Economic summary

News

Politics dominated the month. Andy Burnham succeeded Keir Starmer as prime minister on 20 July, the UK’s seventh in a decade, and unsettled the gilt market within hours by promising to use “any flexibility” available within the fiscal rules. The data, though, improved. Inflation eased to 2.6% in the 12 months to June, its lowest since March 2025, as motor fuel prices fell, while monthly GDP grew 0.1% in May after April’s contraction and the flash composite PMI rebounded to 52.1 in July from 49.3, its strongest reading since February. Unemployment held at 4.9% and regular pay growth slowed to 3.4%. The Bank of England’s next rate decision lands on 30 July.

Indicators

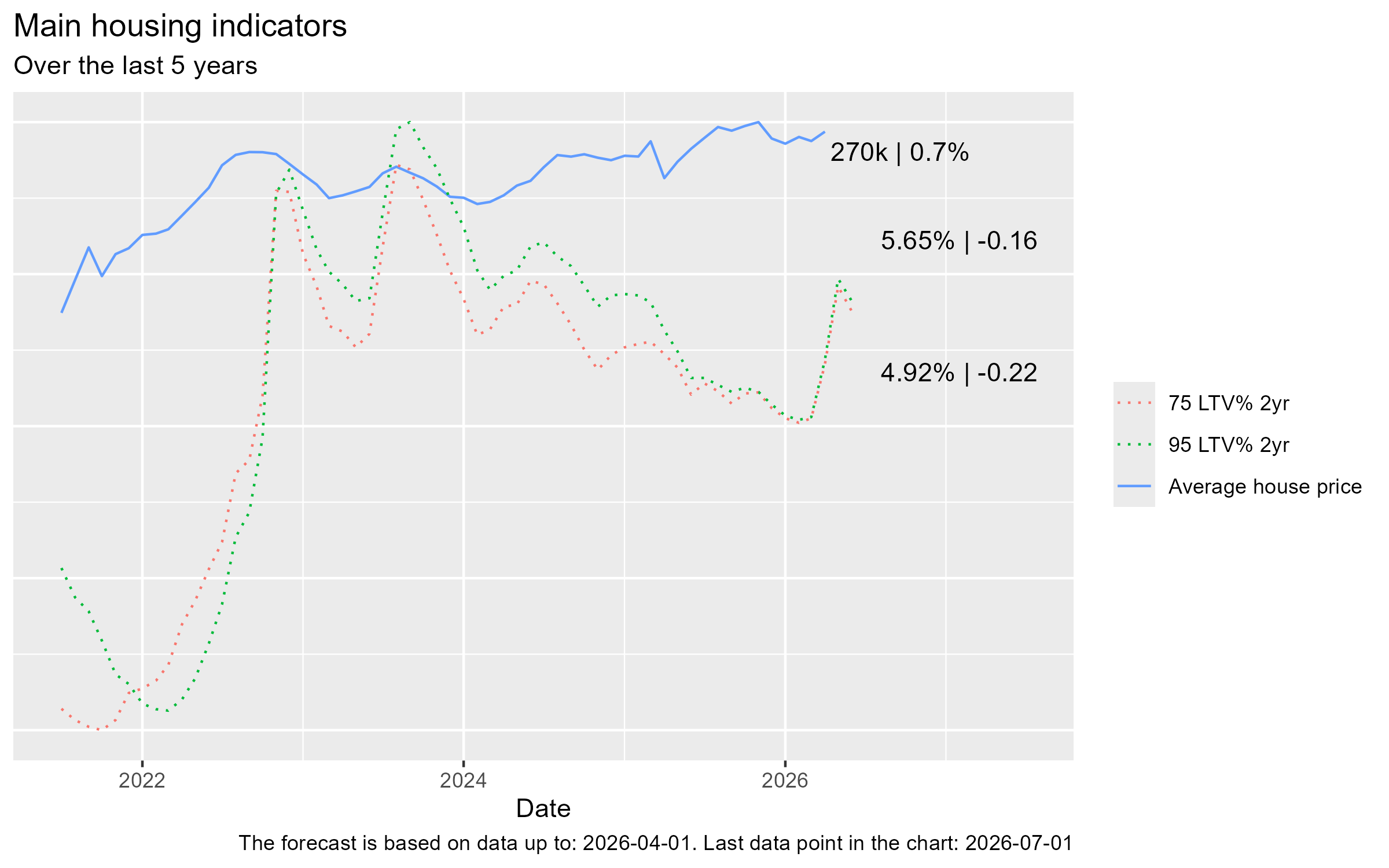

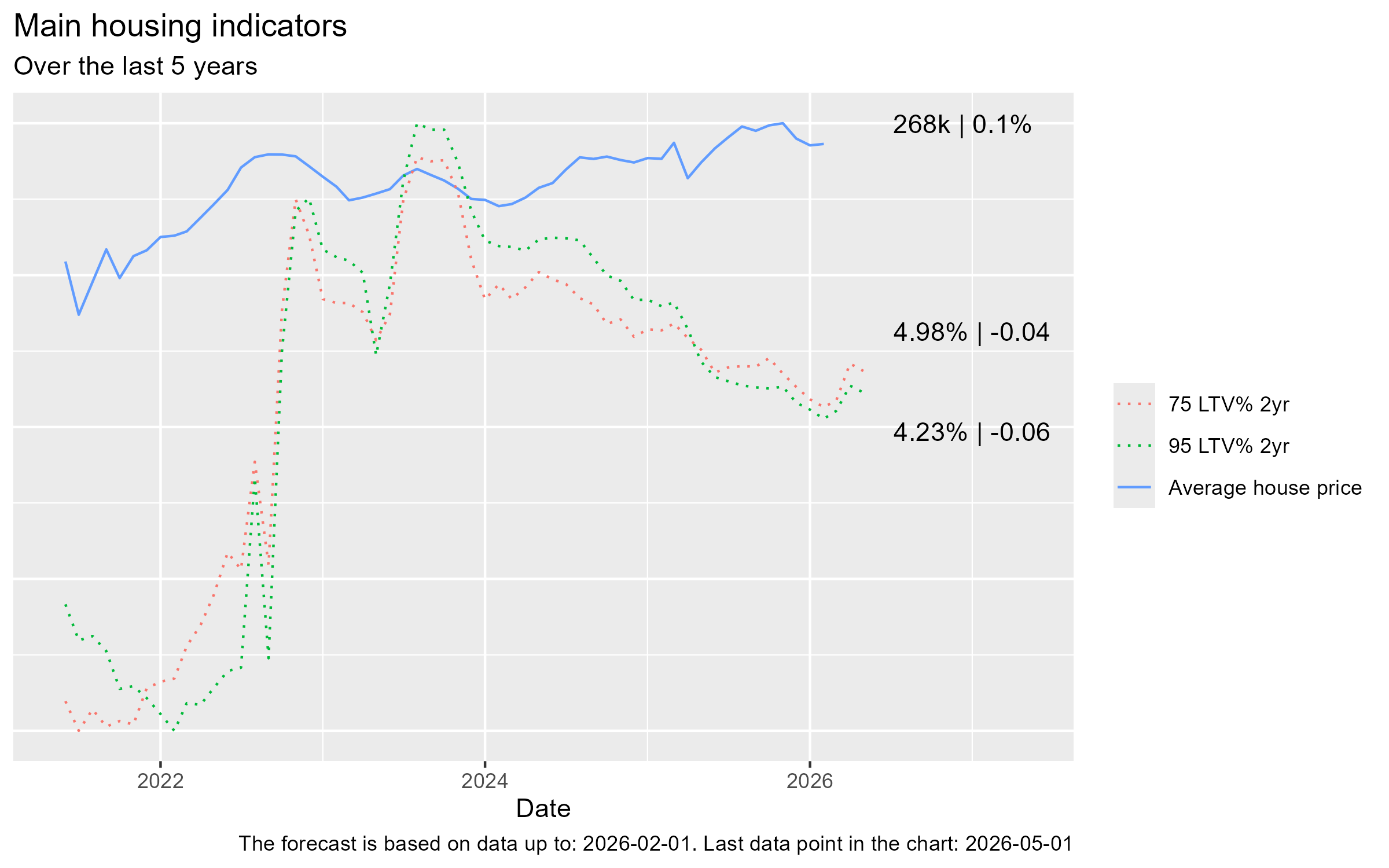

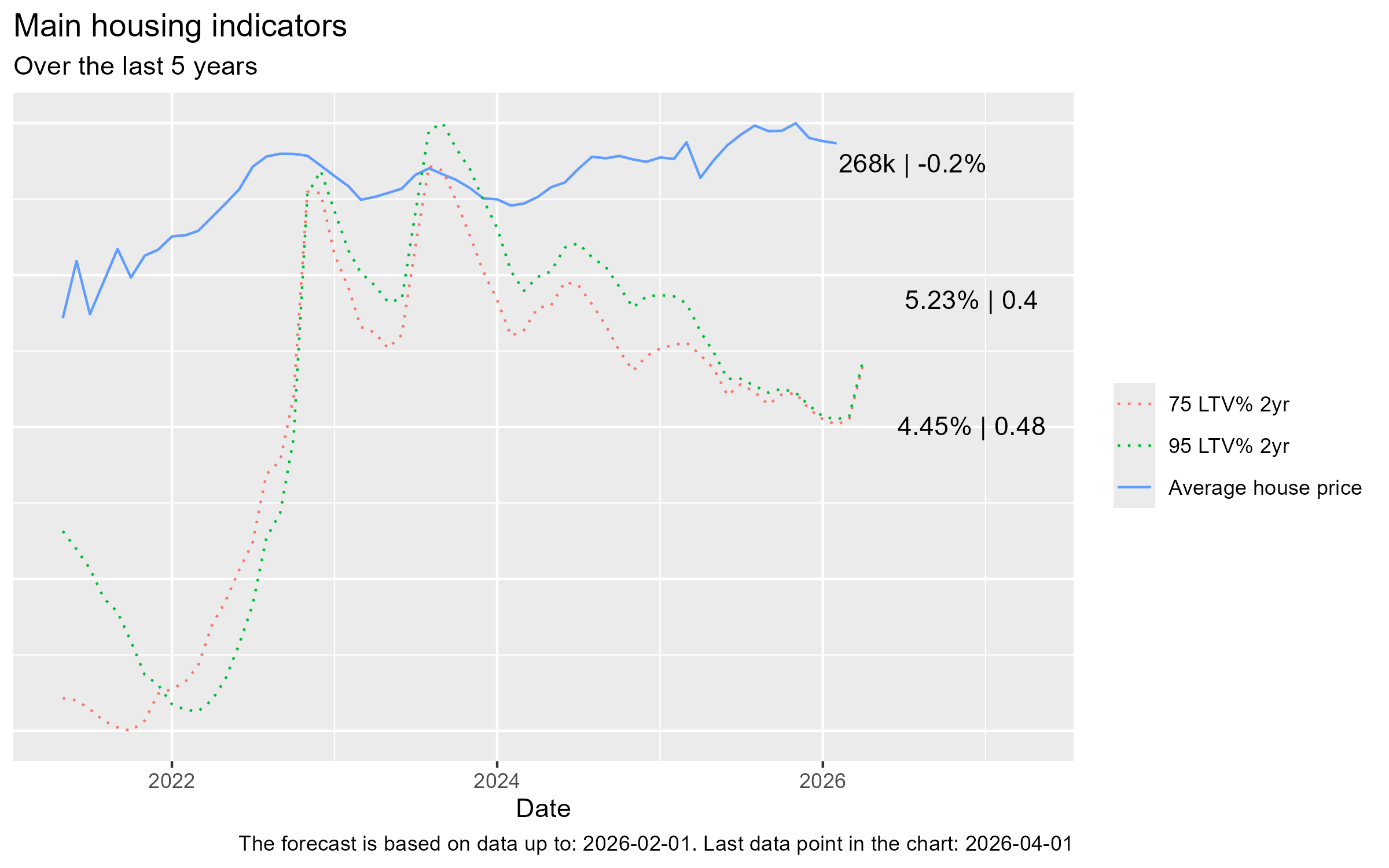

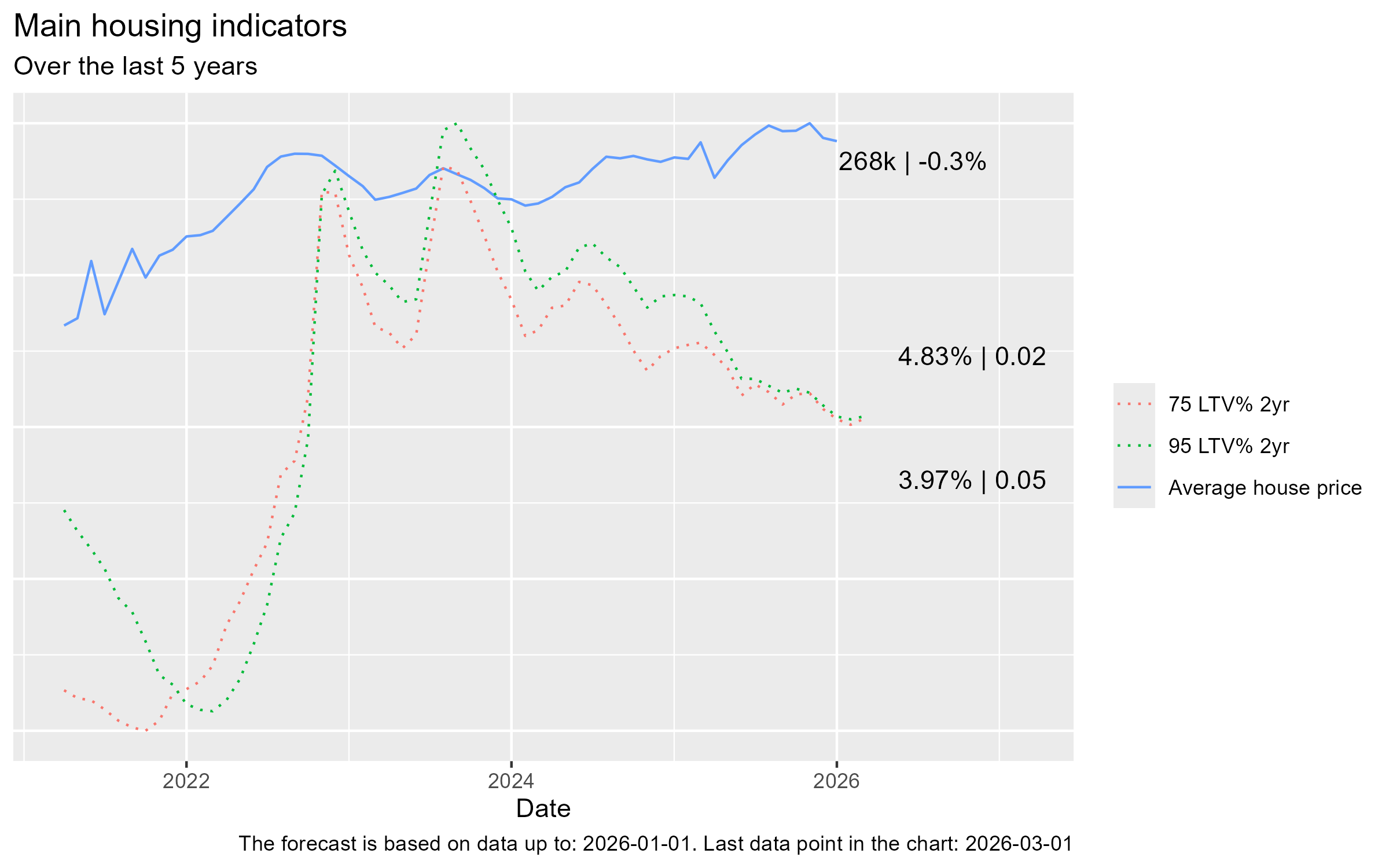

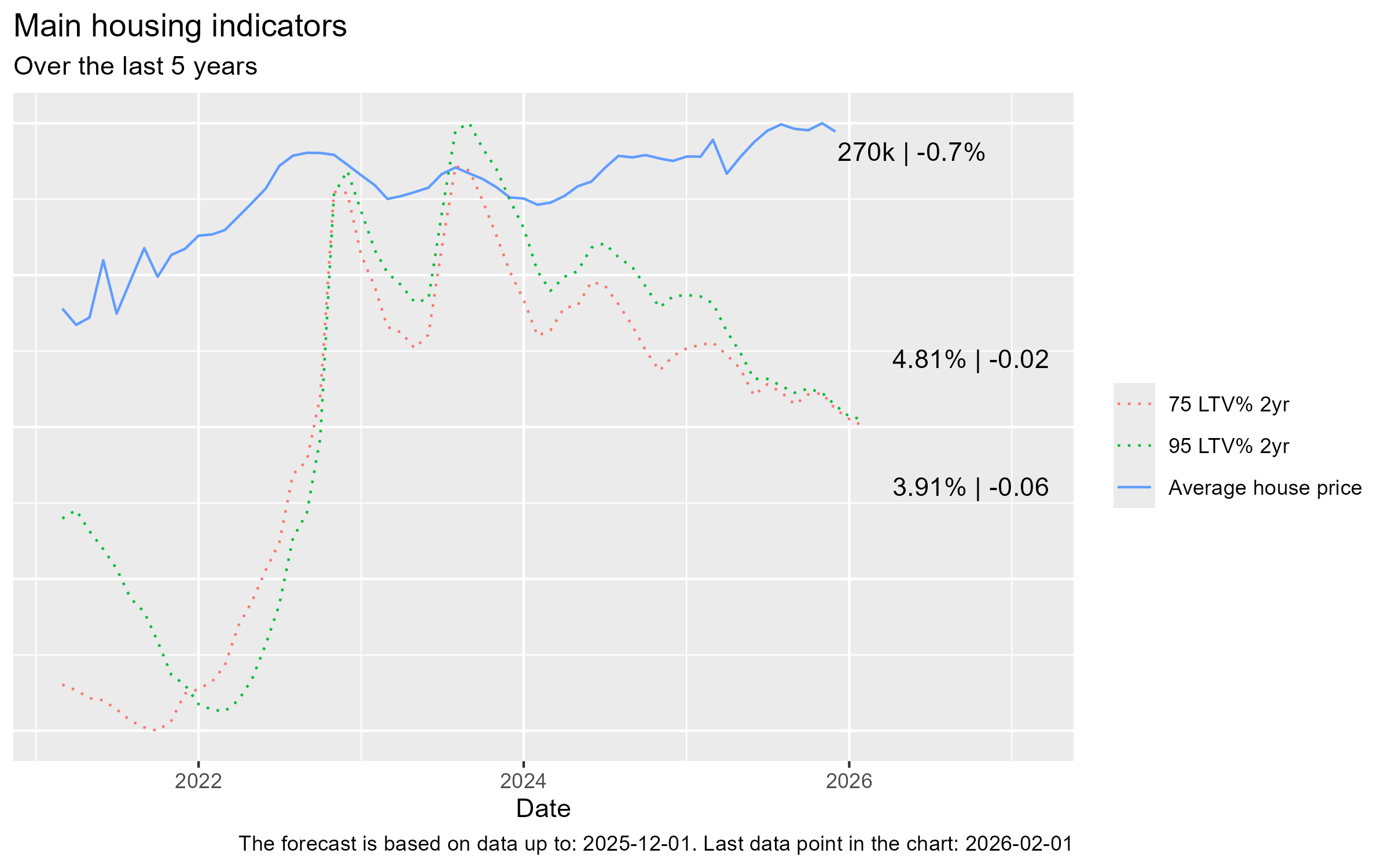

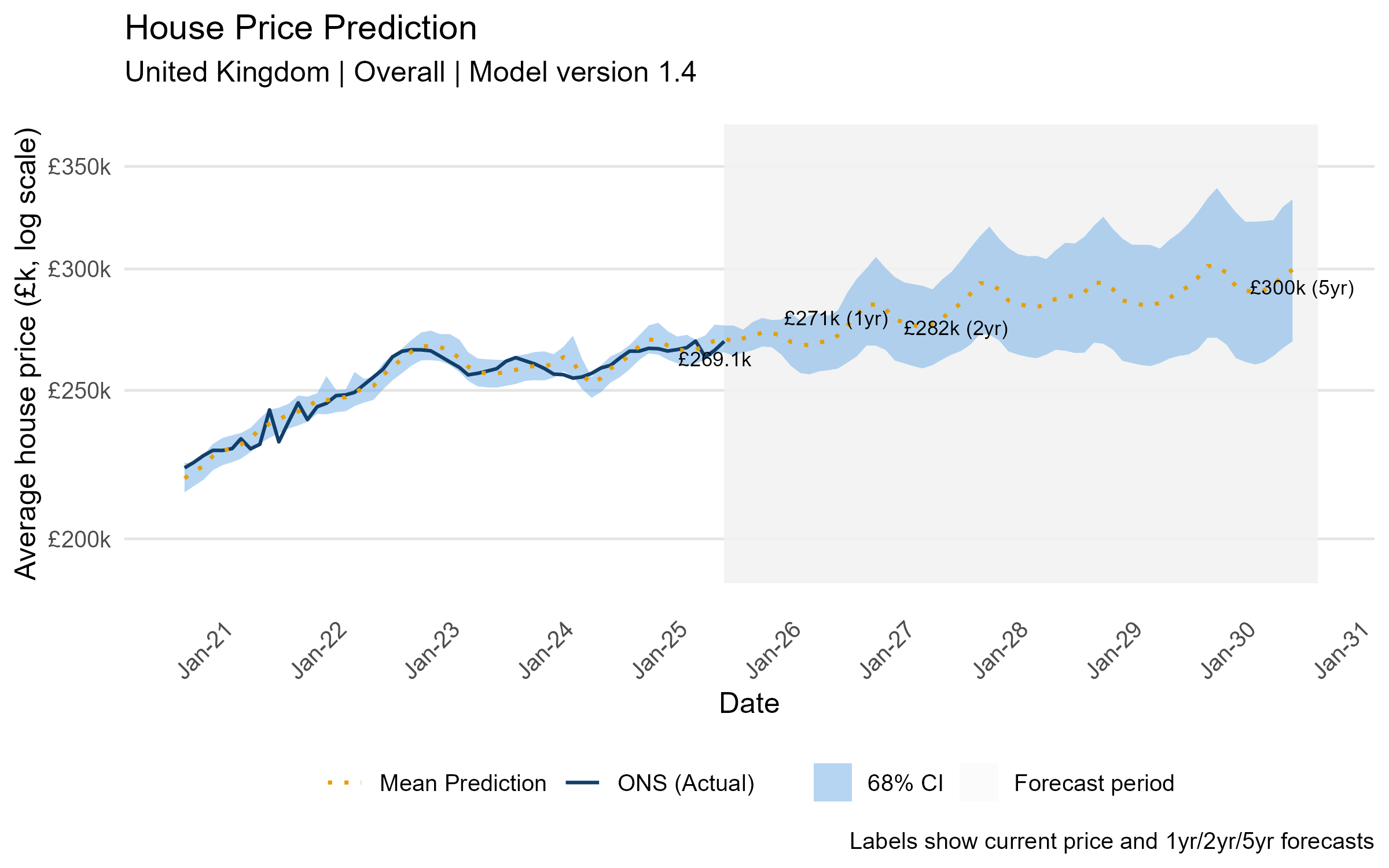

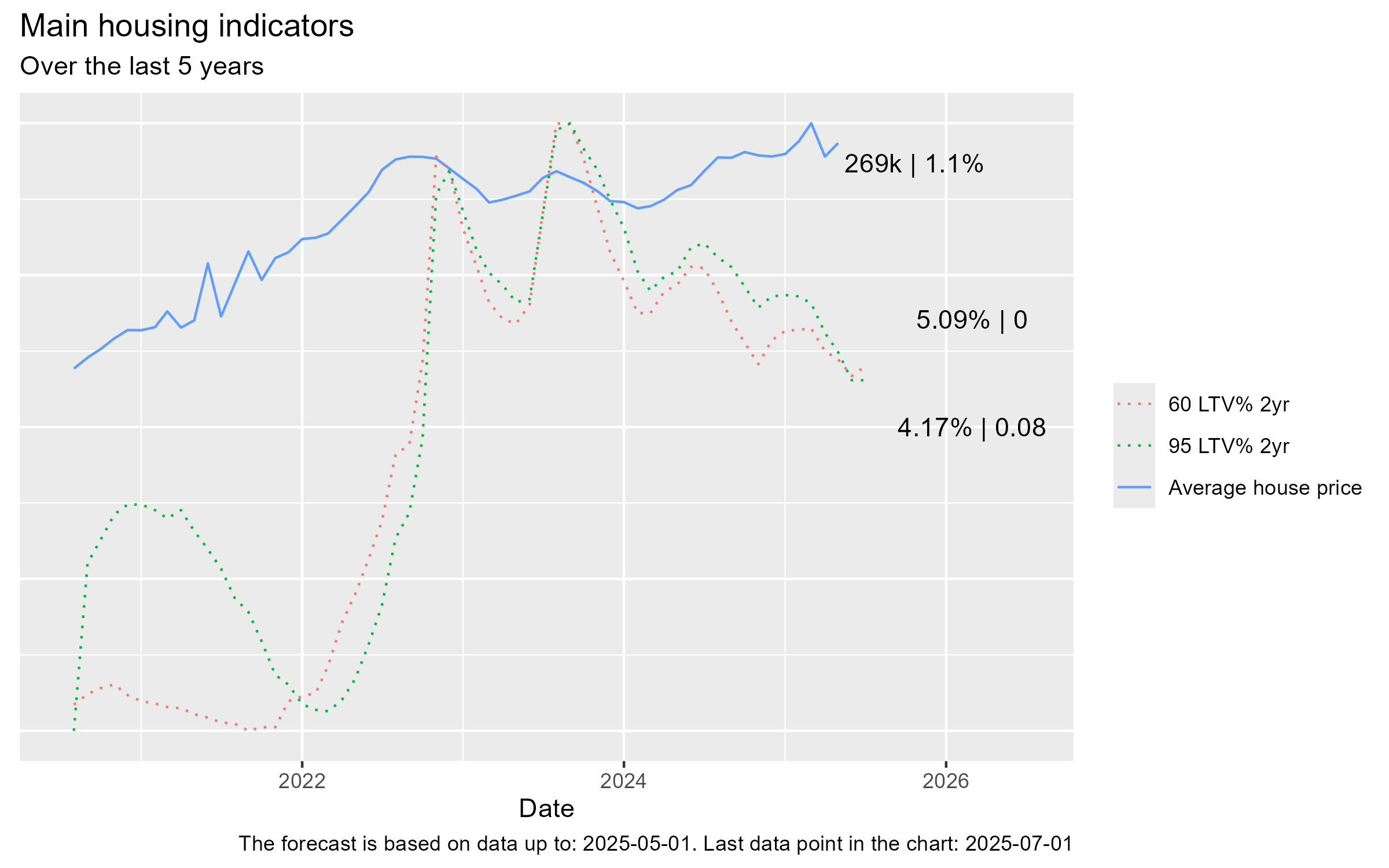

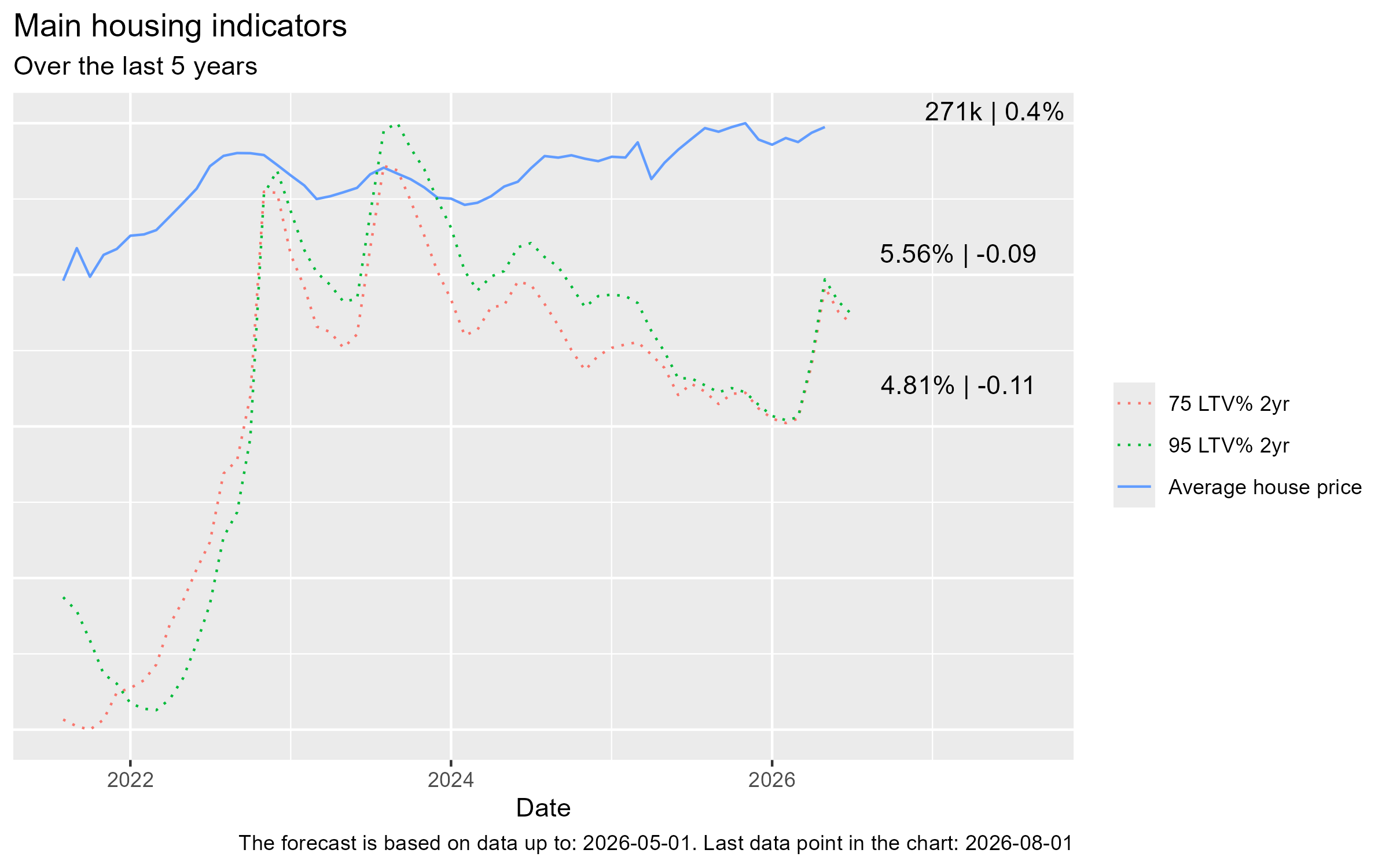

- Average house prices rose to £271k, up 0.4% on the previous month — consistent with the ONS, which put annual UK house price growth at 2.7% in the year to May, down from a revised 3.9% in April as last year’s Stamp Duty base effect washed out

