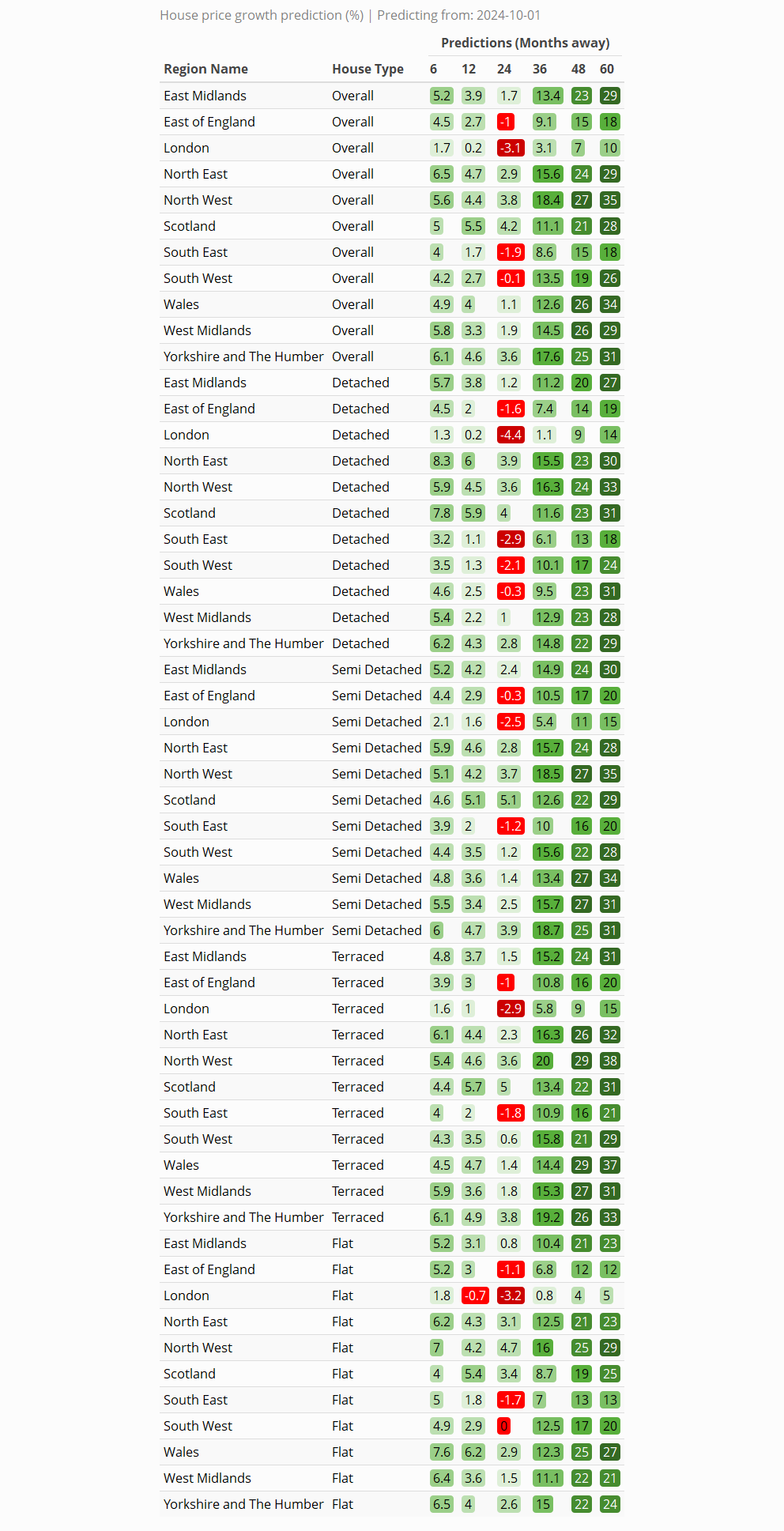

By Region and Property Type

We’ve broken down the forecast by region (England, Wales, Scotland, Northern Ireland) and major property types (Detached, Semi-Detached, Terraced, Flats). Some highlights from the latest tables:

- Detached: Overall expected to see moderate growth, particularly from late 2025 onward. The model suggests that certain areas of Scotland and the North East may outperform, while parts of London could see weaker gains in the near term.

- Semi-Detached: A similar pattern to detached homes, with dips possible in some parts of the East of England but more robust rebounds in Yorkshire and The Humber.

- Terraced: Often more sensitive to changes in affordability, terraced properties could see modest gains in the Midlands and Wales, but might underperform in pricey London boroughs.