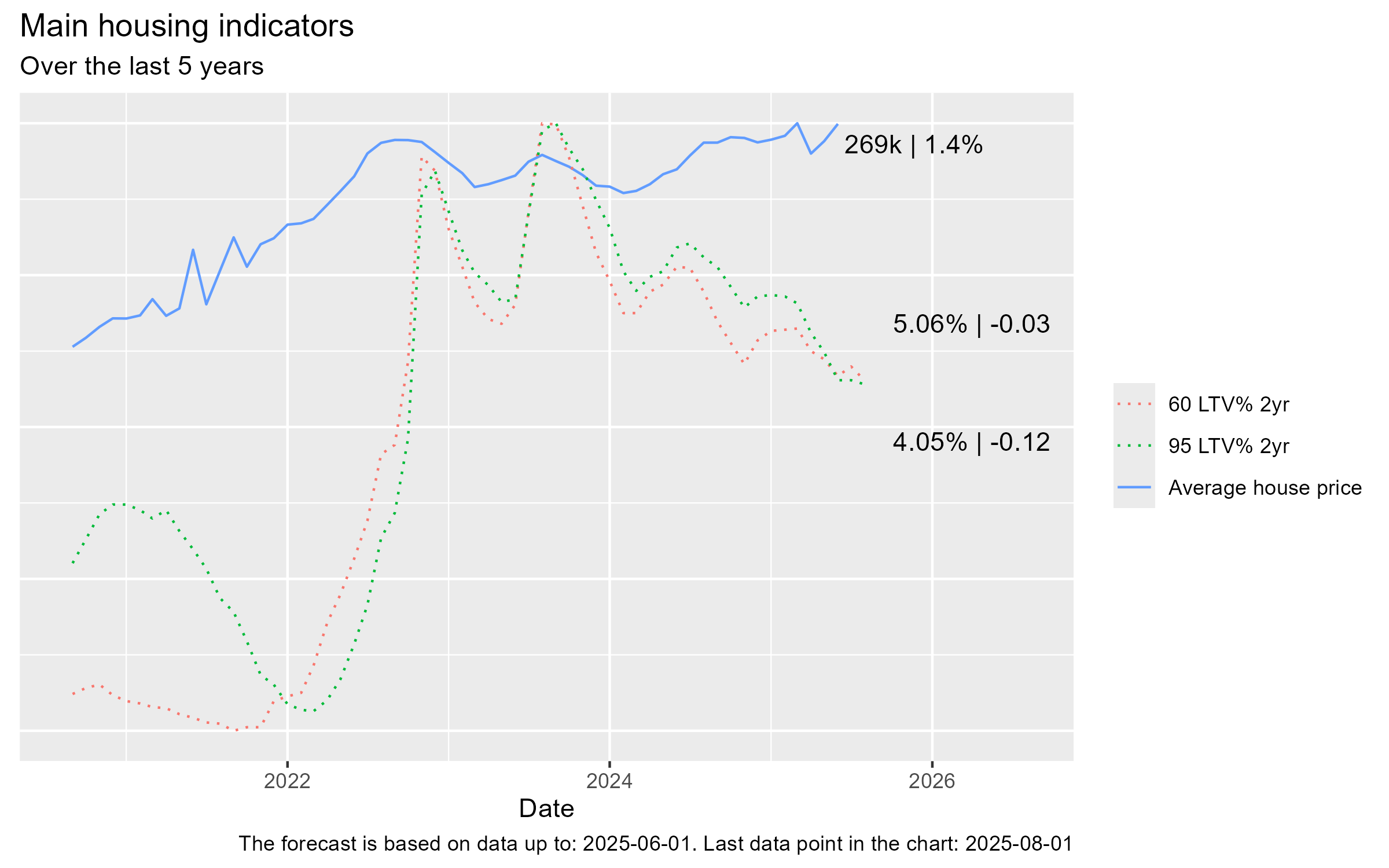

- The average 75% LTV 2-year mortgage rate fell to 4.81% and the 95% LTV 2-year rate to 5.56%, both down around 10 basis points on the month as the energy-driven spike in gilt yields unwound

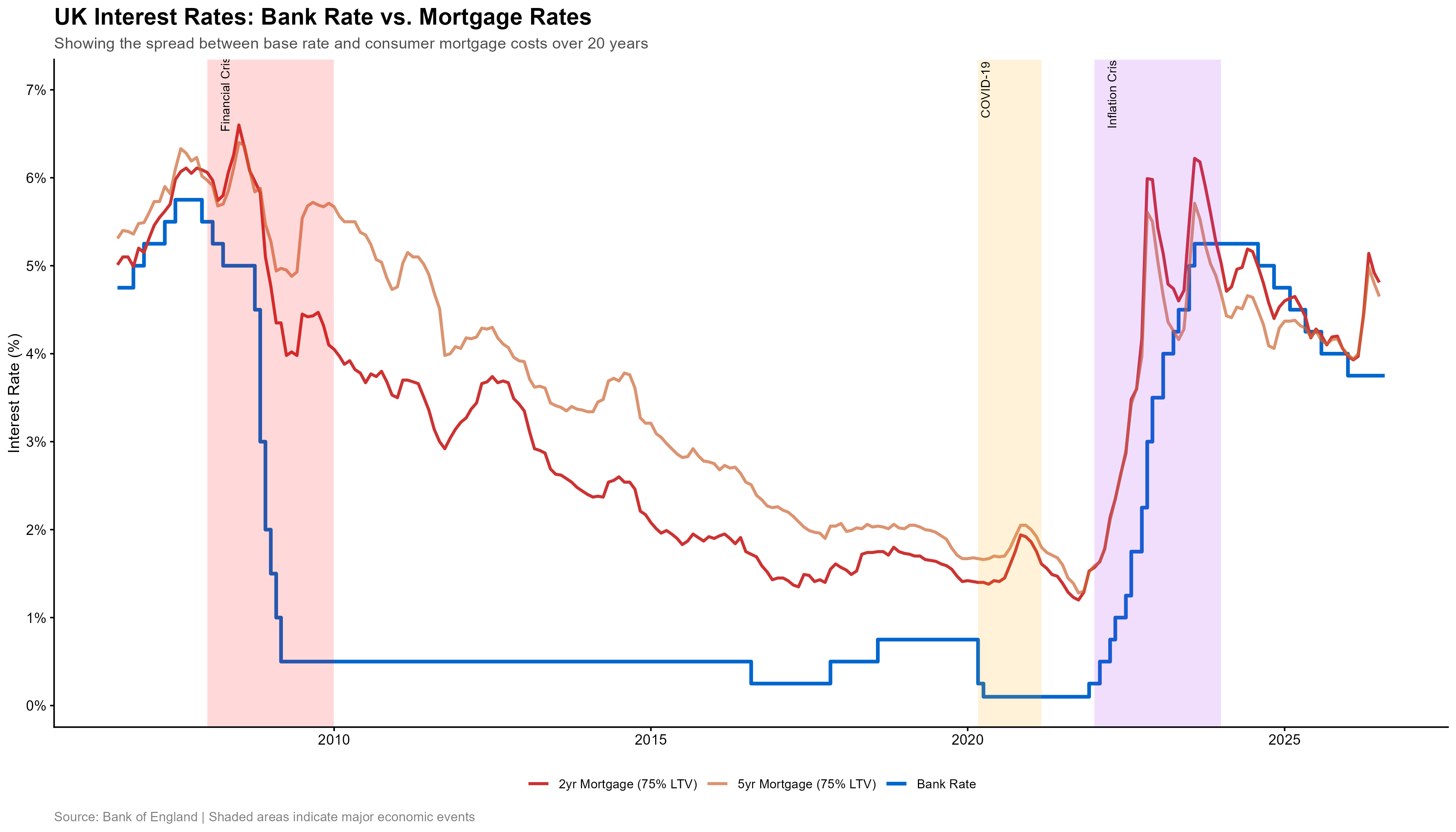

Interest rates and mortgage costs

This month we are featuring the spread between Bank Rate and consumer mortgage pricing over the past twenty years. Bank Rate has been fixed at 3.75% since December 2025, yet two-year fixes at 75% LTV spiked to roughly 5.1% in the spring before falling back to about 4.8% — a reminder that borrowers are priced off swap rates and gilt yields, not off the Bank’s decisions directly. The other notable feature is the inversion: for most of the 2010s the five-year fix carried a clear premium over the two-year, but since 2023 that relationship has reversed, with five-year money now the cheaper option at roughly 4.65%. Markets are, in effect, still pricing rates lower over the medium term even as the near-term path stays stuck.