- Flats: Flats remain somewhat subdued due to lingering effects of remote work and changed lifestyle demands. That said, pockets in London and major city centres with high demand for smaller units may post decent growth after 2025.

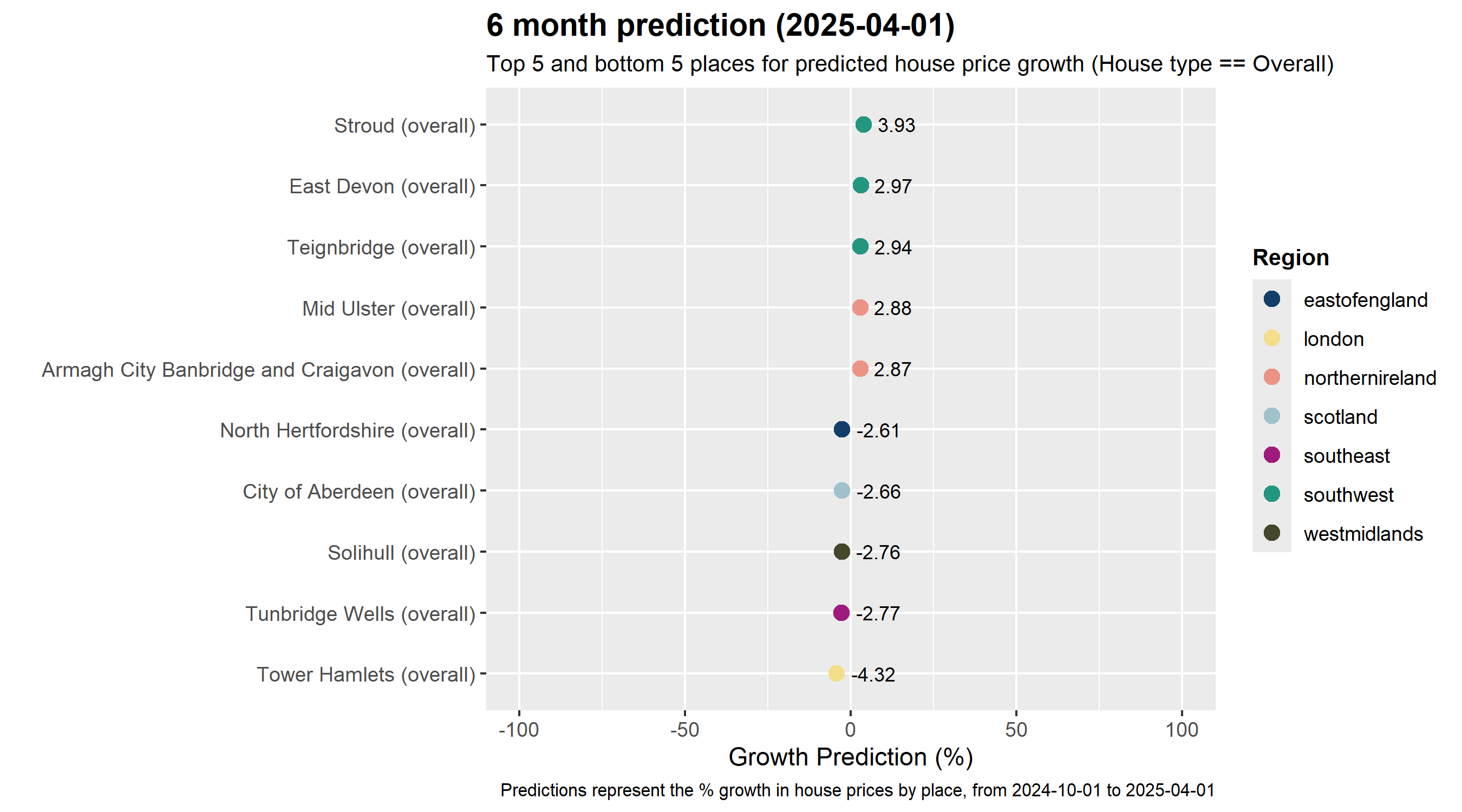

The Winners and Losers

We’ve identified the top 5 and bottom 5 places for predicted house price growth at various time horizons (Overall house type). Here’s a quick glance:

6-Month Prediction (by April 2025)

- Top 5: Stroud, East Devon, Teignbridge, Mid Ulster, and Armagh City Banbridge and Craigavon appear poised for growth between roughly +2.8% and +3.9%.