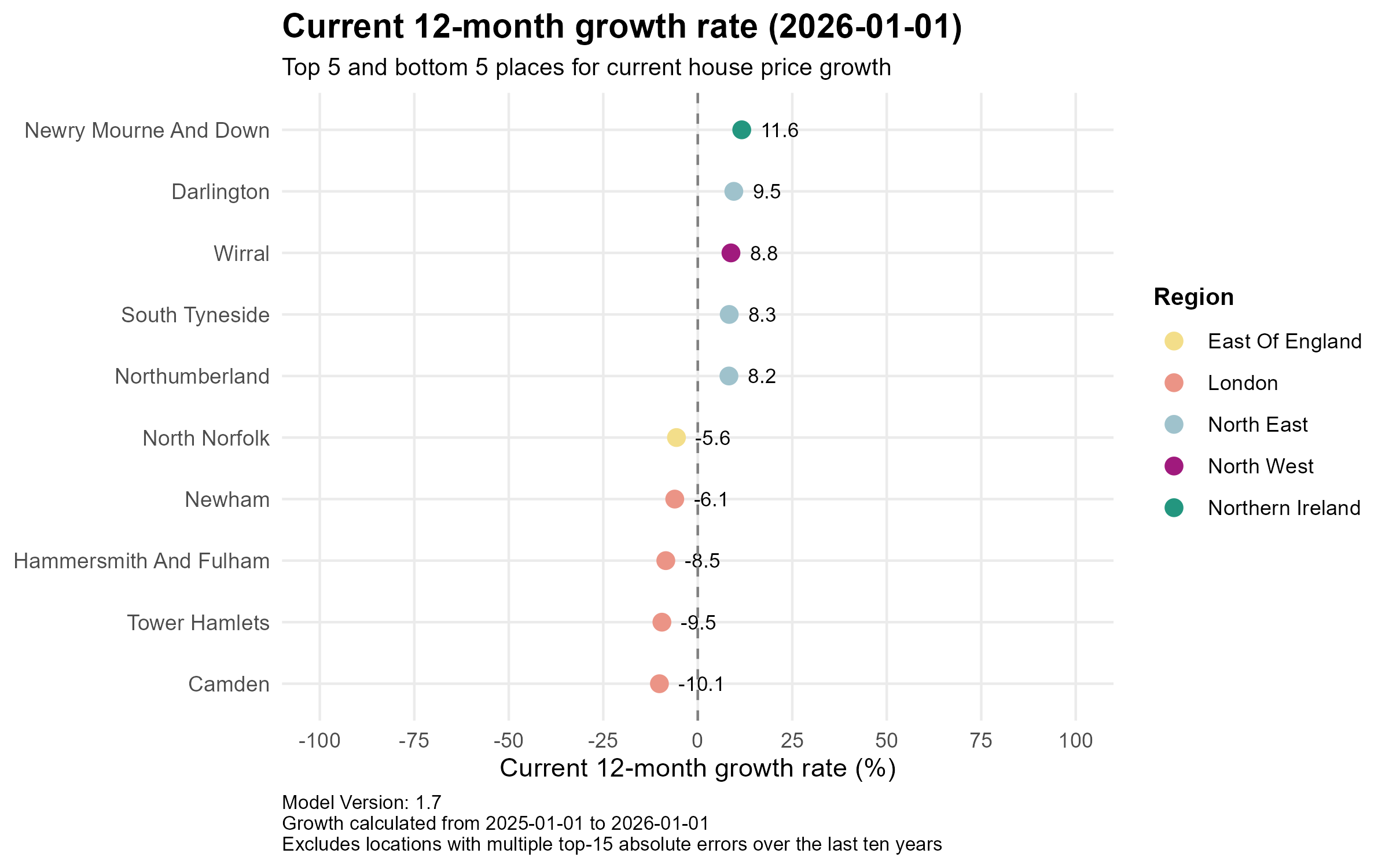

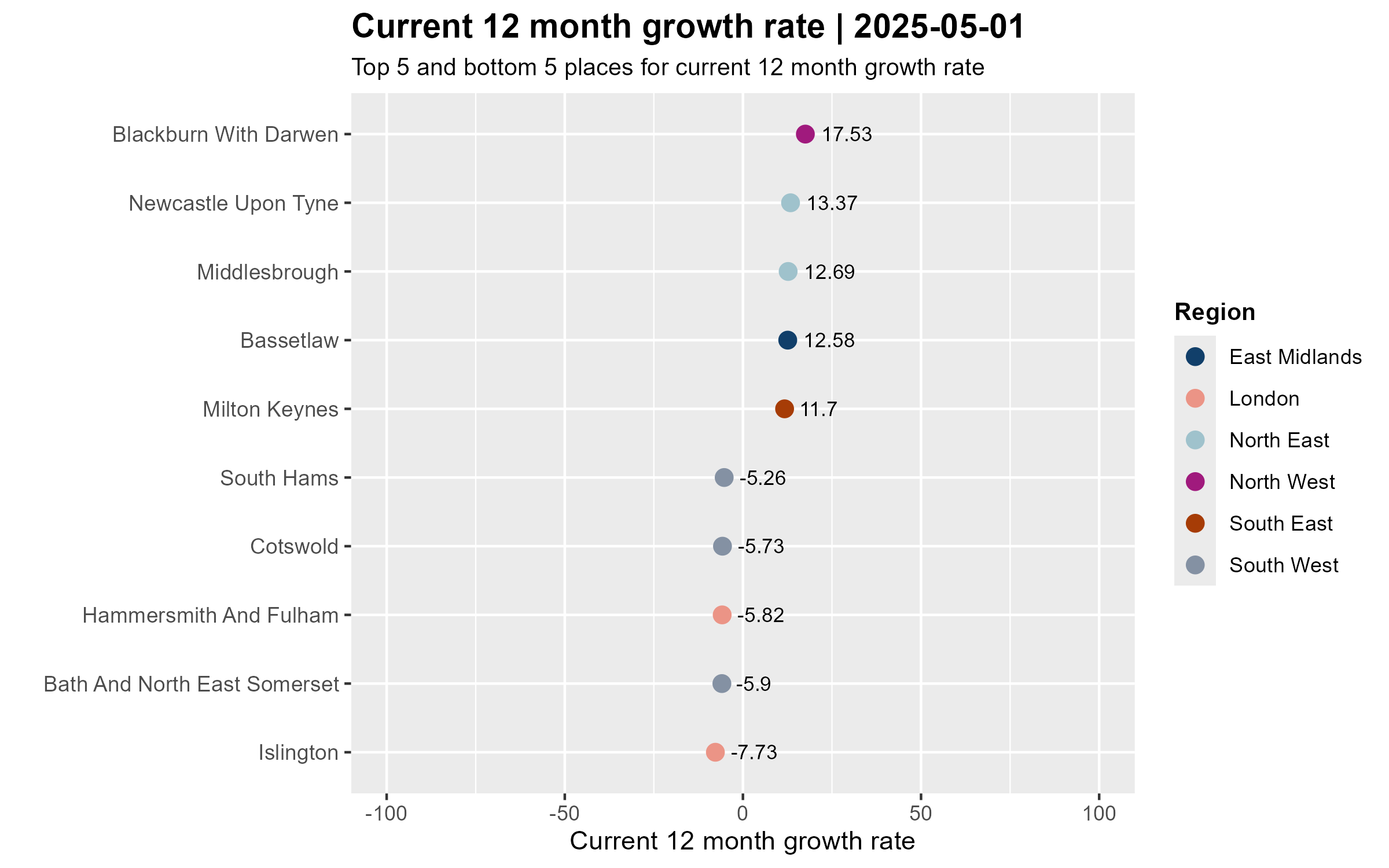

Current growth rates

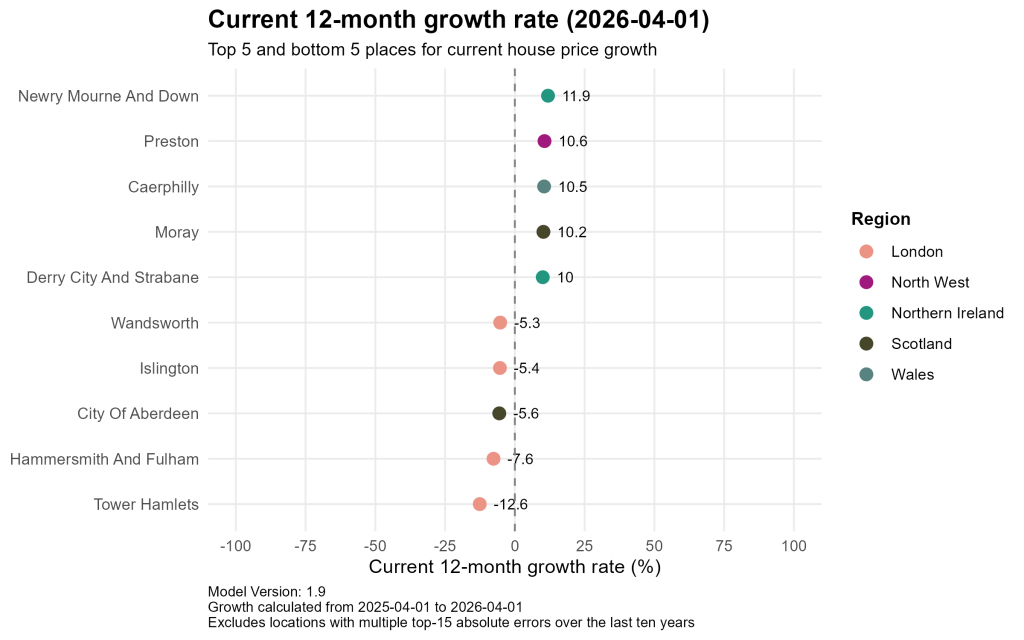

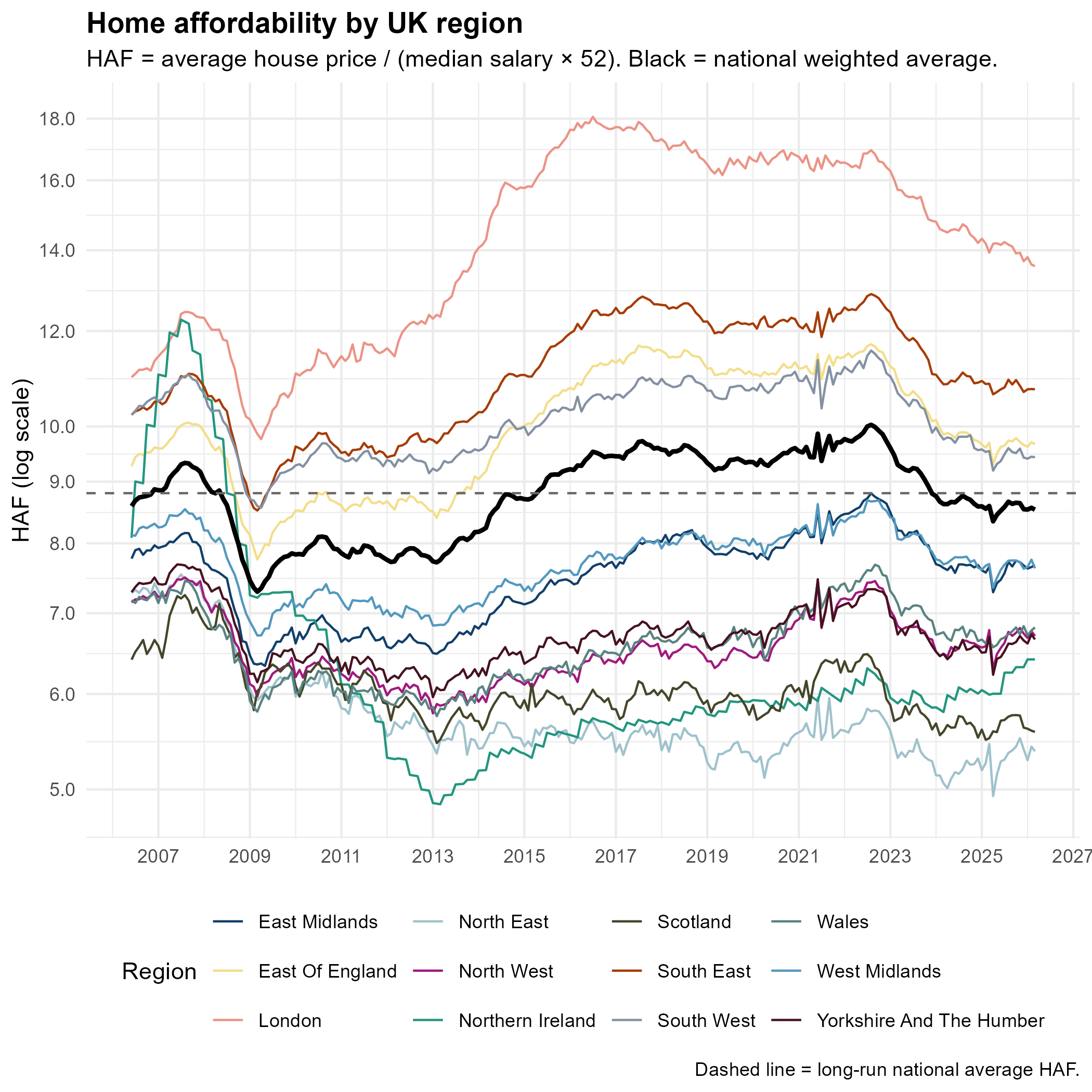

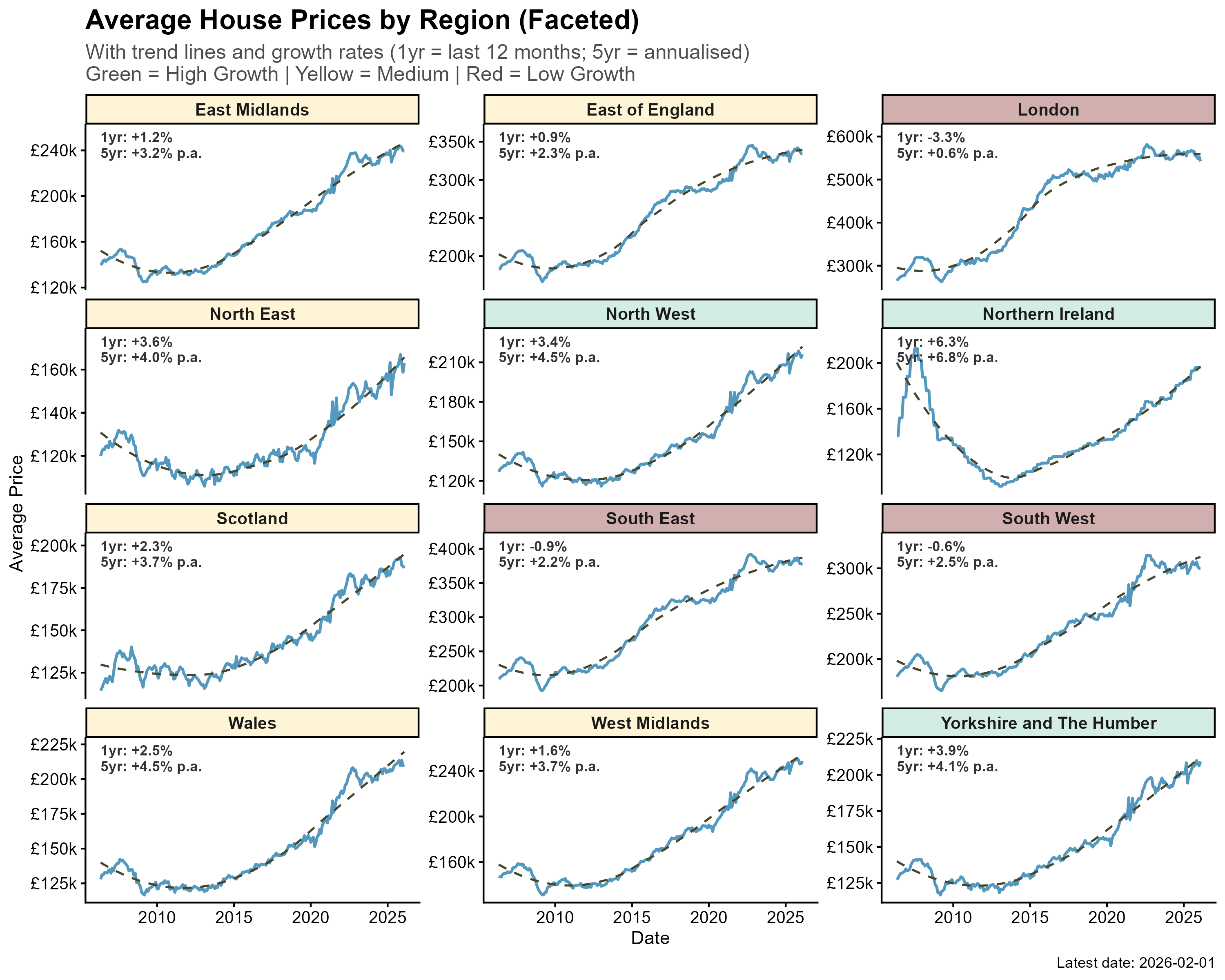

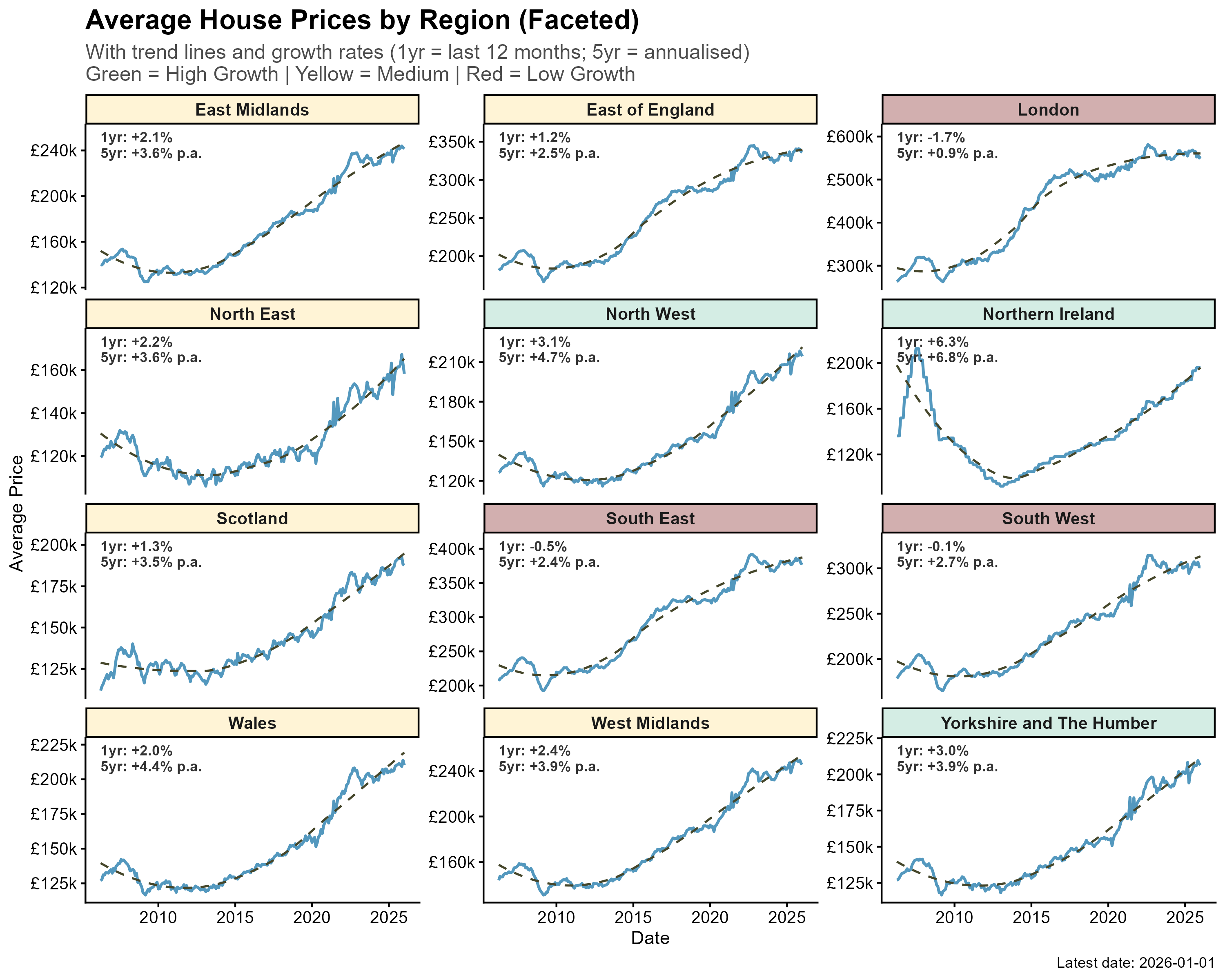

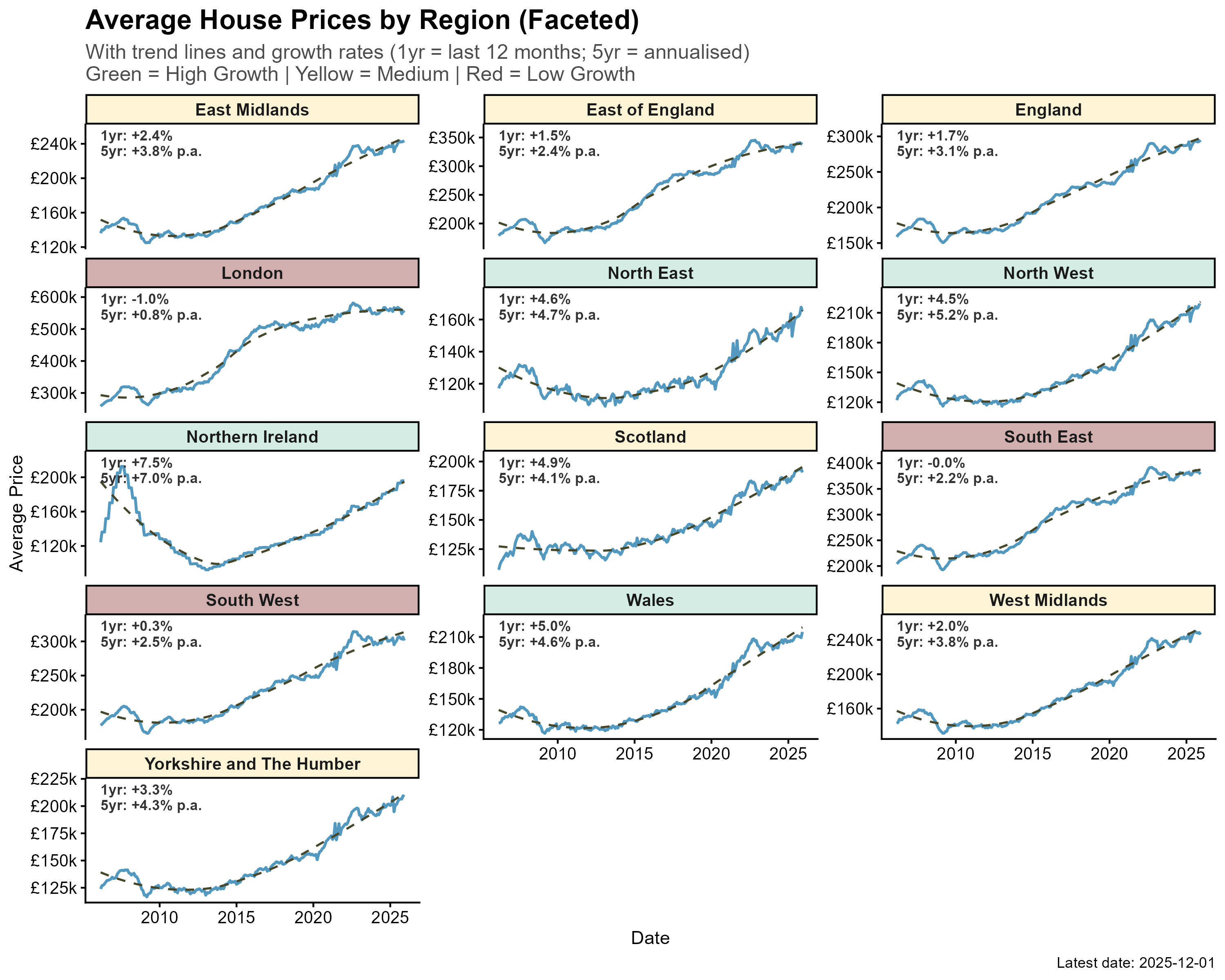

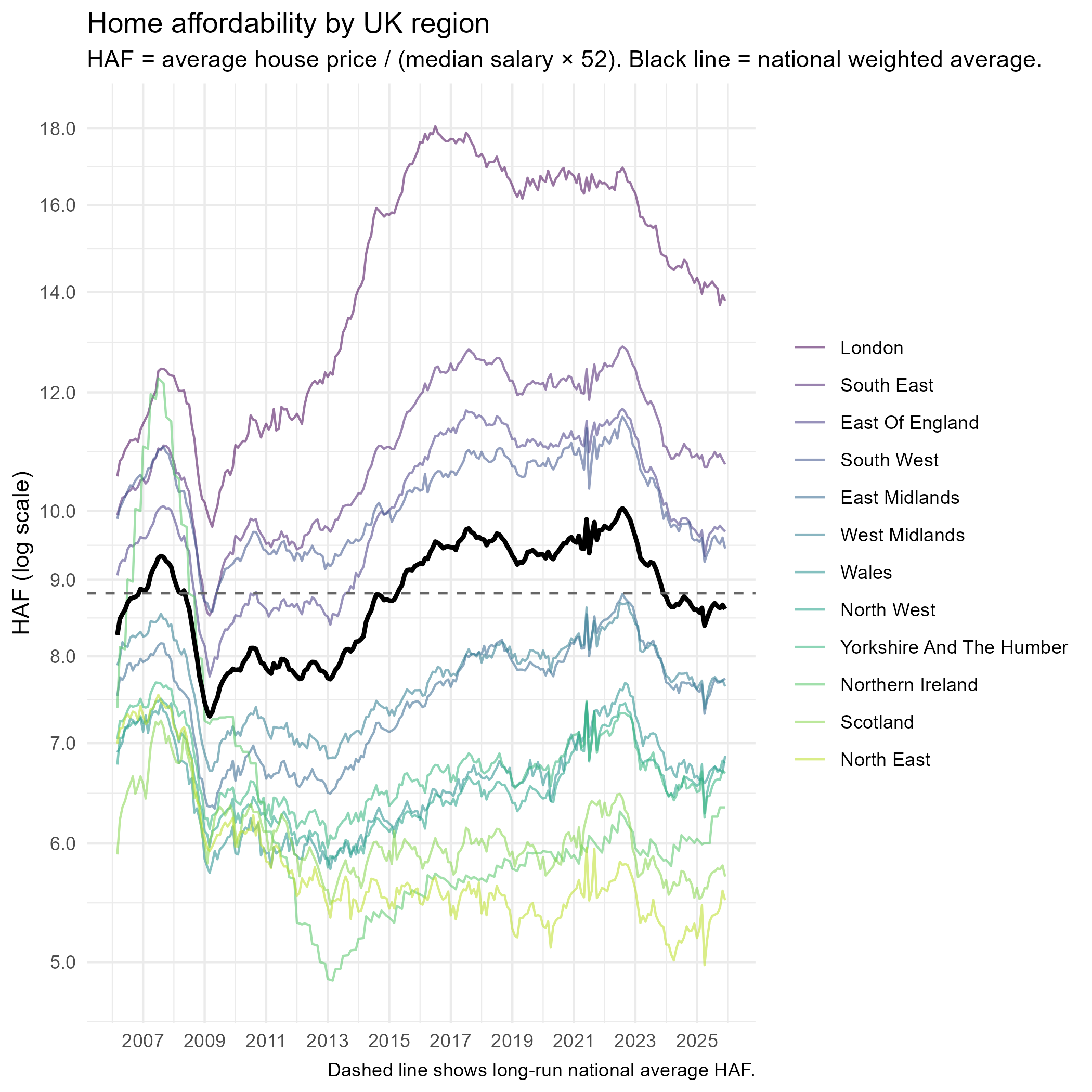

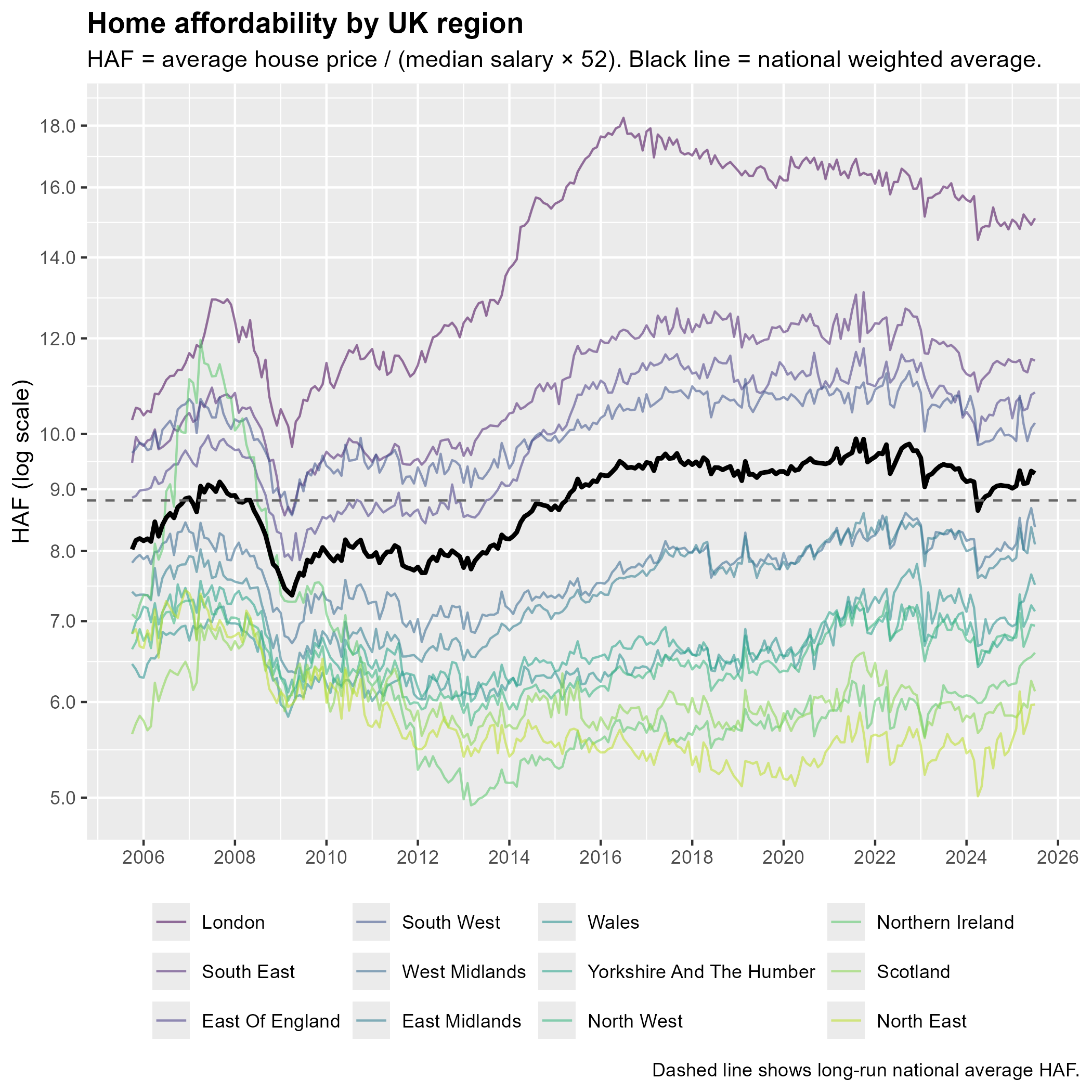

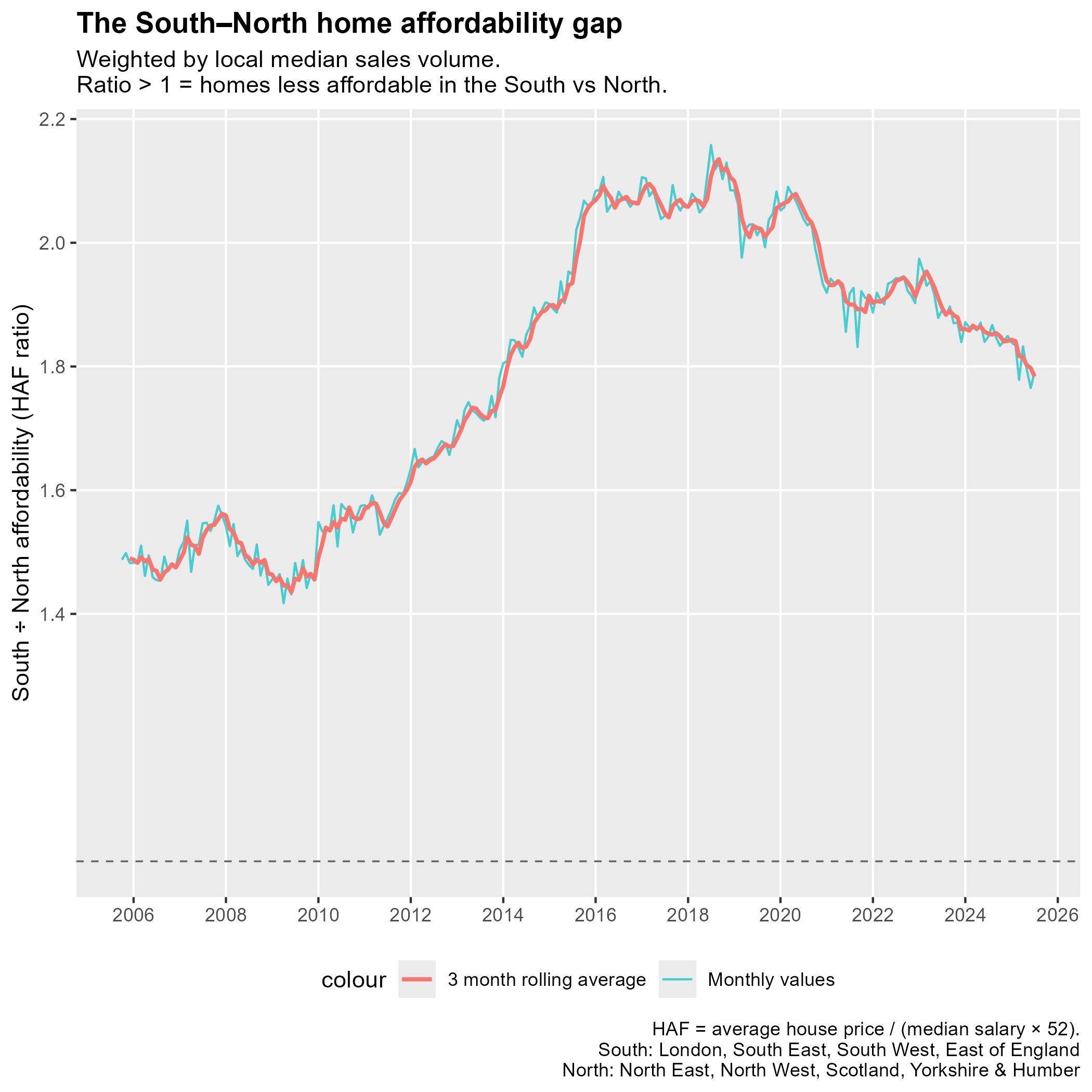

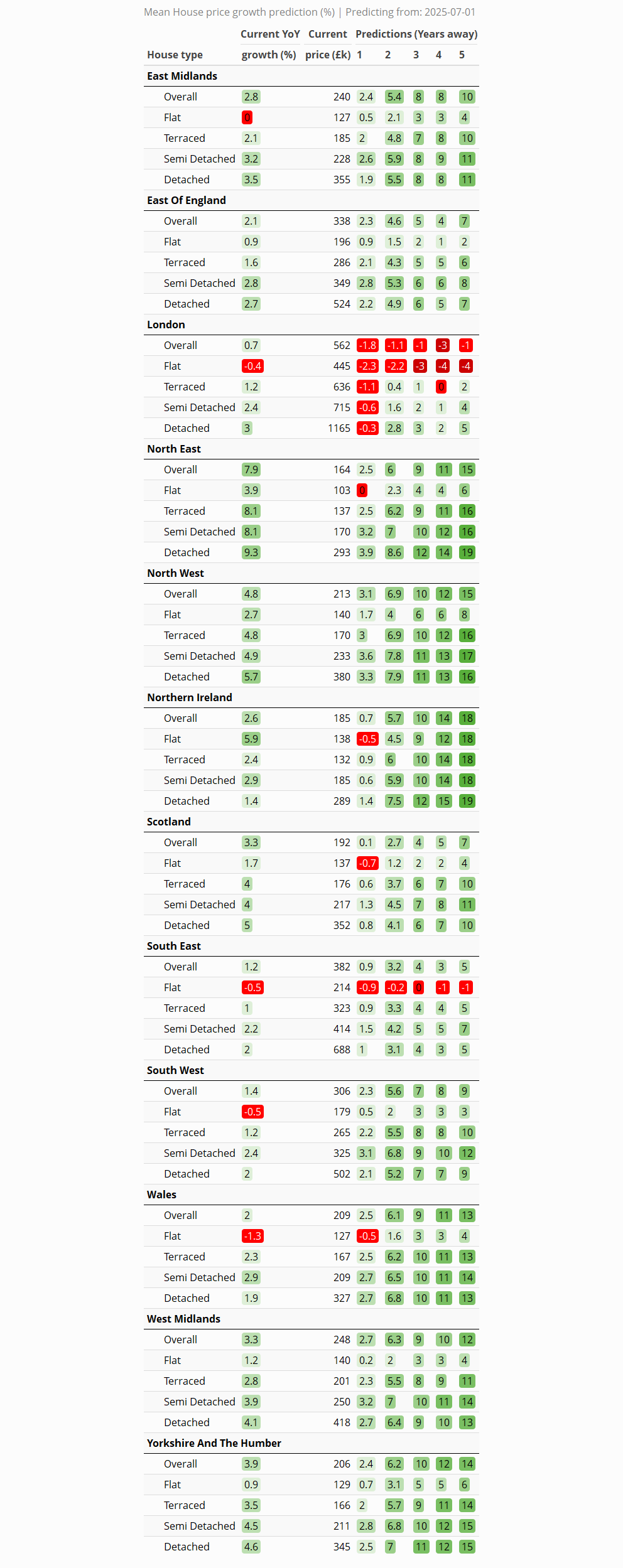

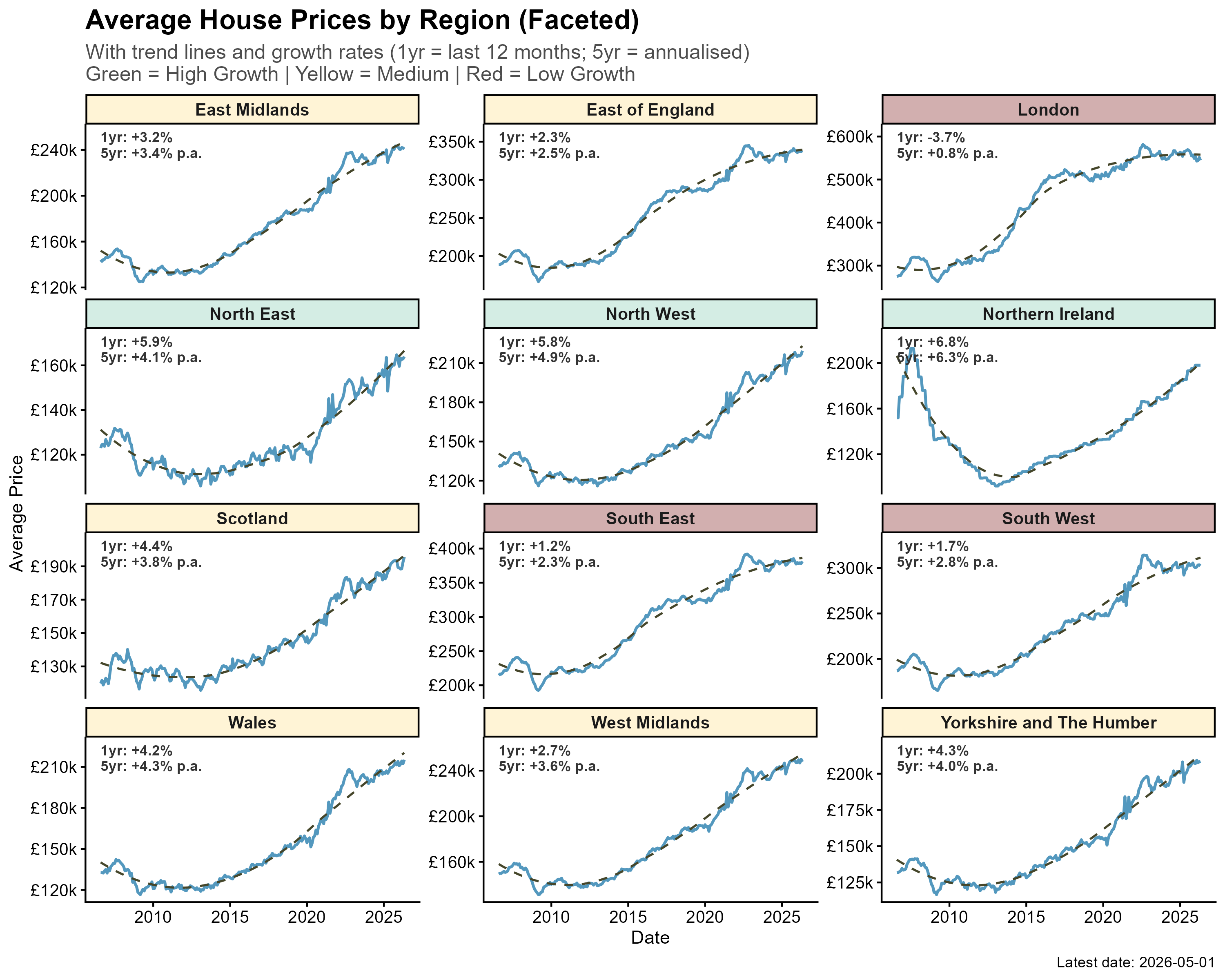

The north–south split remains the defining feature of the market, and the five-year annualised figures confirm it is structural rather than a one-month quirk. Northern Ireland leads on both measures, up 6.8% over the year and 6.3% a year over five years, followed by the North East (+5.9% and +4.1% p.a.) and the North West (+5.8% and +4.9% p.a.). Scotland (+4.4%), Yorkshire and The Humber (+4.3%) and Wales (+4.2%) form a solid middle tier with five-year rates of around 4%. The South East (+1.2%), South West (+1.7%) and East of England (+2.3%) lag, while London is the clear outlier at −3.7% over the year and just +0.8% a year over five.