- Bottom 5: Areas like Tunbridge Wells, Solihull, Tower Hamlets, and parts of the North Hertfordshire region are expected to see slightly negative or flat growth, in the -2.6% to -4.3% range.

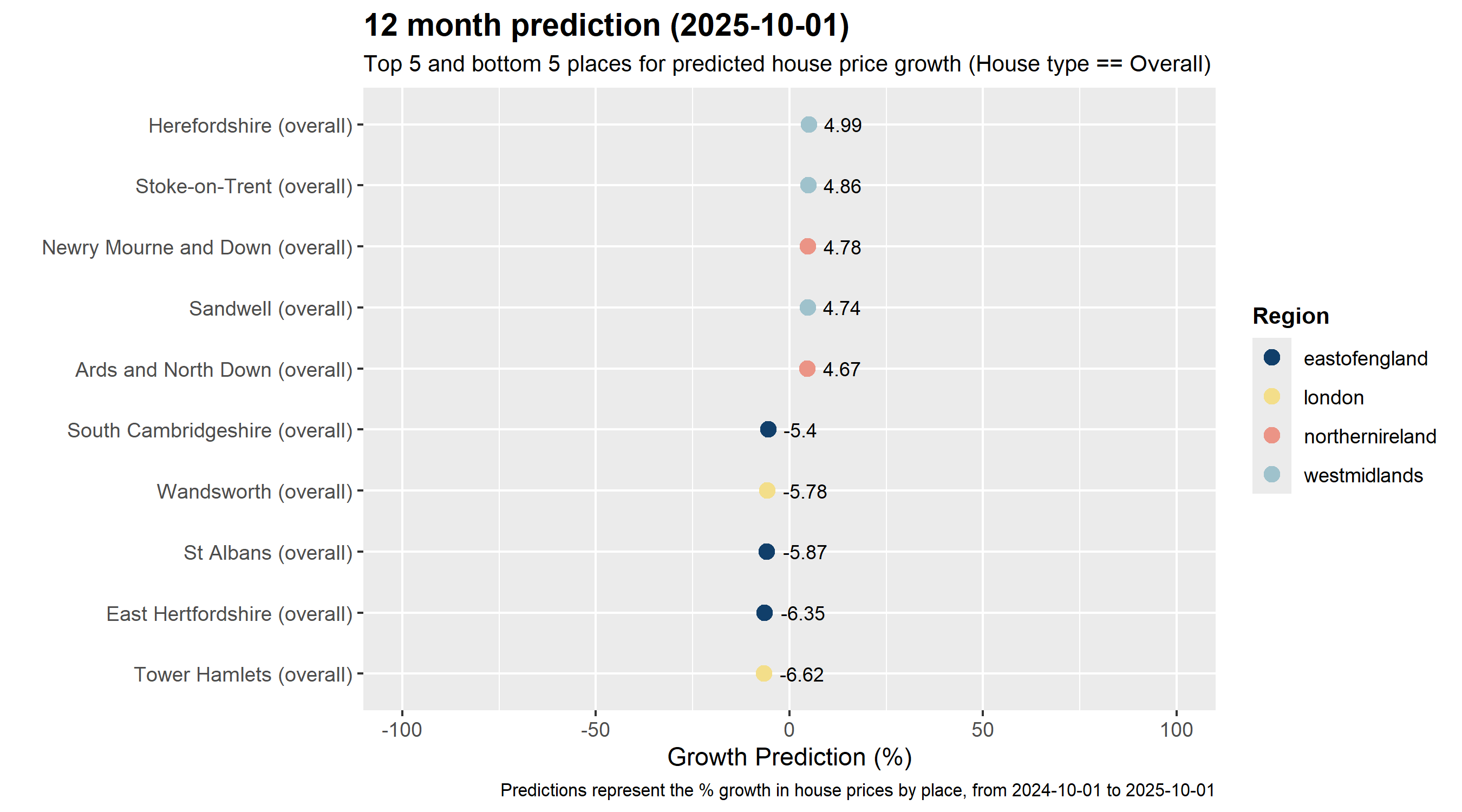

12-Month Prediction (by October 2025)

- Top 5: Herefordshire, Stoke-on-Trent, Newry Mourne and Down, Sandwell, and Ards and North Down could see the highest increases (around +4.7% to +5.0%).

- Bottom 5: Regions like South Cambridgeshire, Wandsworth, St Albans, East Hertfordshire, and Tower Hamlets are more likely to lag (around -5% to -6.6%).

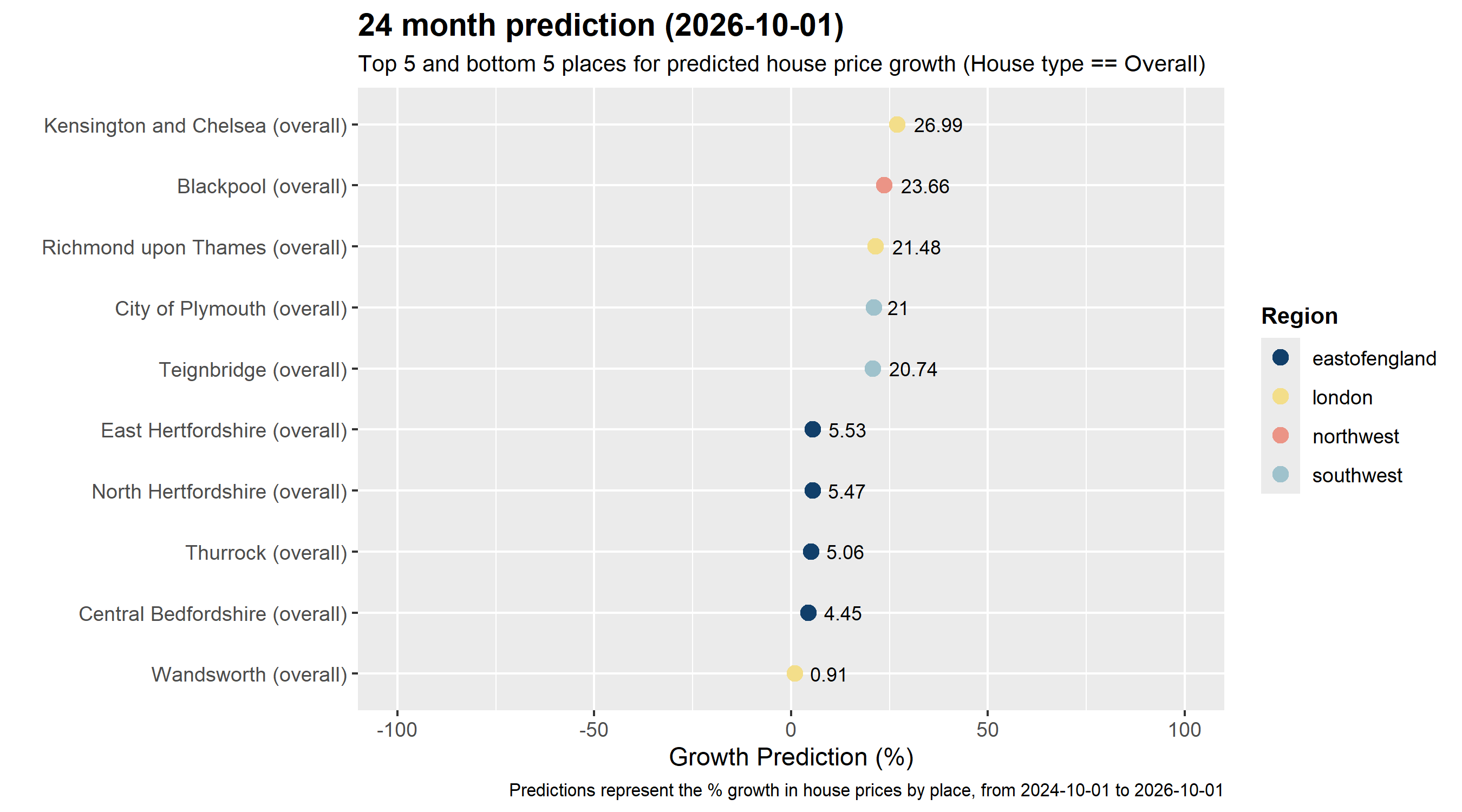

24-Month Prediction (by October 2026)

- Top 5: London borough Kensington and Chelsea leads the pack with nearly +27%, followed by Blackpool, Richmond upon Thames, City of Plymouth, and Teignbridge—ranging from about +20% to +27%.

- Bottom 5: North Hertfordshire, East Hertfordshire, Thurrock, Central Bedfordshire, and Wandsworth appear among those with lower growth (5% or less).