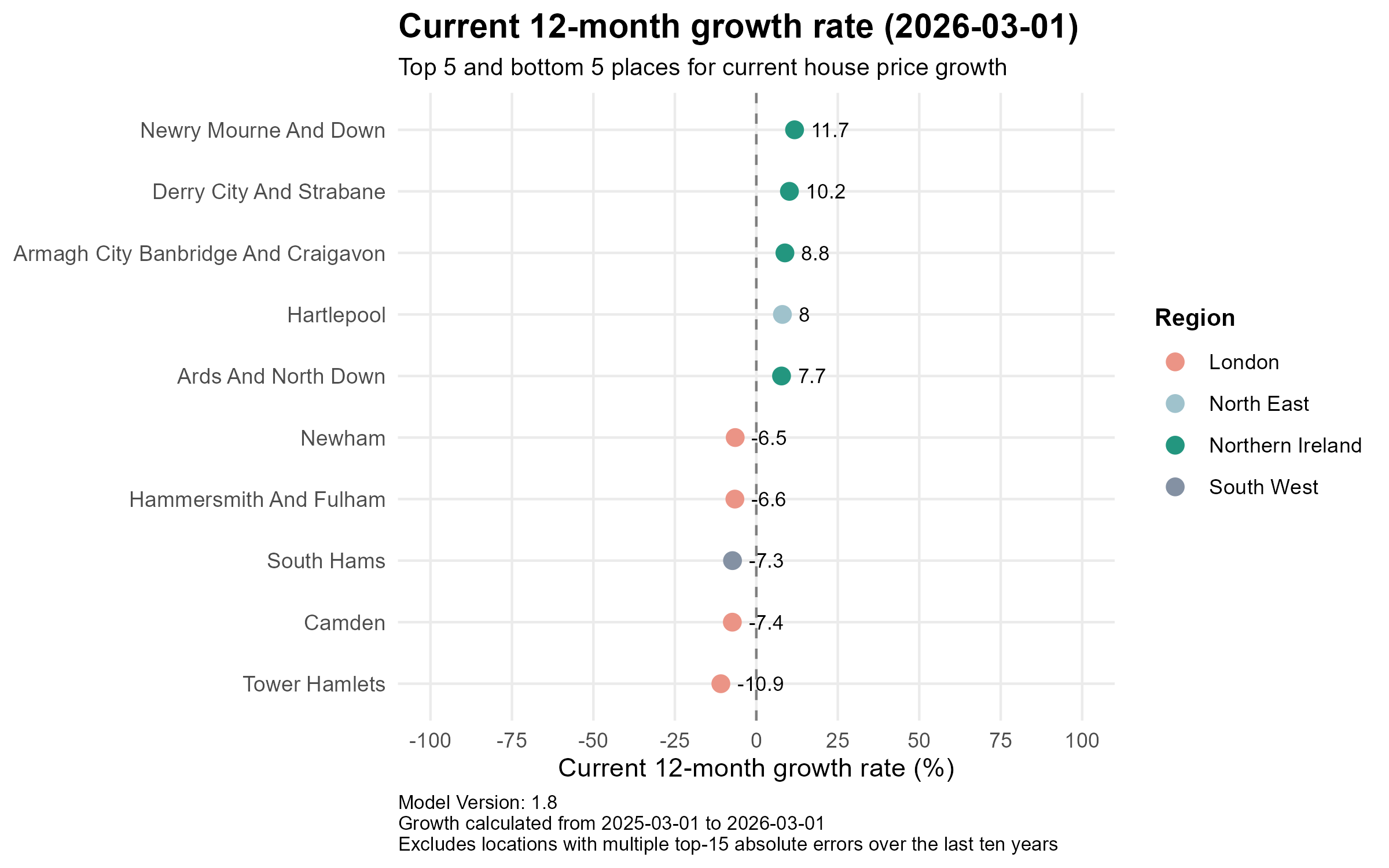

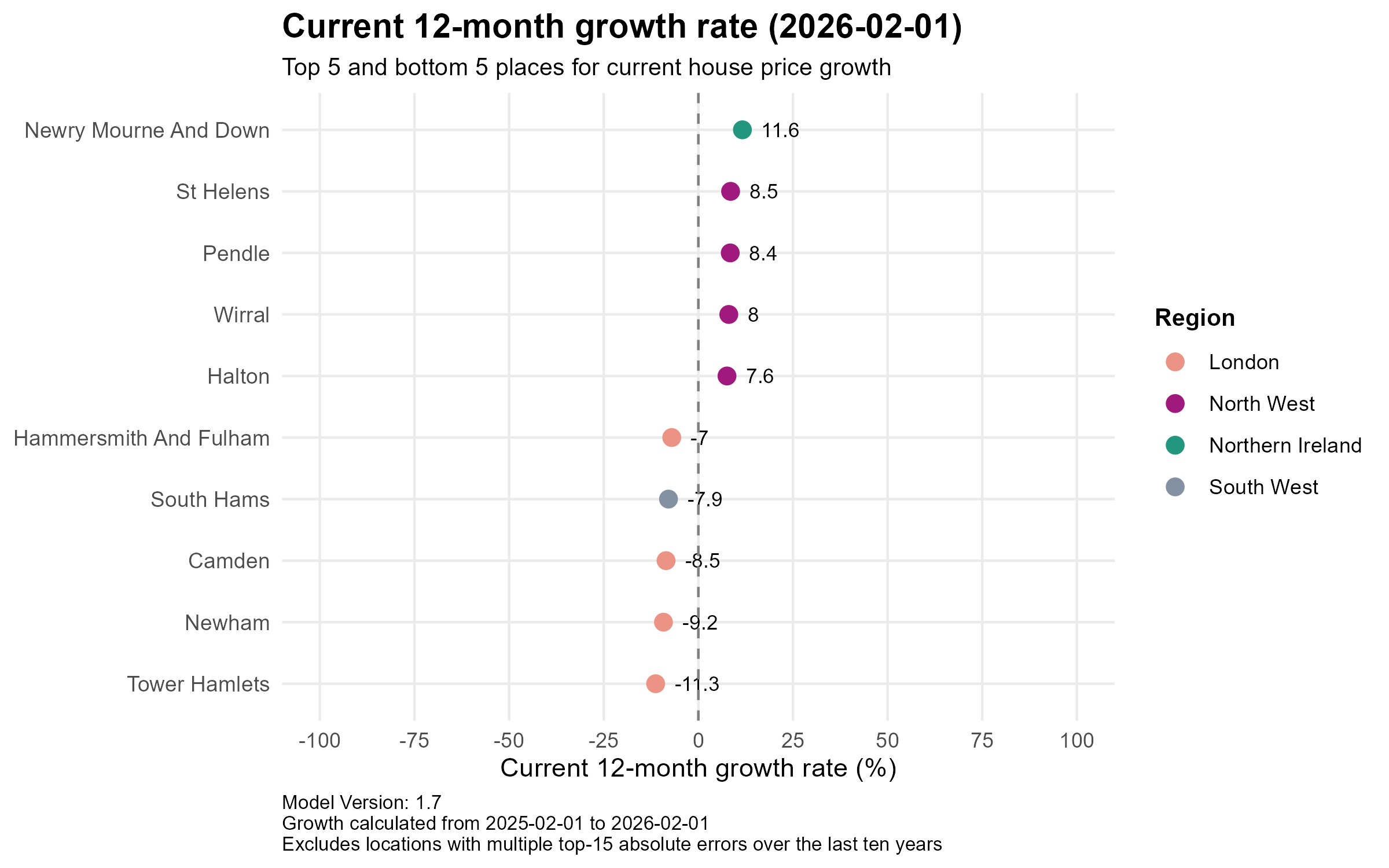

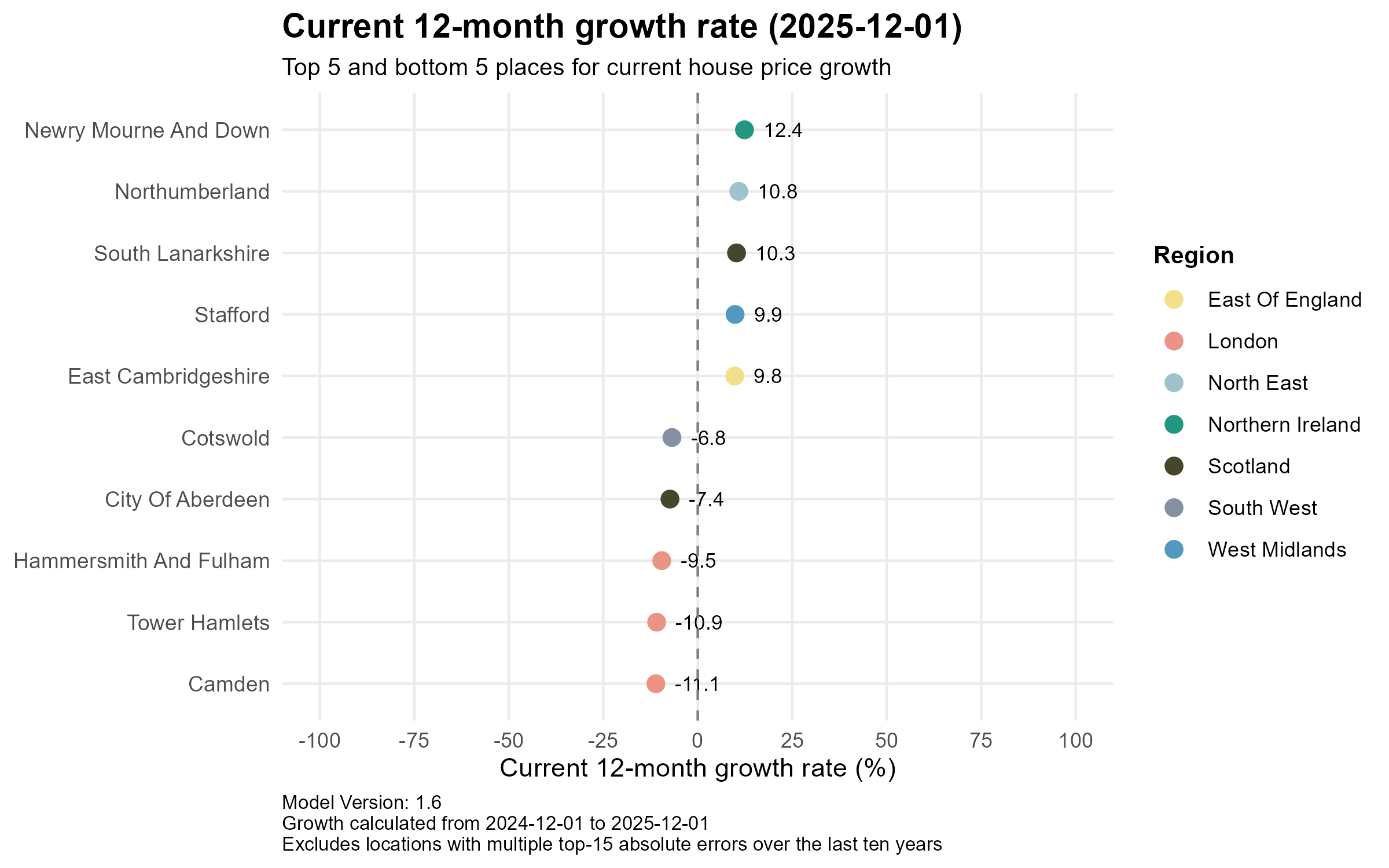

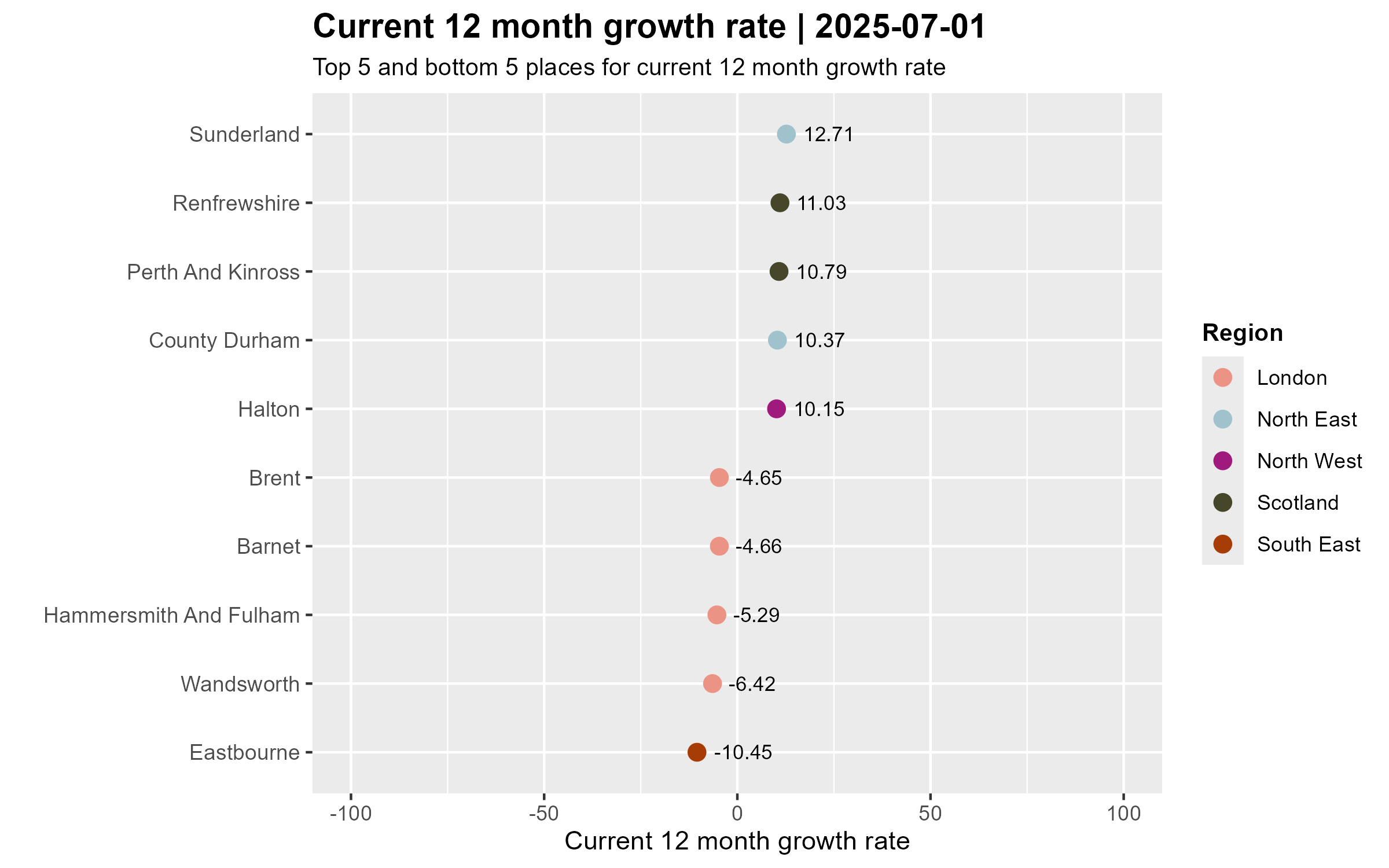

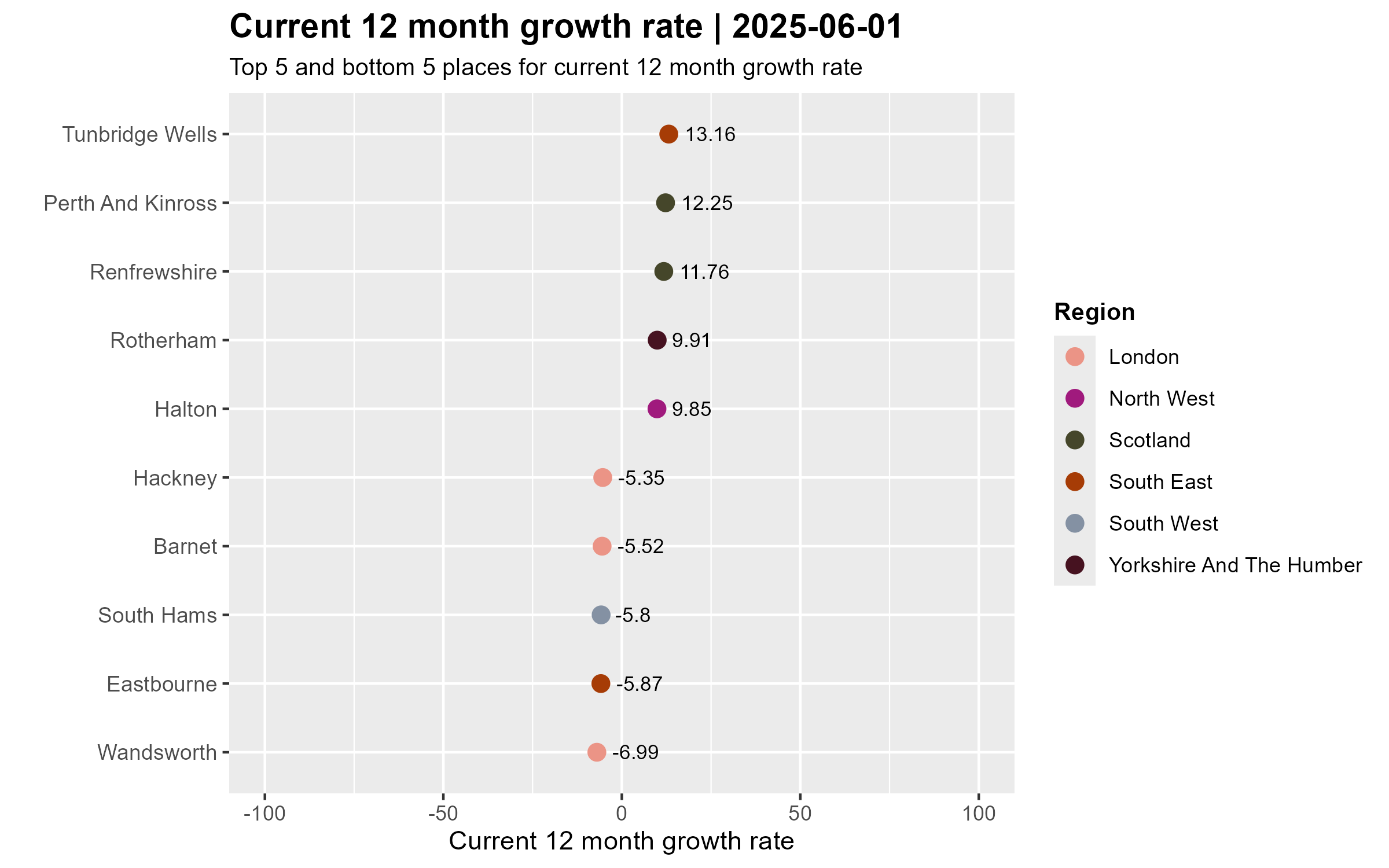

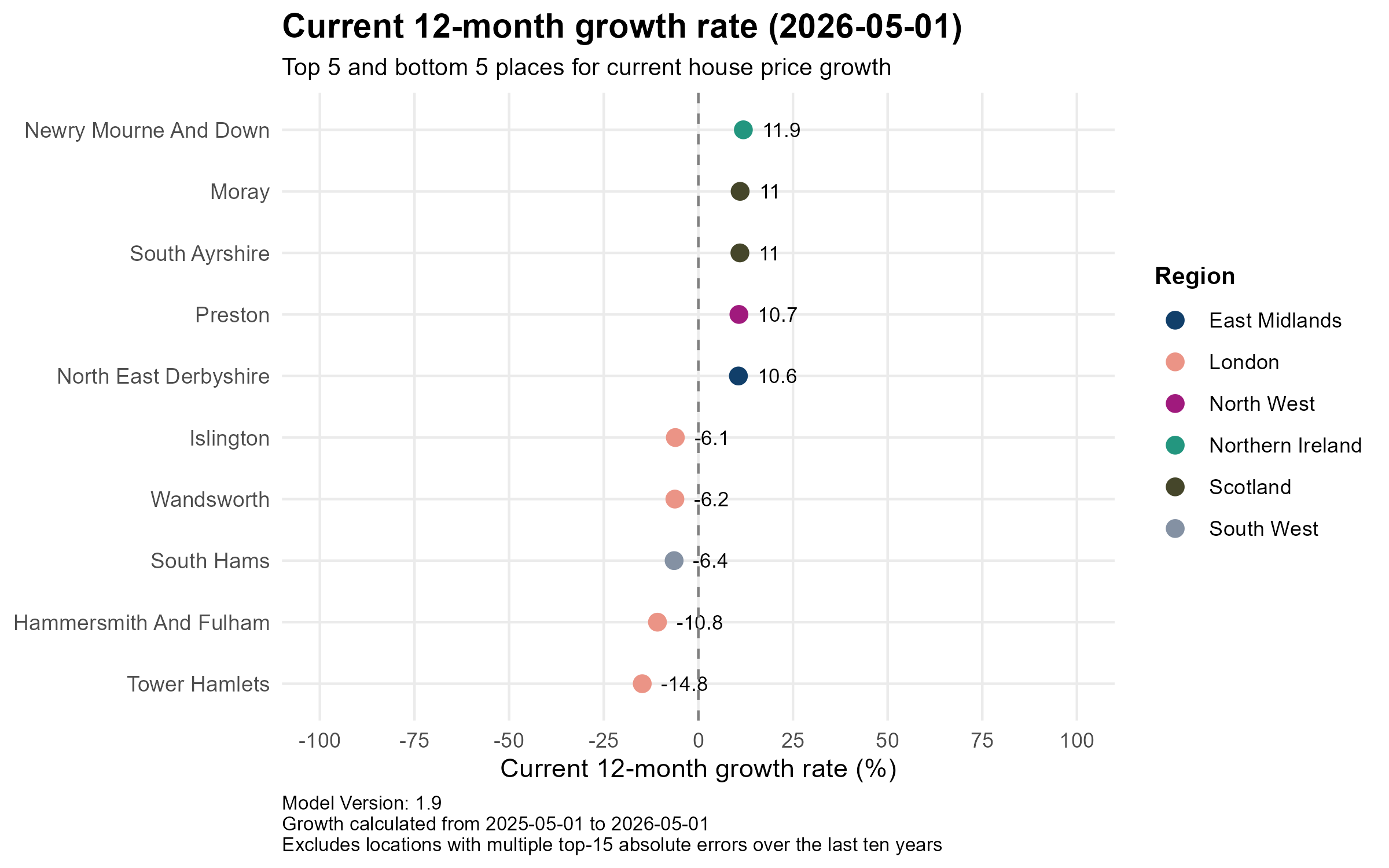

At local level the dispersion is wider still. Newry Mourne and Down in Northern Ireland again tops the table with 12-month growth of +11.9%, followed by two Scottish authorities, Moray and South Ayrshire, both at +11.0%, with Preston in the North West (+10.7%) and North East Derbyshire in the East Midlands (+10.6%) completing the top five. London occupies four of the five weakest positions: Tower Hamlets has fallen 14.8% over the year, its steepest decline yet in this series, with Hammersmith and Fulham (−10.8%), Wandsworth (−6.2%) and Islington (−6.1%) also sharply down, joined by South Hams in Devon (−6.4%). A spread of more than 26 percentage points between best and worst underlines how little the “UK market” behaves as a single market.

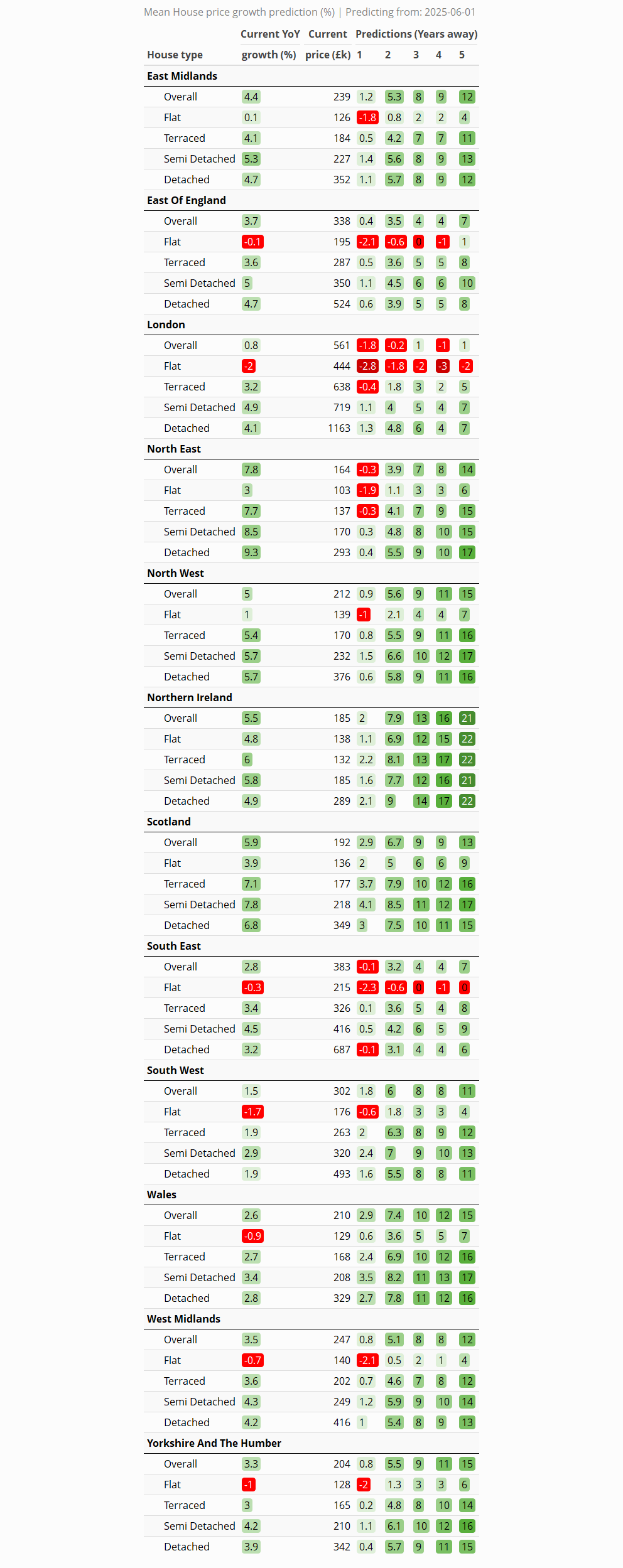

Predictions

Overall

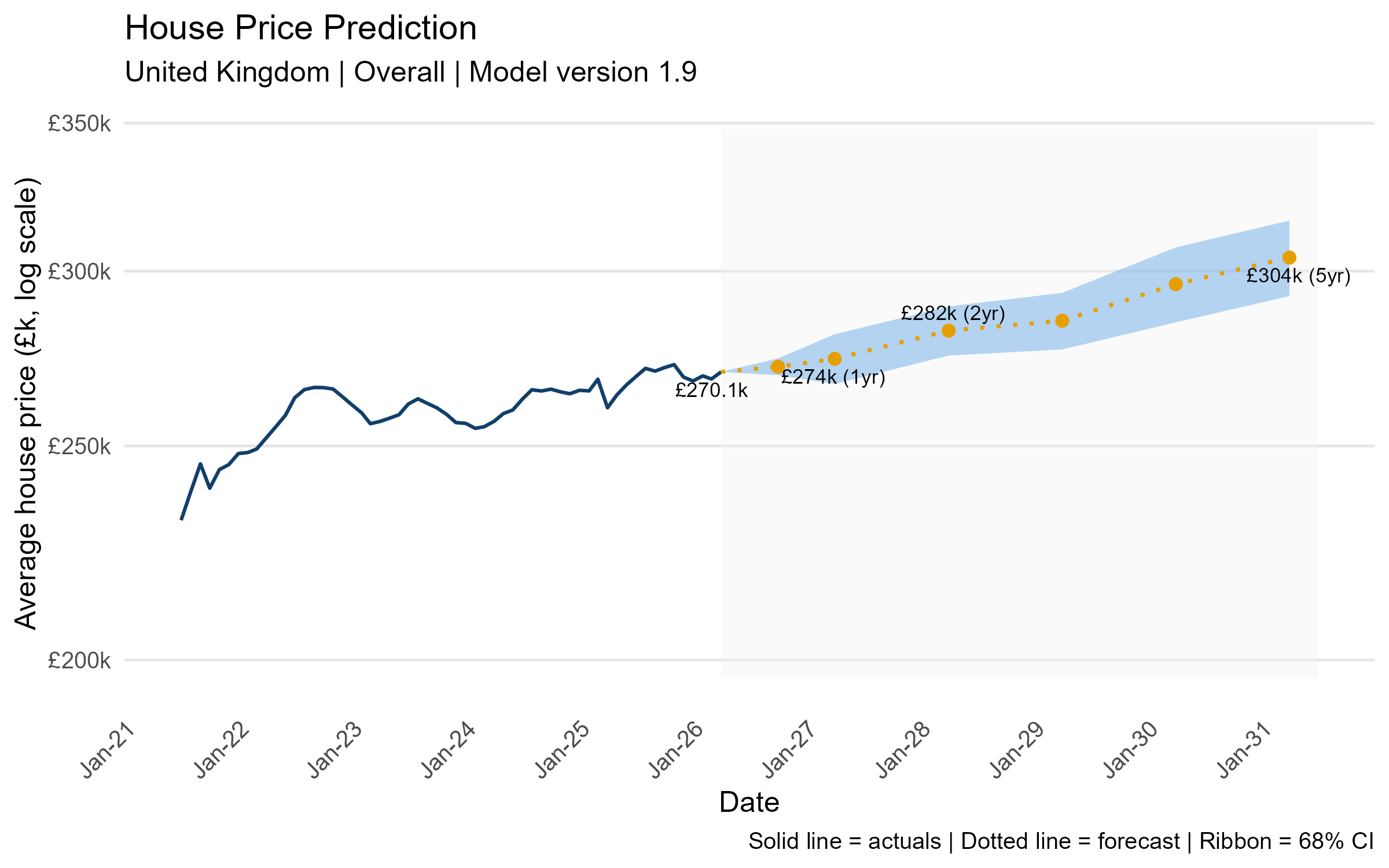

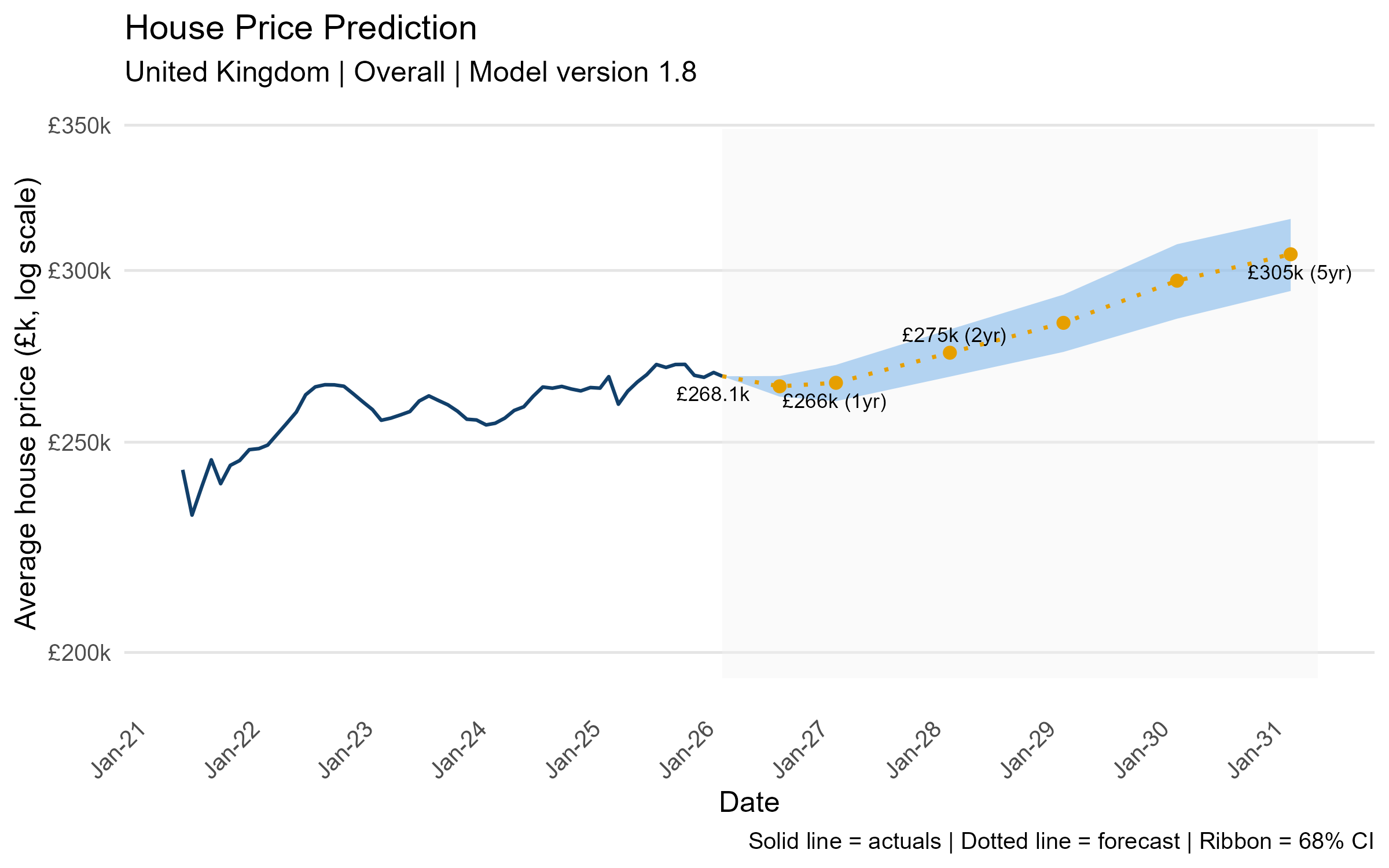

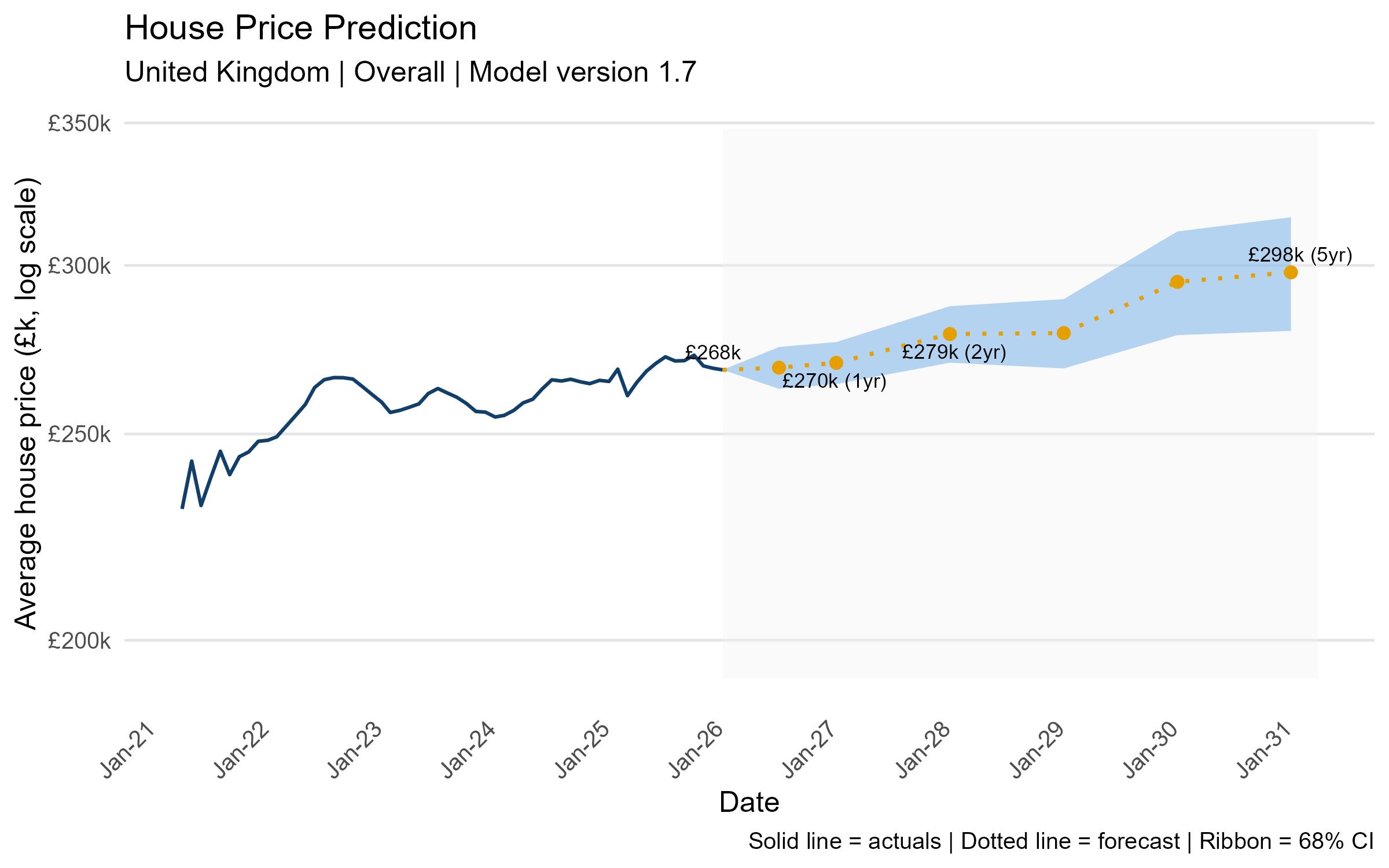

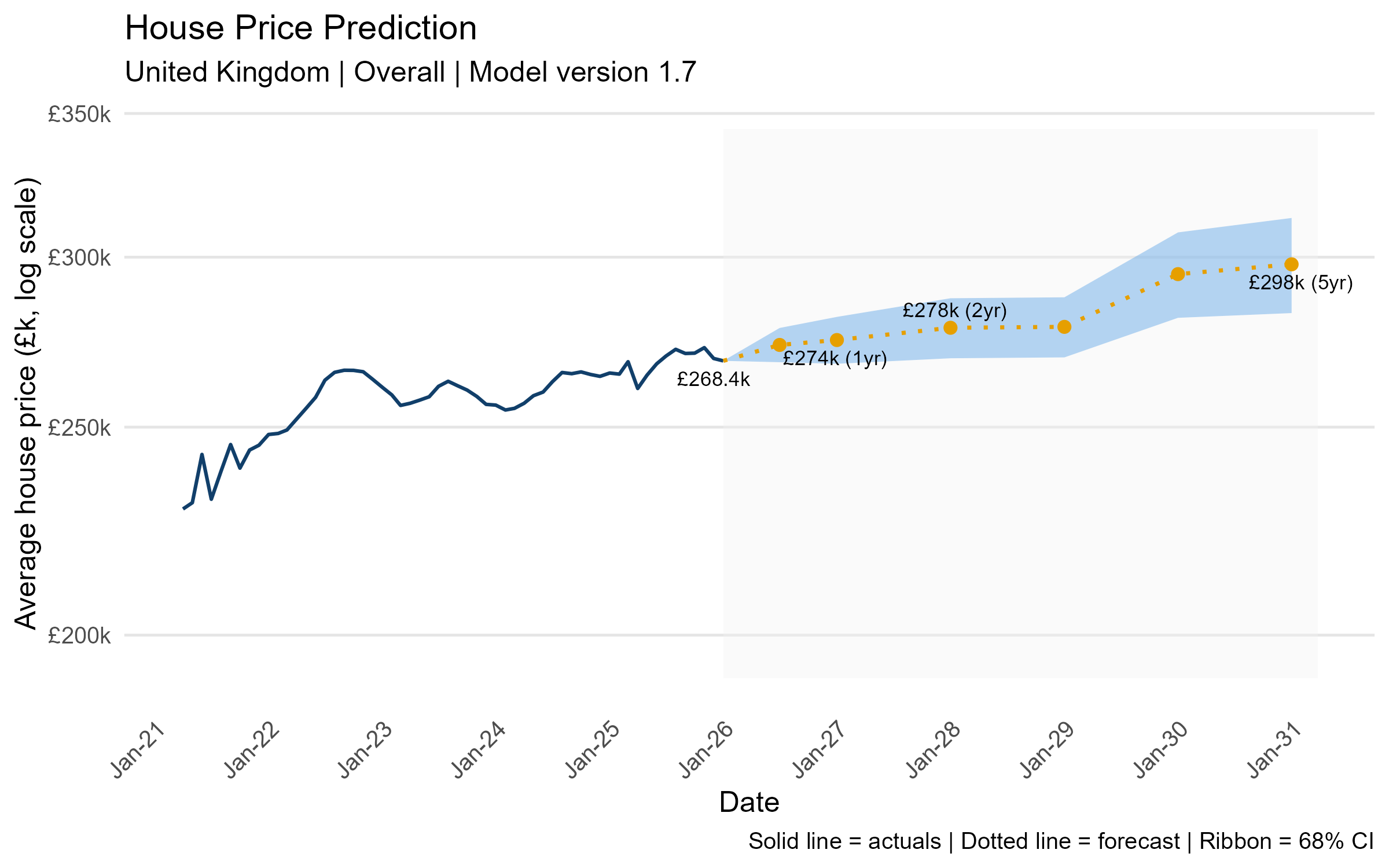

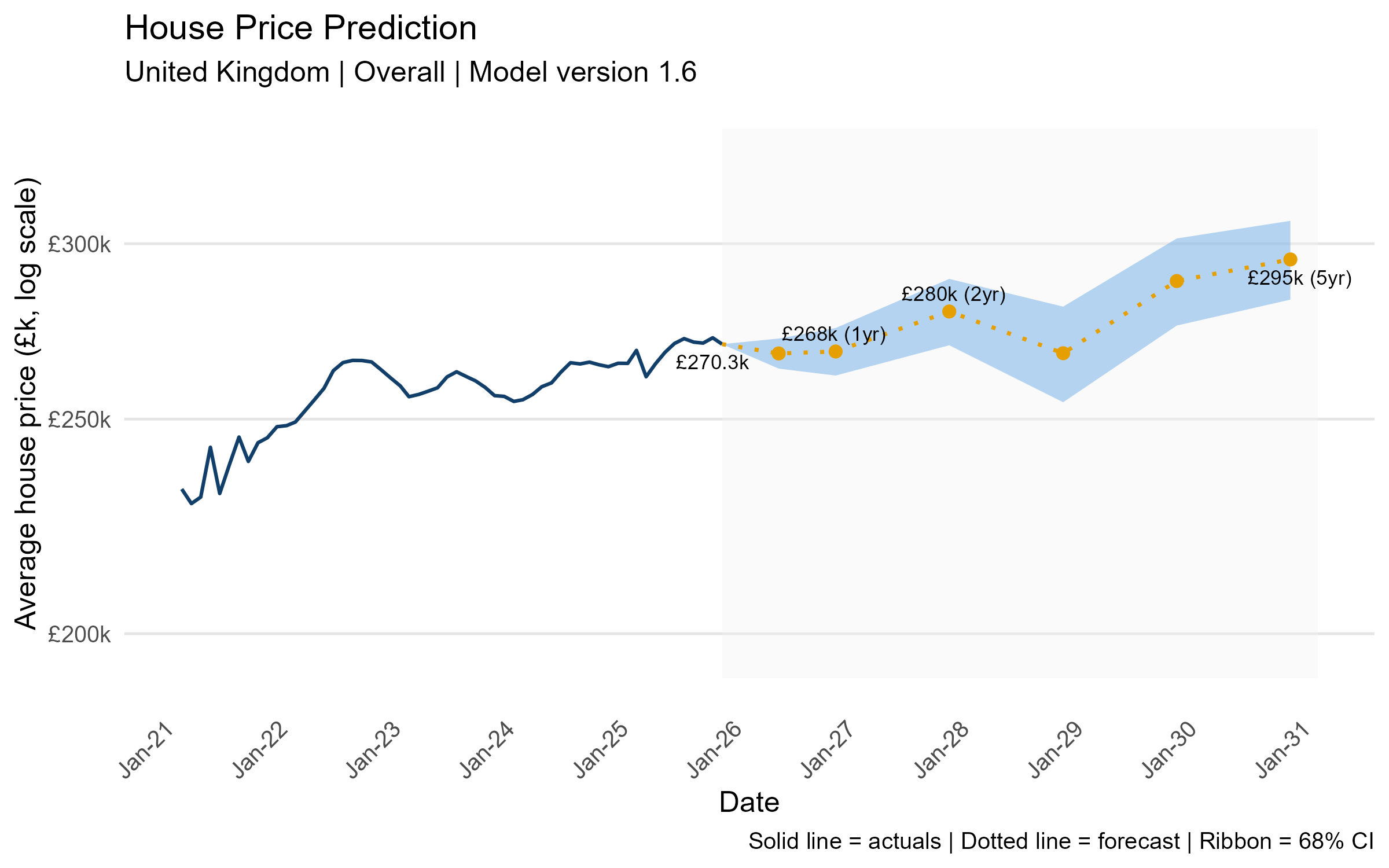

The model projects a flat year followed by a steadier climb, taking the current £271.3k to £273k within twelve months, £281k by 2028 and around £297k by 2031, cumulative growth of roughly 9.5% over five years. That is a more conservative long-run path than last month’s £304k, and the widening confidence band beyond year two reflects genuine uncertainty in the rate outlook.

Regional

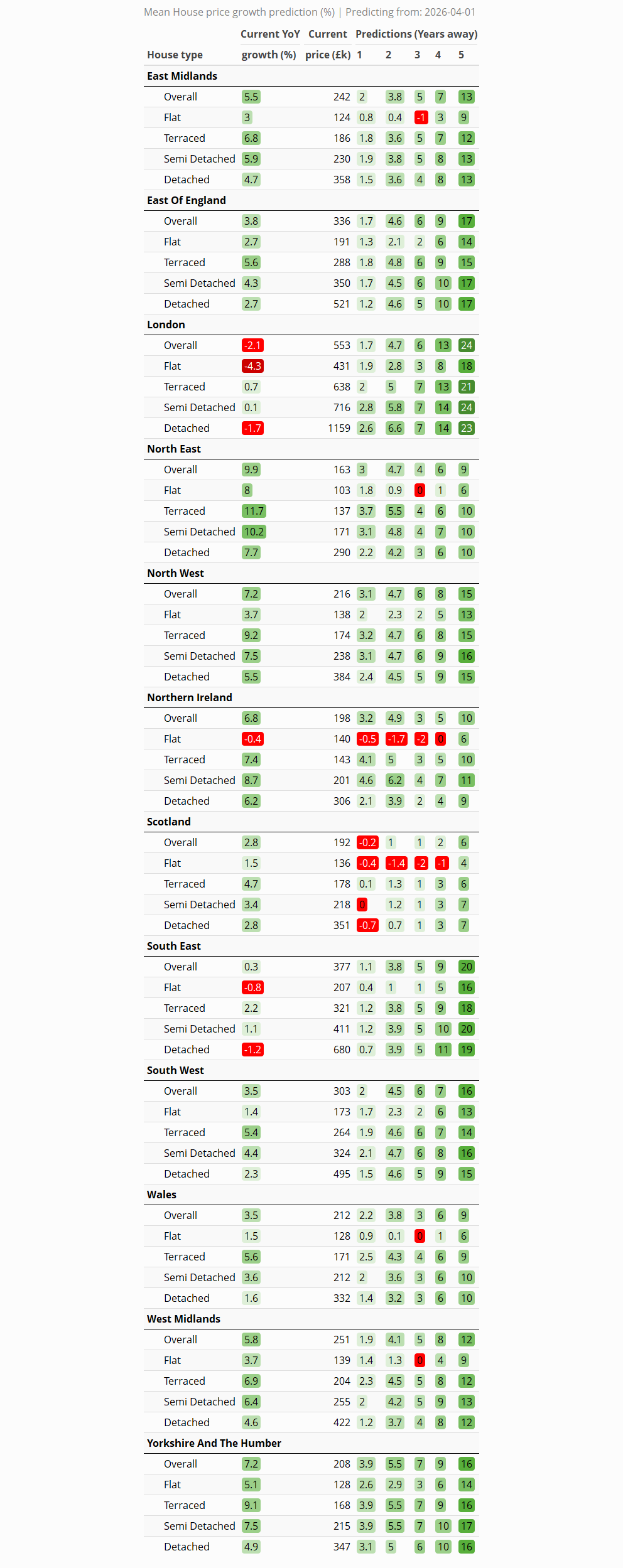

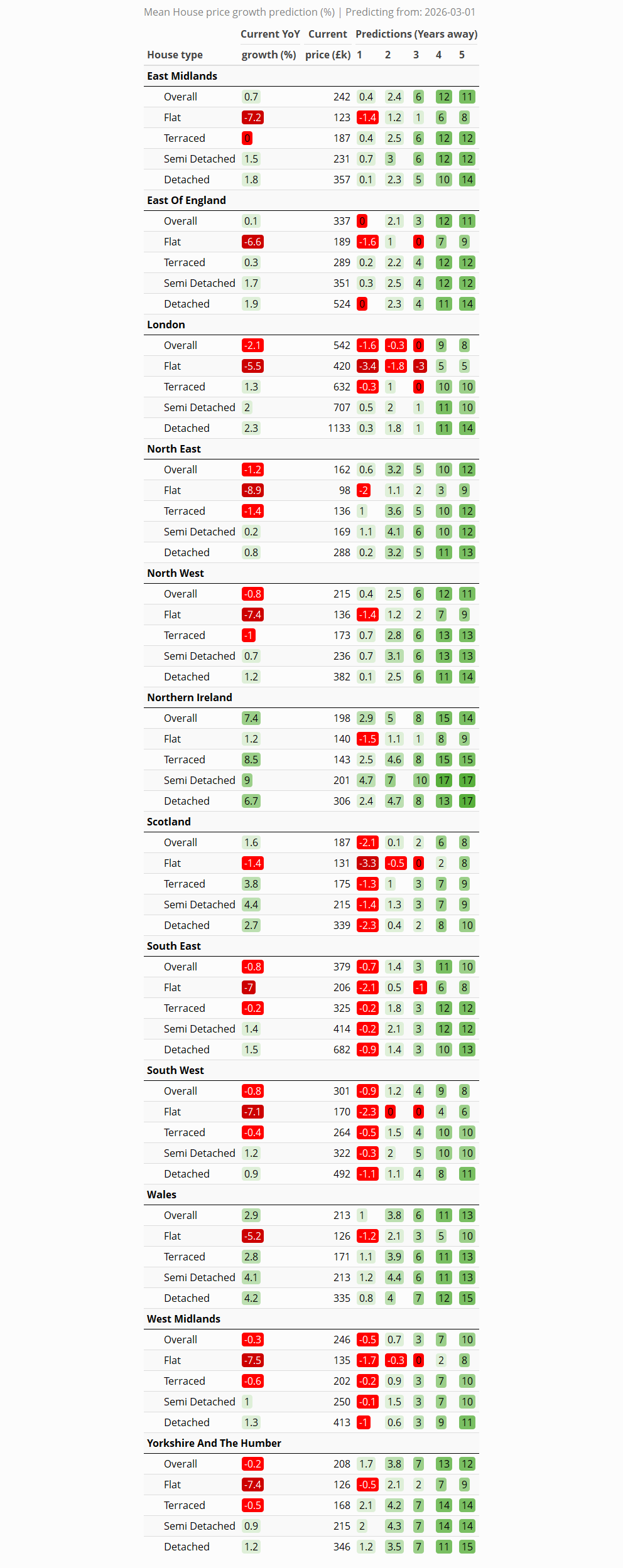

Short term (years 1–2): Every region is forecast to grow in year one, led by the North West (+2.7%), Yorkshire and The Humber (+2.5%) and Northern Ireland (+2.4%), with Scotland the laggard at just +0.5%. By year two the pack tightens considerably, with the North West and South West (both +4.2%), the East of England (+4.1%) and London, the South East and Northern Ireland (all +4.0%) clustered together, while Scotland still trails at +1.9%.

Medium term (years 3–4): From year three the southern regions take over. London reaches +6% cumulative by year three, ahead of the East of England, South East, South West, North West and Yorkshire (all around +5%), and by year four the South East leads at +8% with London, the East of England, North West, South West and Yorkshire all at +7%. Scotland (+3%), the North East (+3%) and Northern Ireland (+3%) fall well behind as their early affordability advantage is used up.

Long term (year 5): The five-year ranking is decisively southern. London tops the table at +15%, followed by the South East (+13%), the East of England (+12%) and the North West (+11%), with the South West and Yorkshire and The Humber both at +10%. The regions that led on current growth end up at the bottom: Scotland (+5%), the North East (+6%) and Northern Ireland (+6%) all trail, with Wales (+7%) not far ahead.

Flats remain the weak spot almost everywhere. The model has them falling outright in year two in the East Midlands (−0.8%), West Midlands (−0.2%), Wales (−0.5%), Scotland (−1.9%), the North East (−1.3%) and Northern Ireland (−1.6%), and still negative at year three in several of those regions, a reflection of service-charge and cladding costs that continue to weigh on the sector.