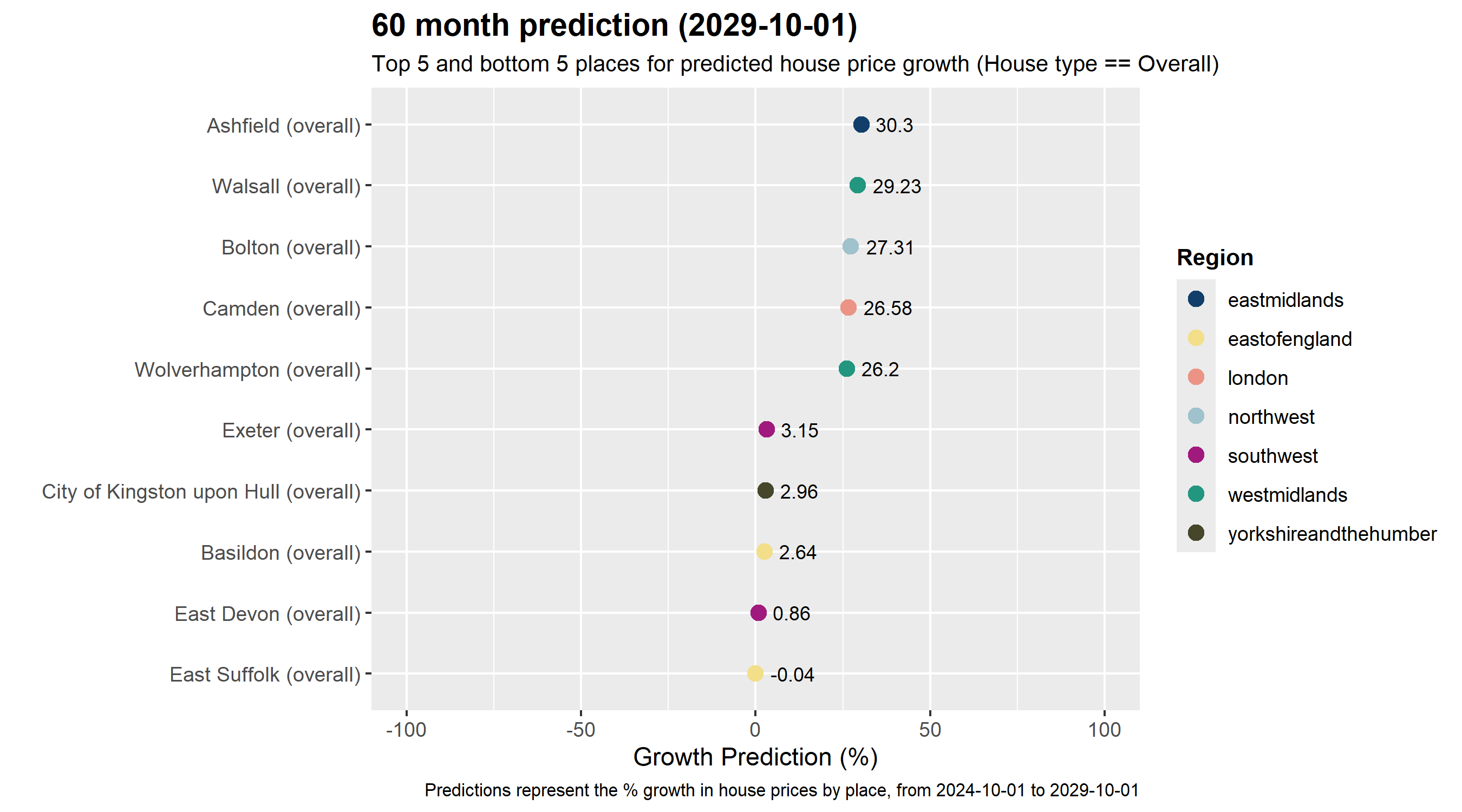

60-Month Prediction (by October 2029)

- Top 5: Forecasts show Ashfield, Walsall, Bolton, Camden, and Wolverhampton potentially jumping by about +26% to +30%.

- Bottom 5: Basildon, East Devon, East Suffolk, City of Kingston upon Hull, and Exeter rank toward the lower end, with growth forecasts hovering around 0% to +3%.

Remember that these “bottom” spots don’t necessarily mean negative growth—some are merely forecast to be outpaced by the stronger-performing regions.

Key Takeaways

- Short term: Patchy performance. Some areas could see small dips, while others eke out moderate gains.

- Mid term: Overall recovery trend, with stronger pockets in certain regions and property types.

- Long term: More robust price appreciation is possible, especially for certain urban areas and commuter regions, though the spread between top- and bottom-performing locales is set to widen.