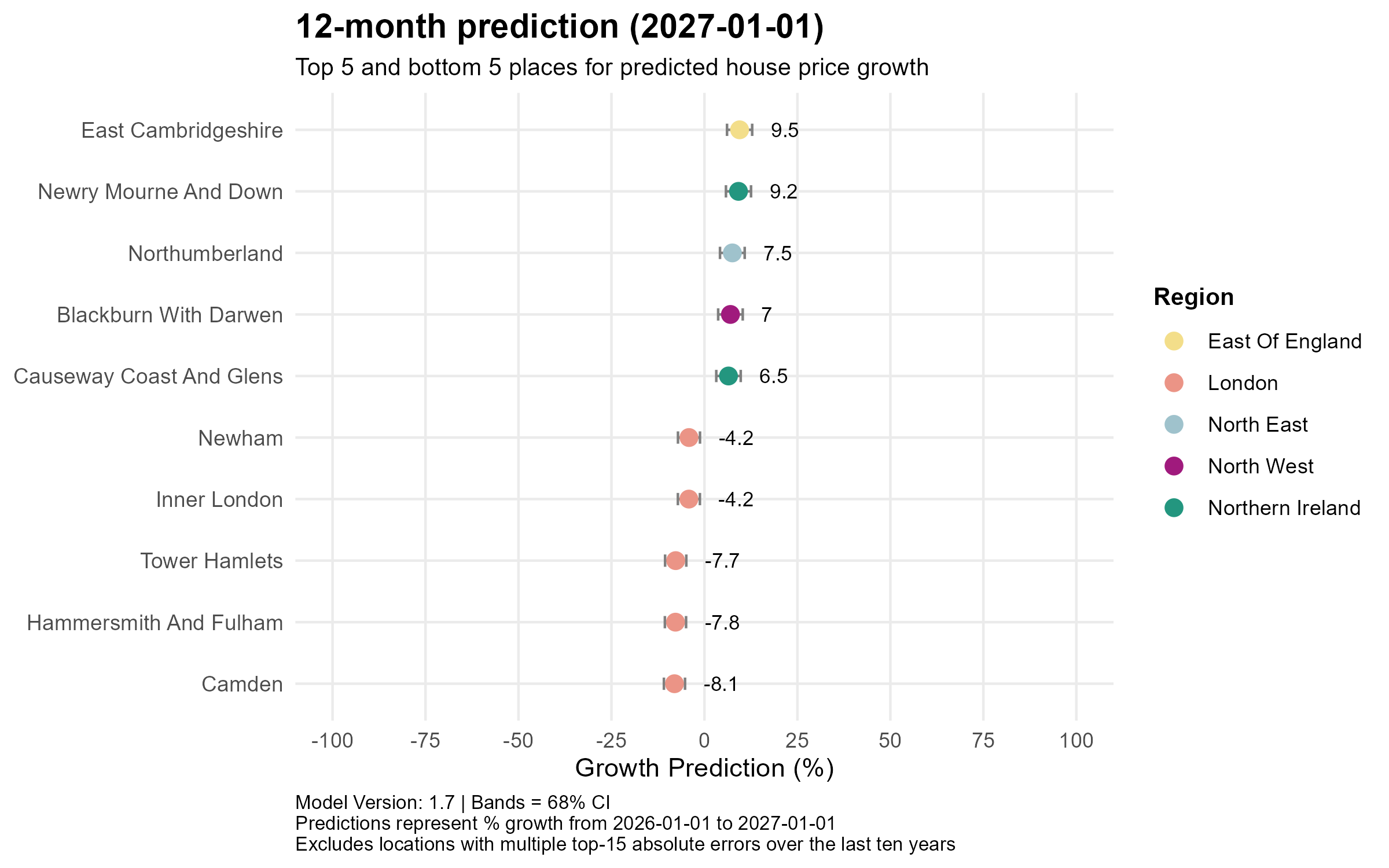

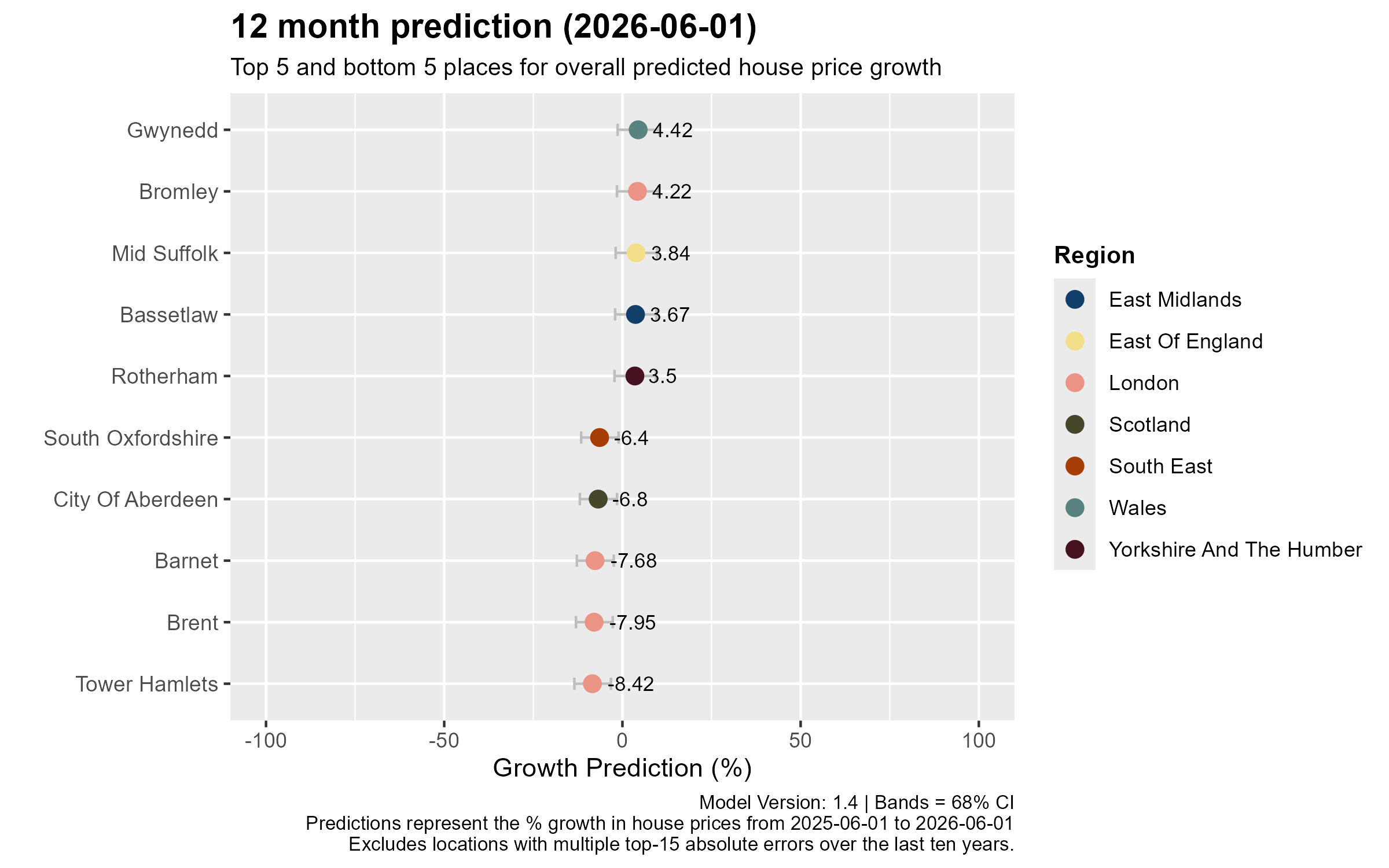

Local

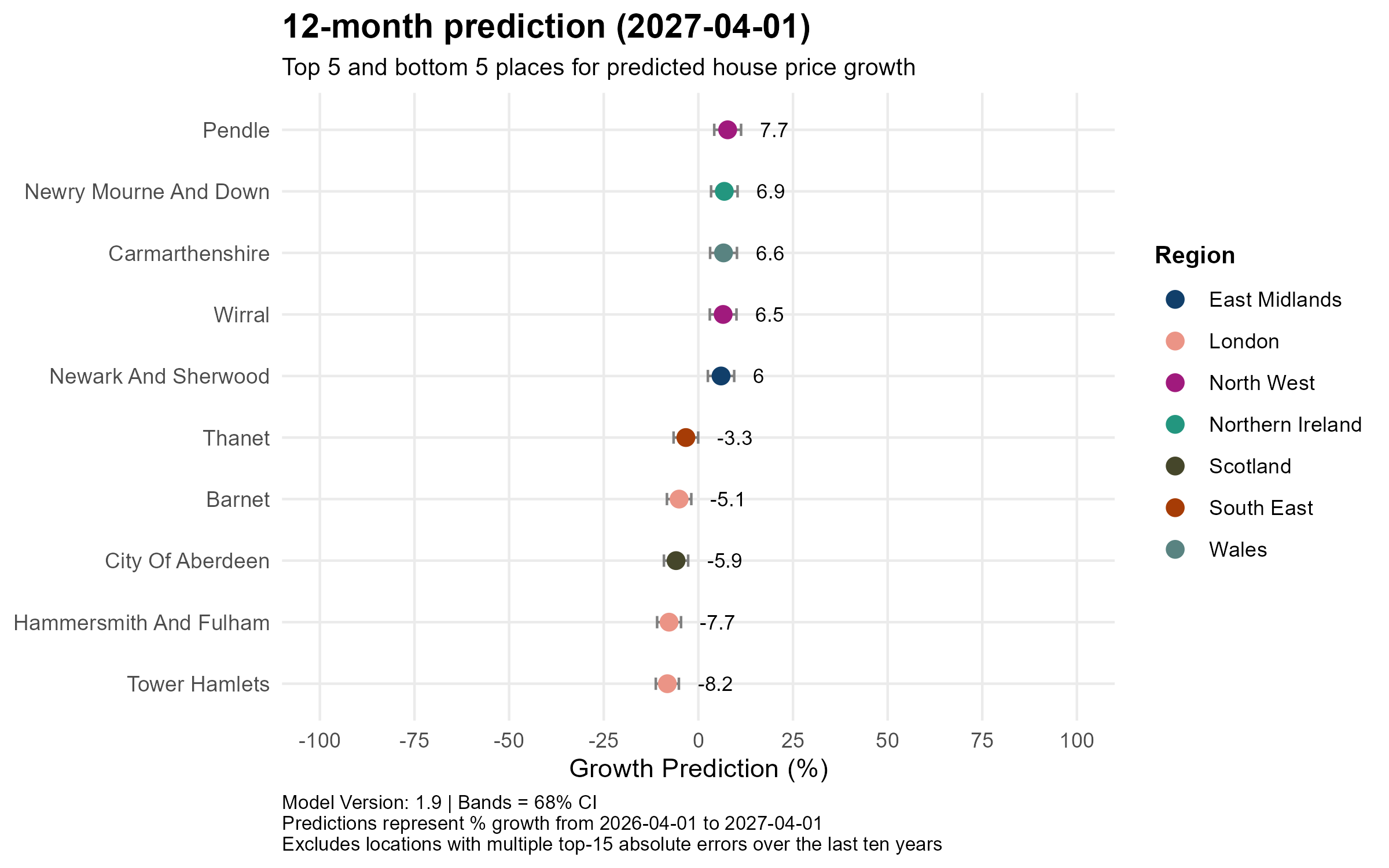

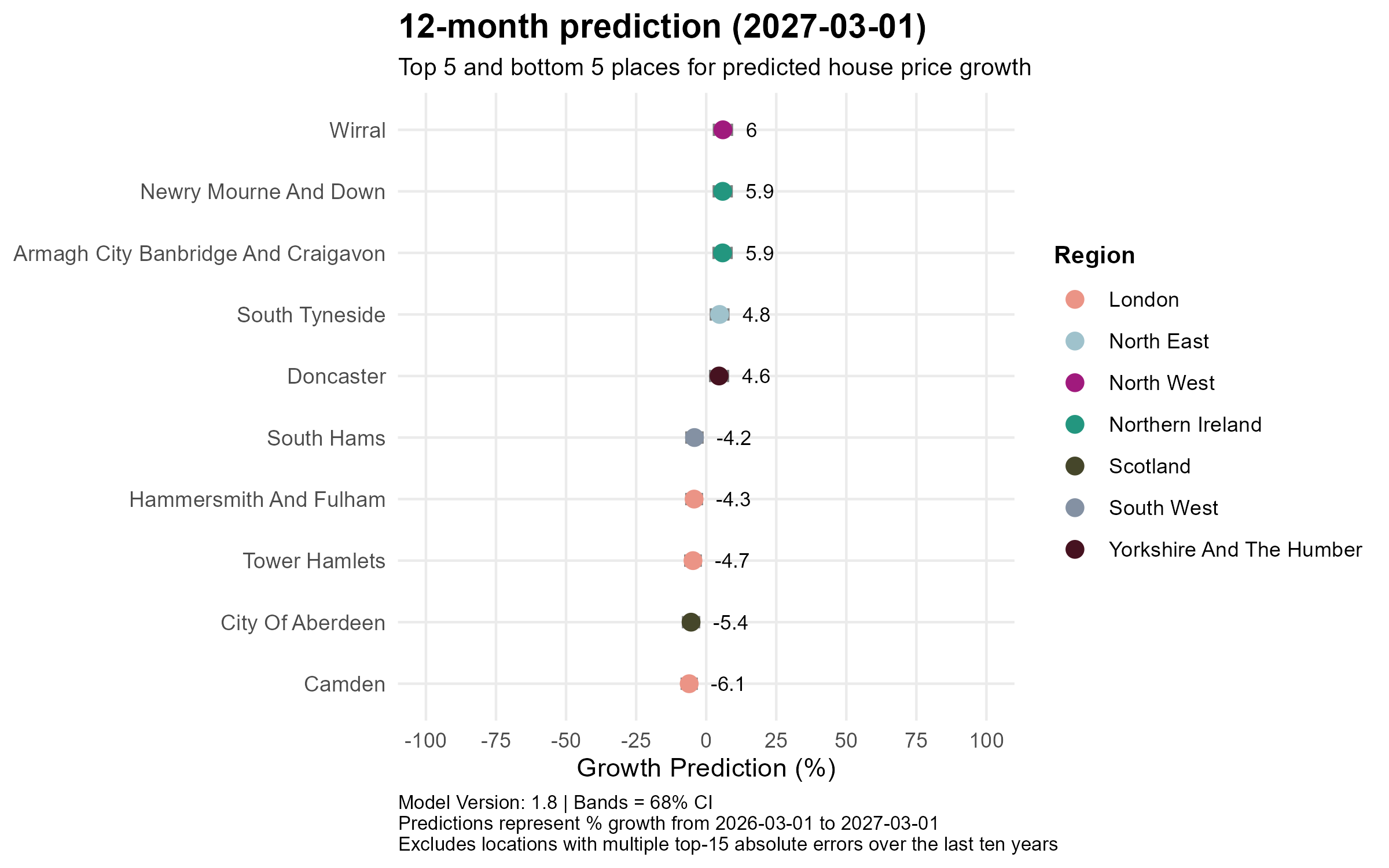

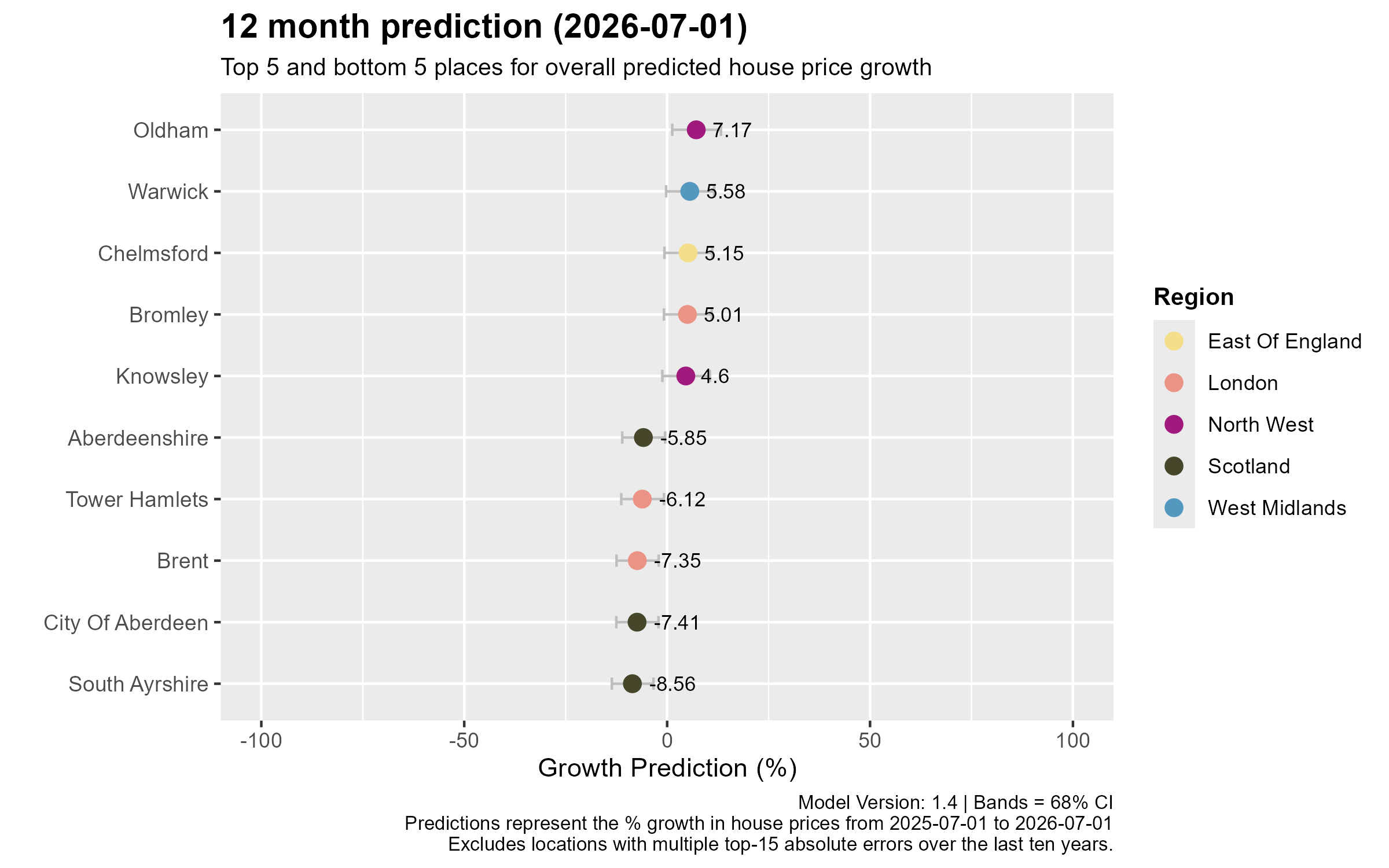

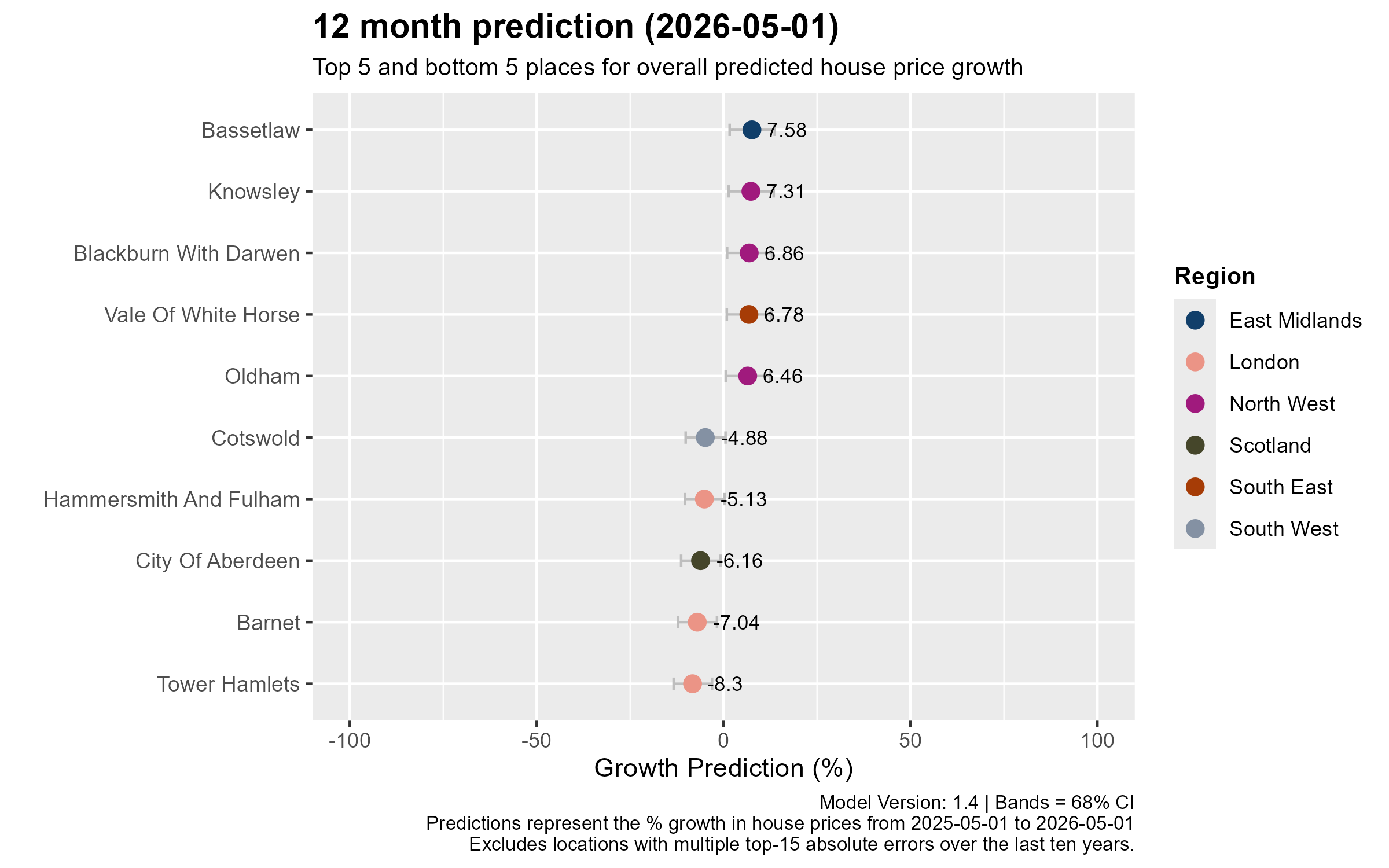

12-month prediction (to May 2027)

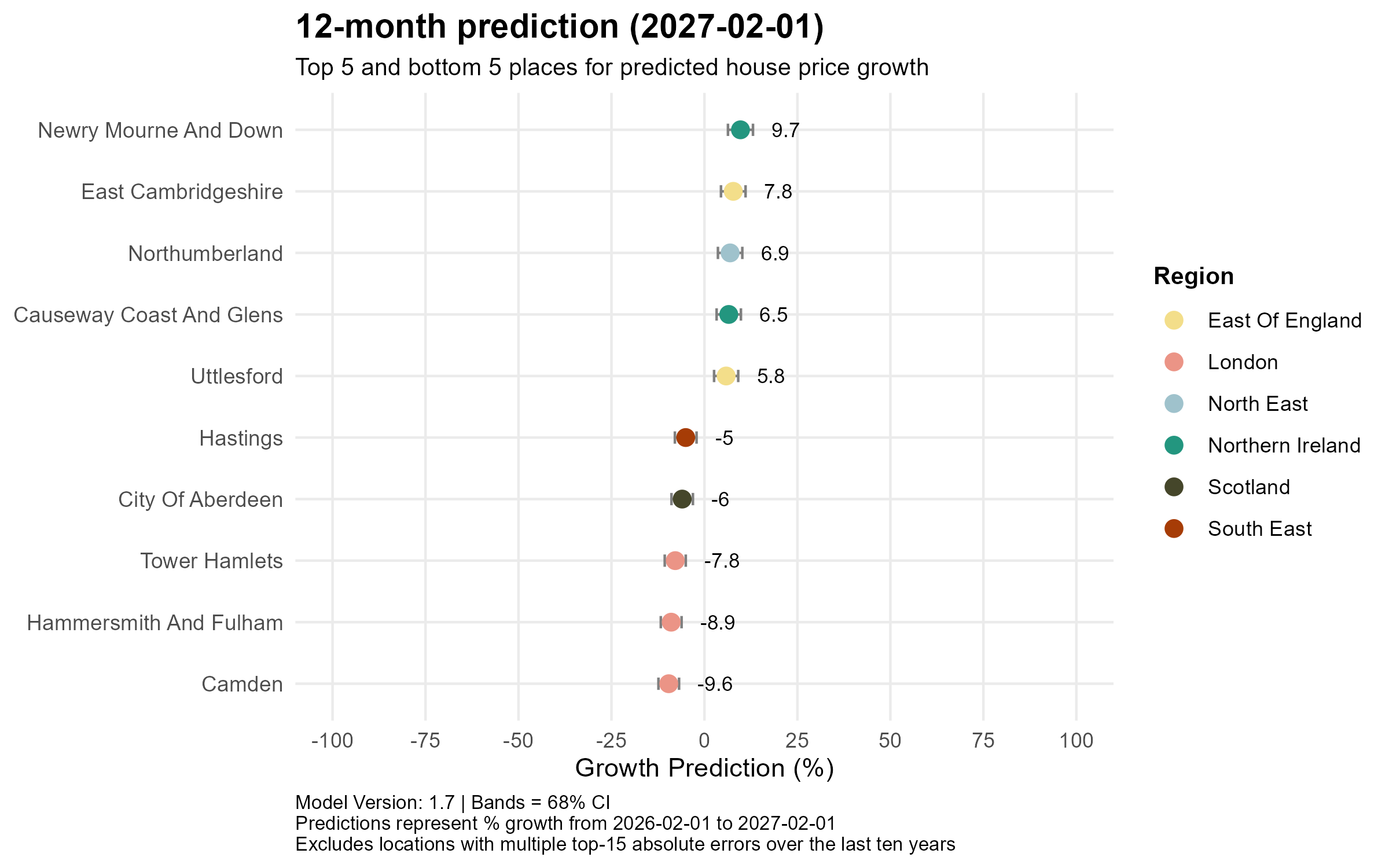

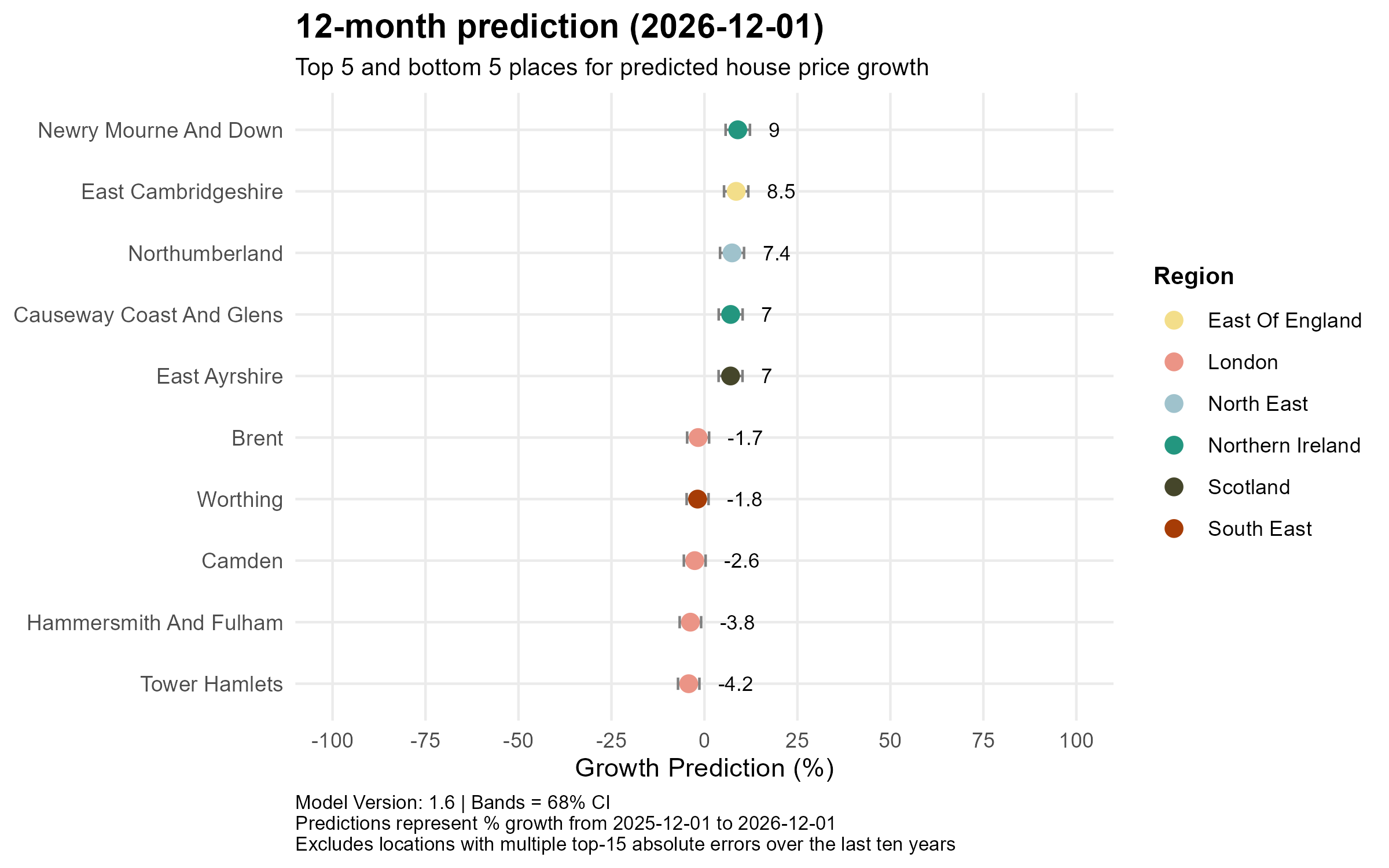

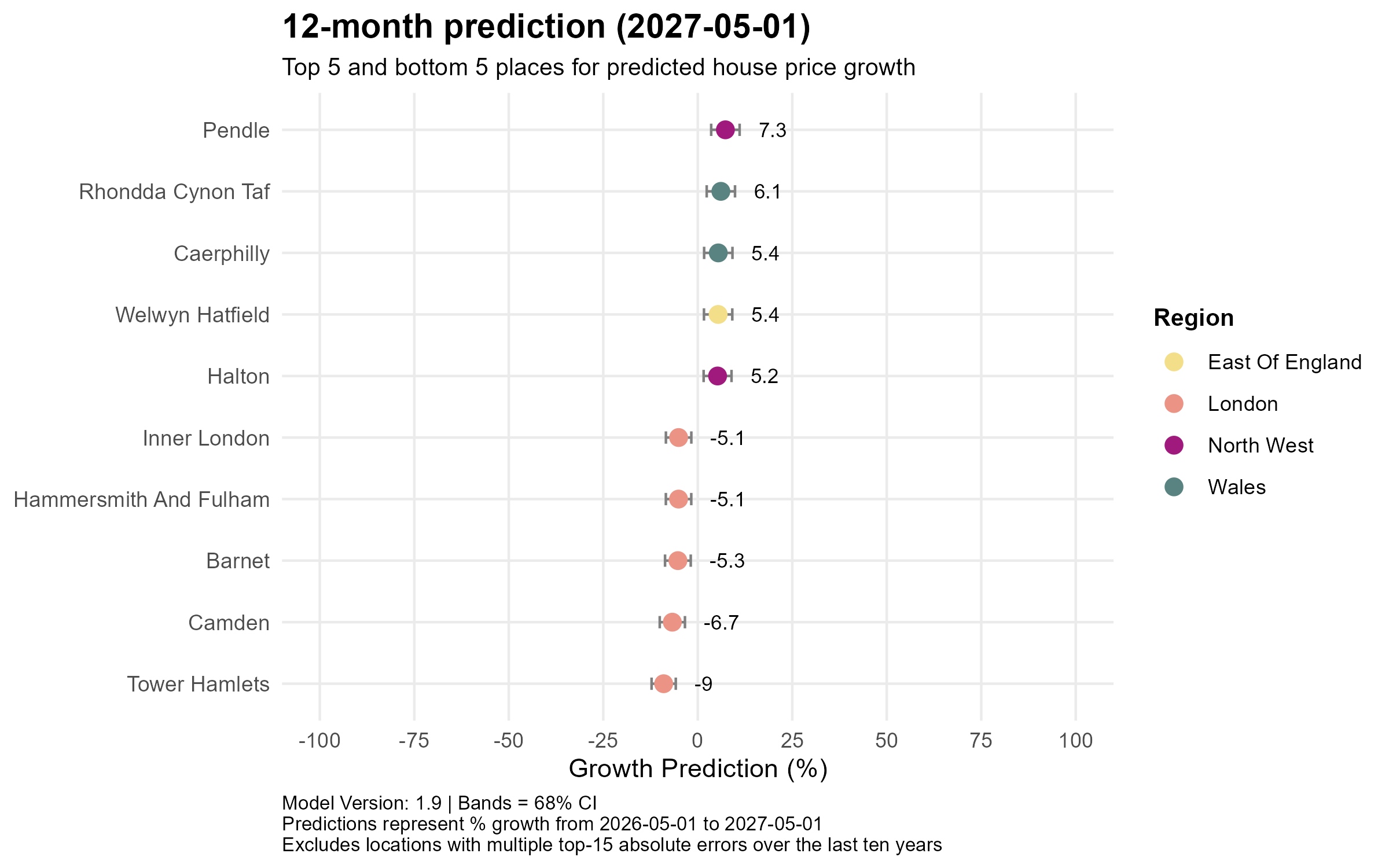

The near-term leaderboard is drawn entirely from the affordable North, Wales and the commuter belt. Pendle in Lancashire leads at +7.3%, followed by Rhondda Cynon Taf (+6.1%) and Caerphilly (+5.4%) in Wales, Welwyn Hatfield in Hertfordshire (+5.4%) and Halton in Cheshire (+5.2%). The bottom five is, unusually, entirely London: Tower Hamlets (−9.0%), Camden (−6.7%), Barnet (−5.3%), Inner London as a whole (−5.1%) and Hammersmith and Fulham (−5.1%) are all expected to fall further before the capital’s correction runs its course.

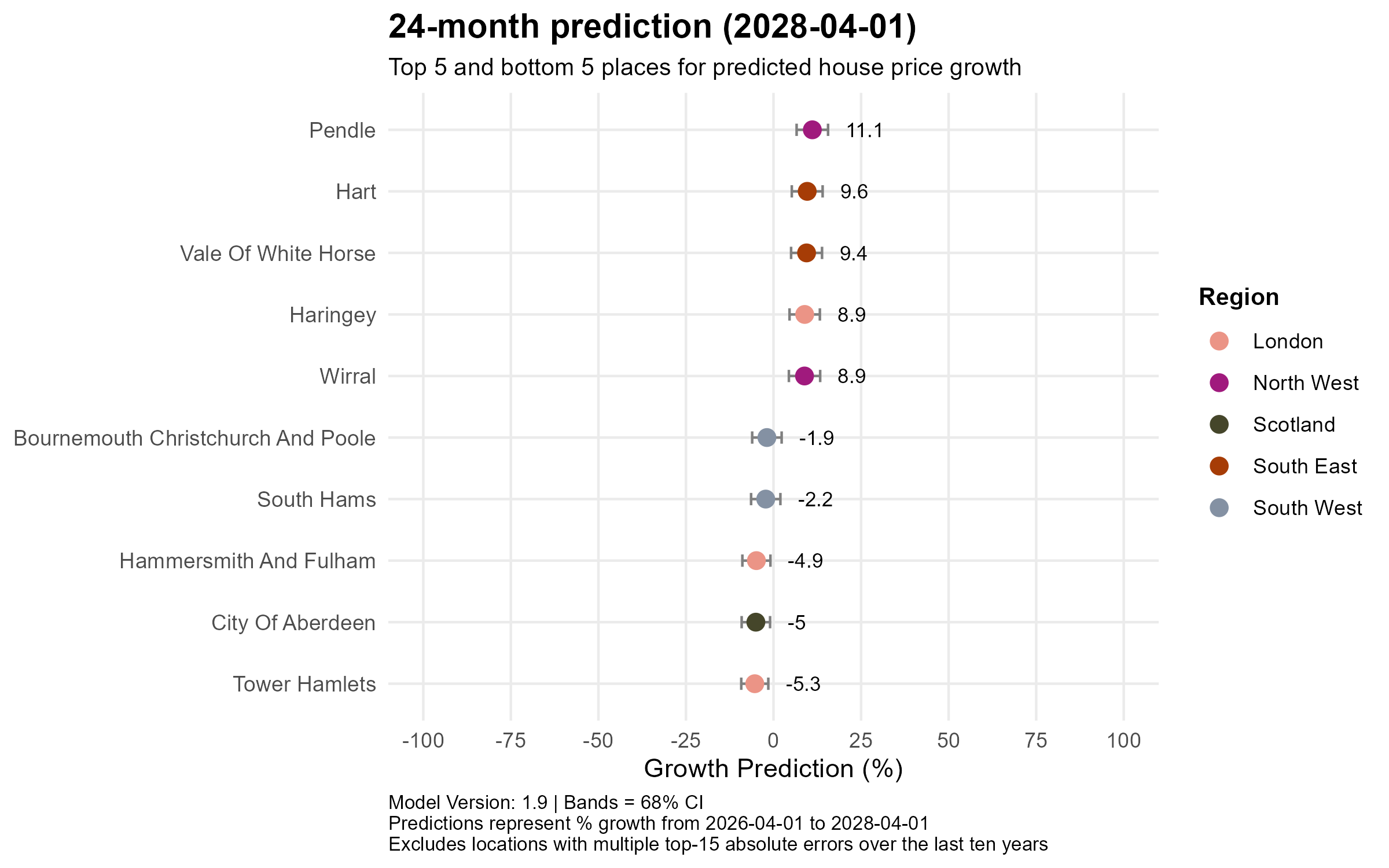

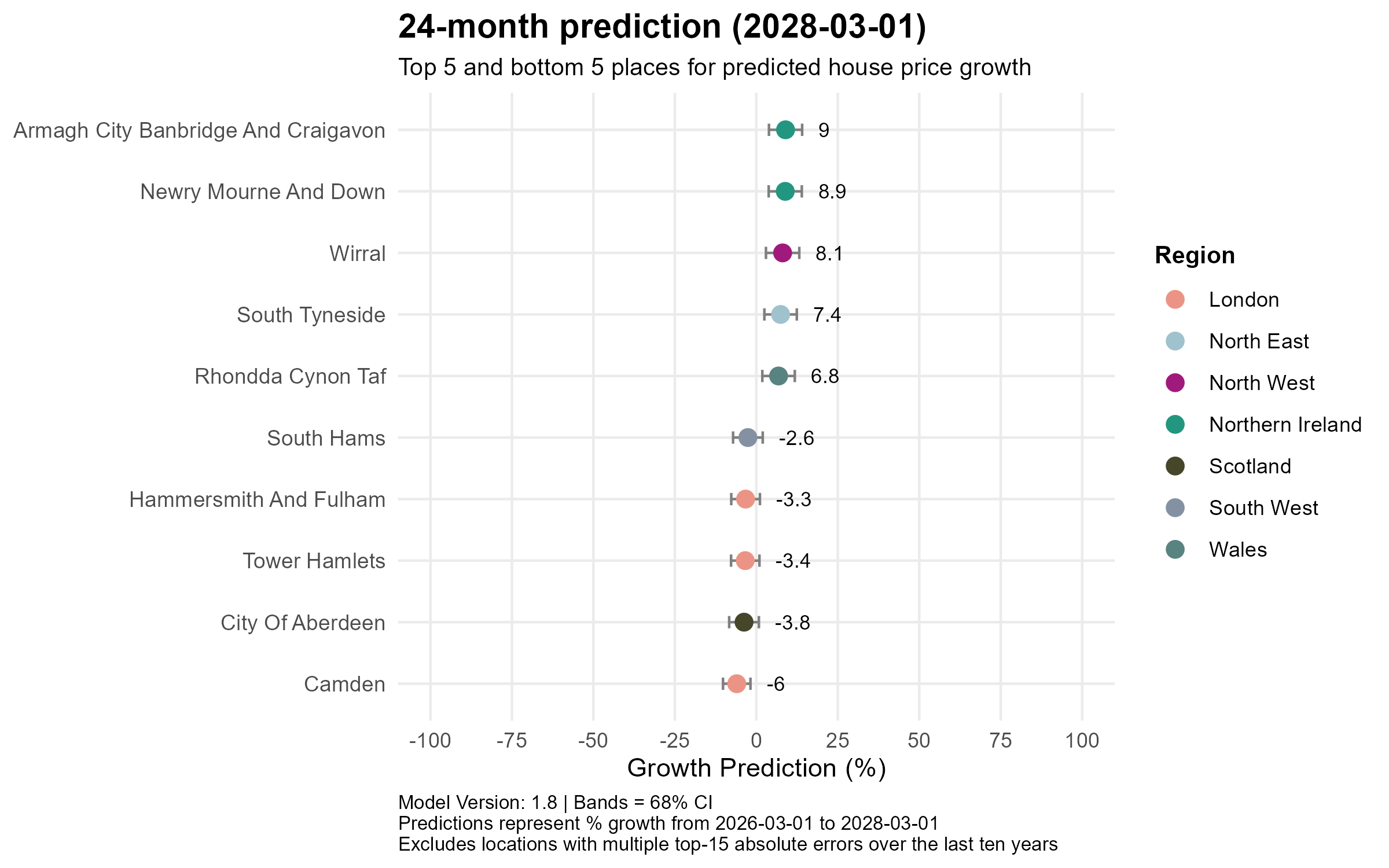

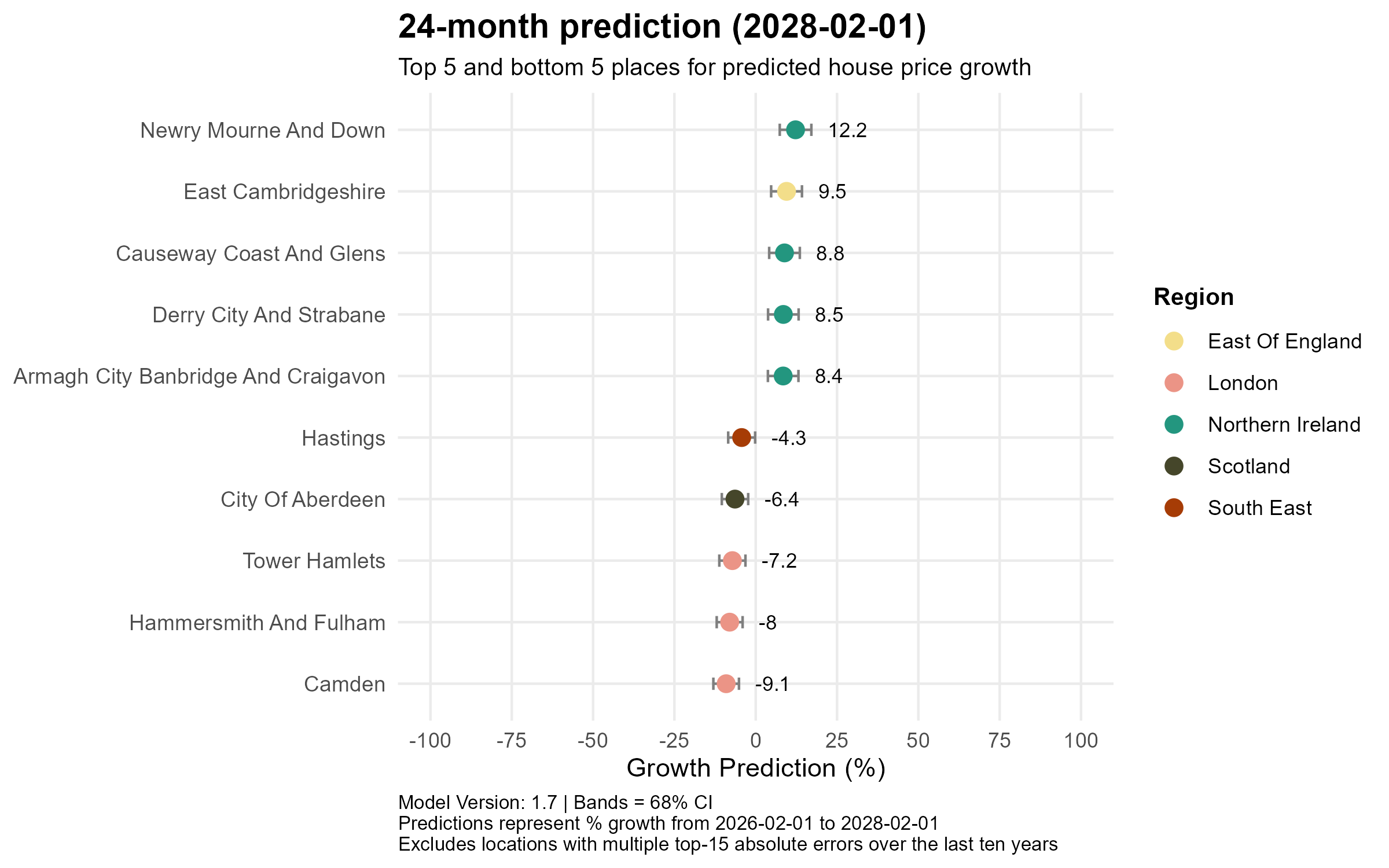

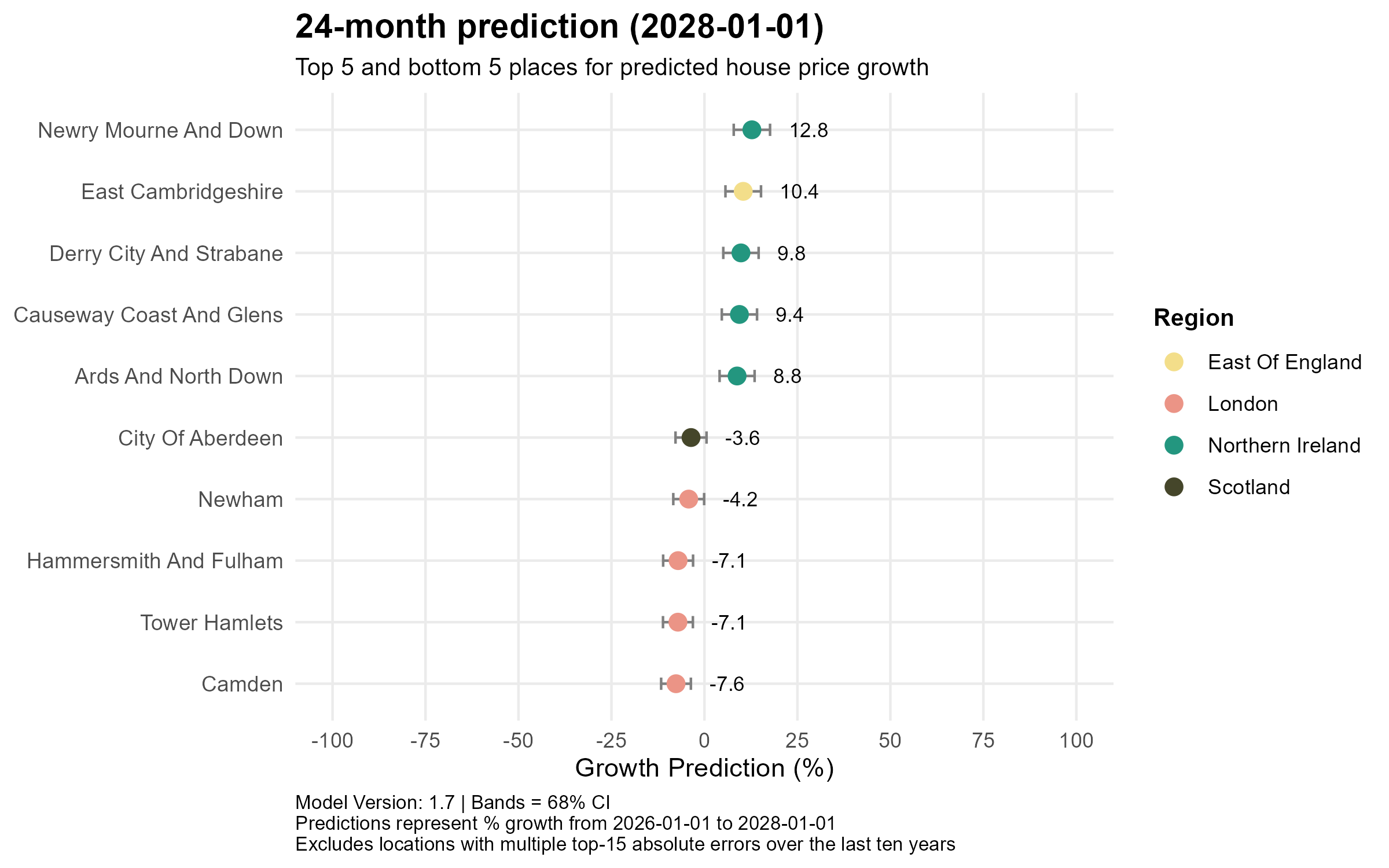

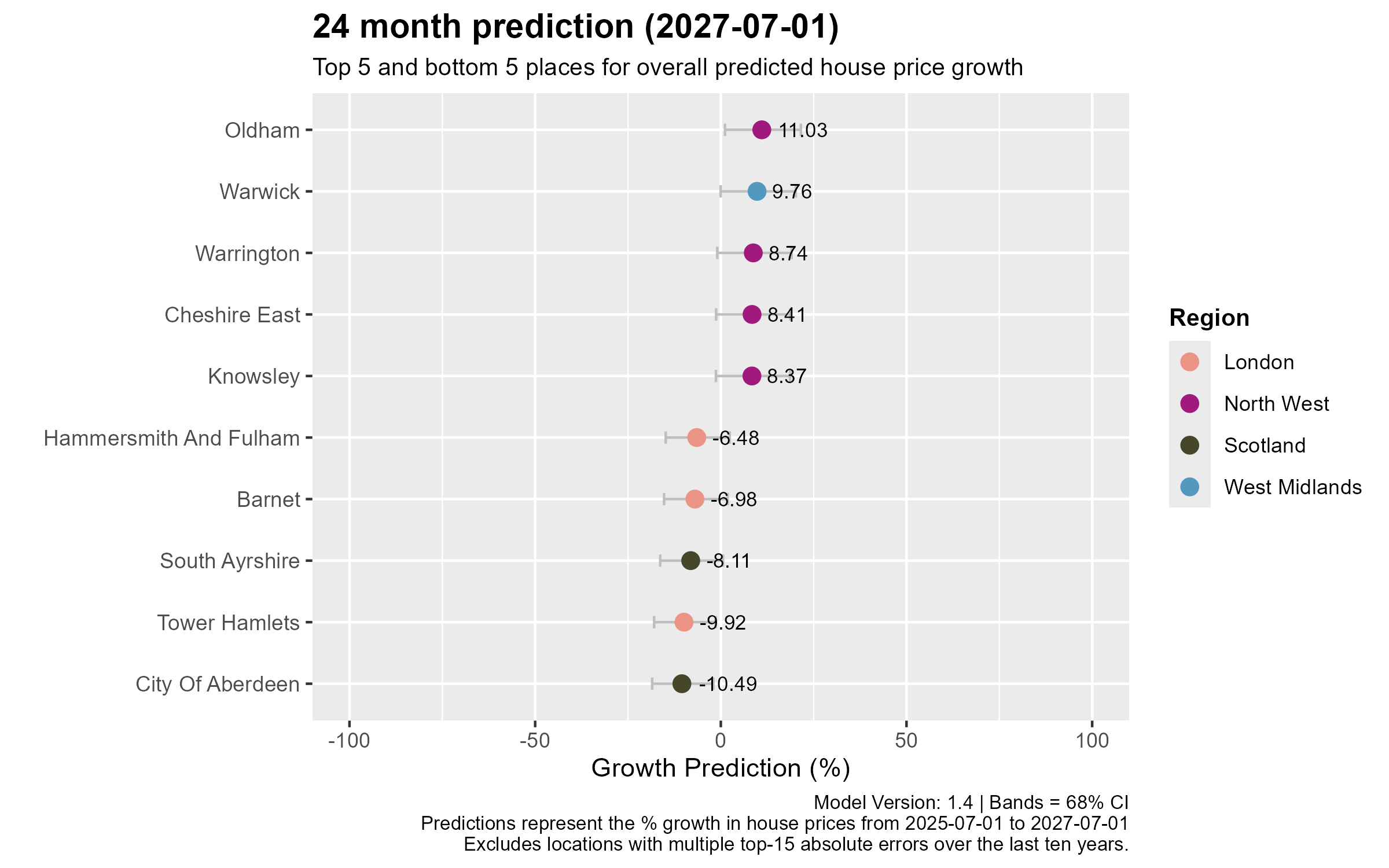

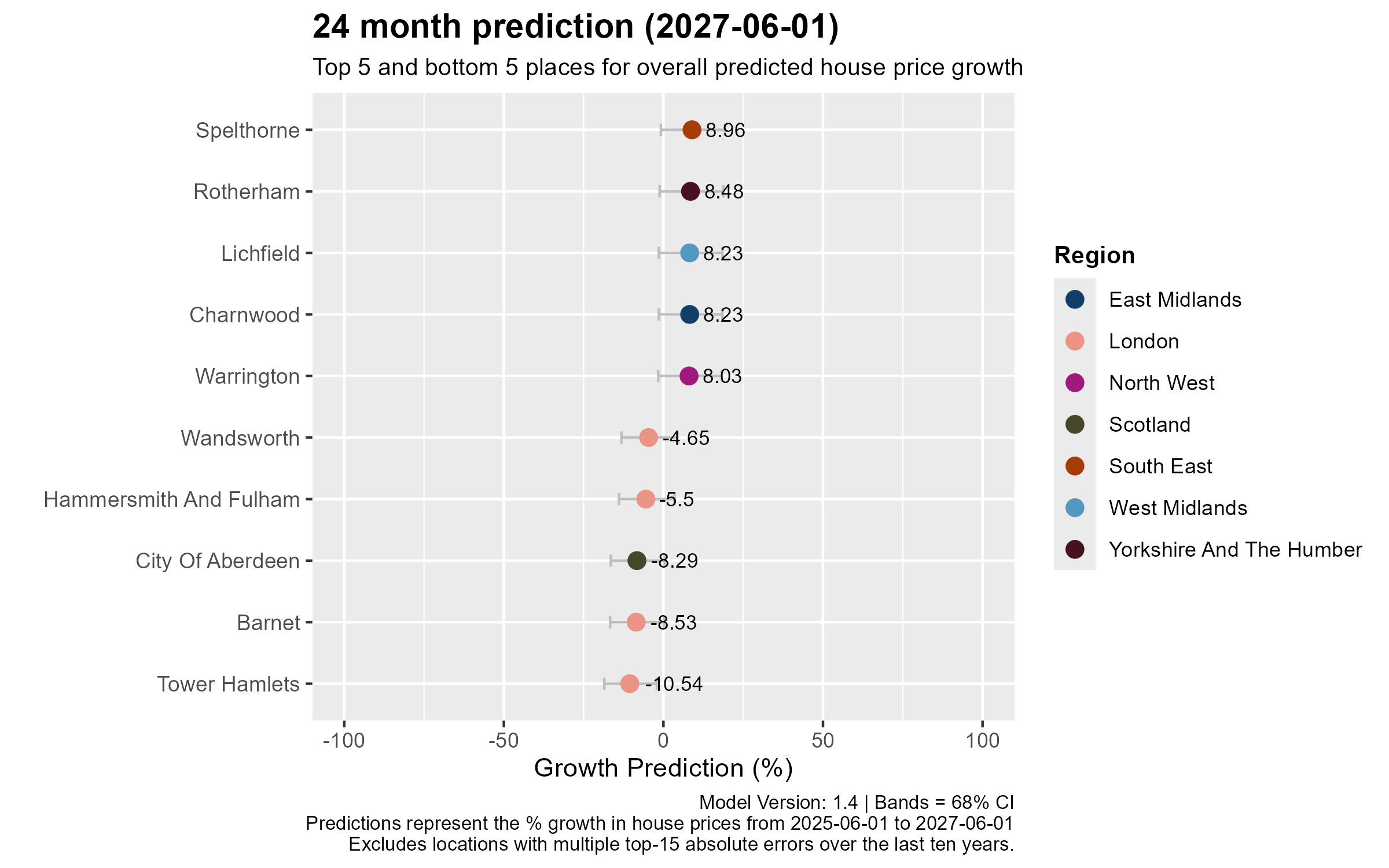

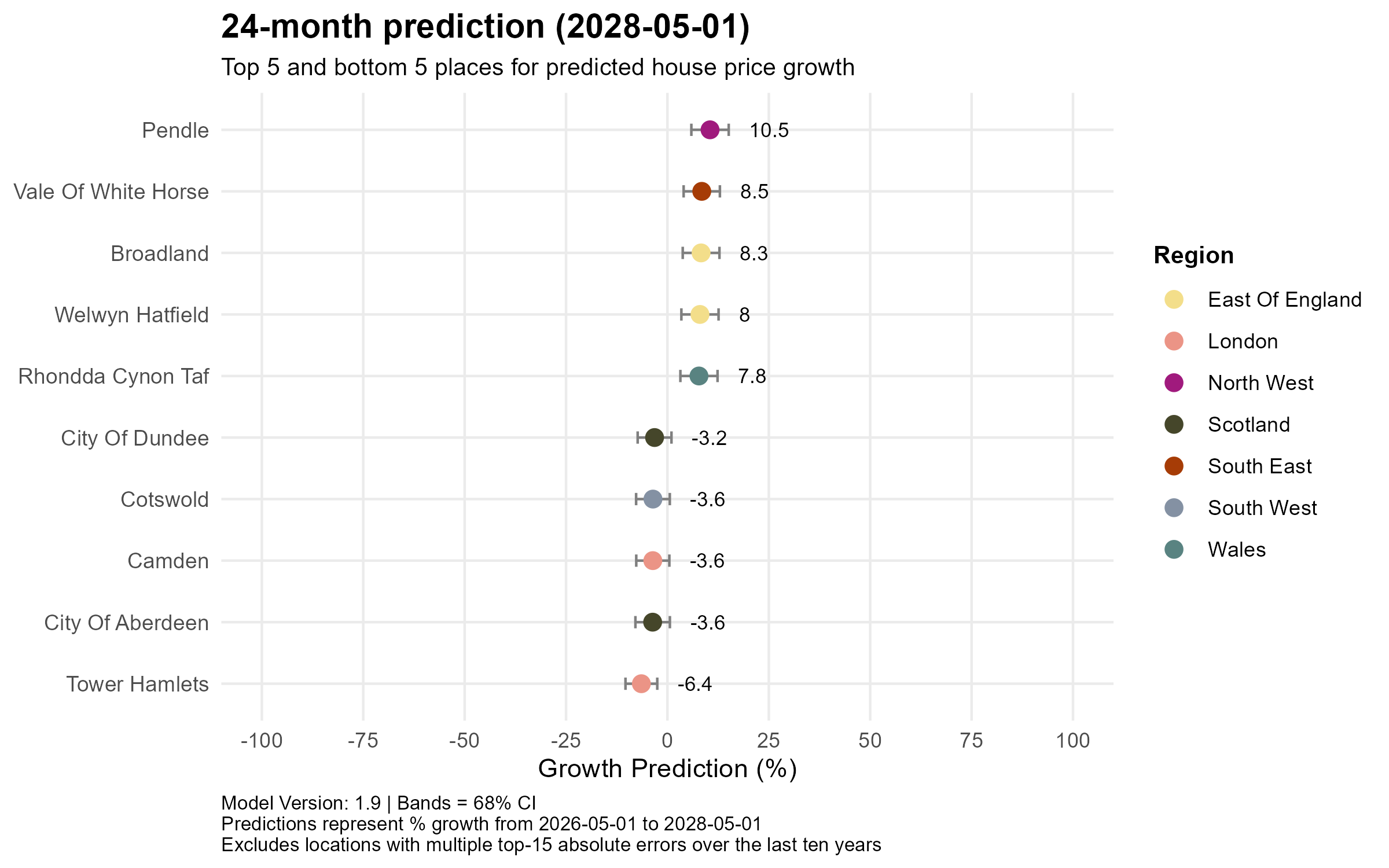

24-month prediction (to May 2028)

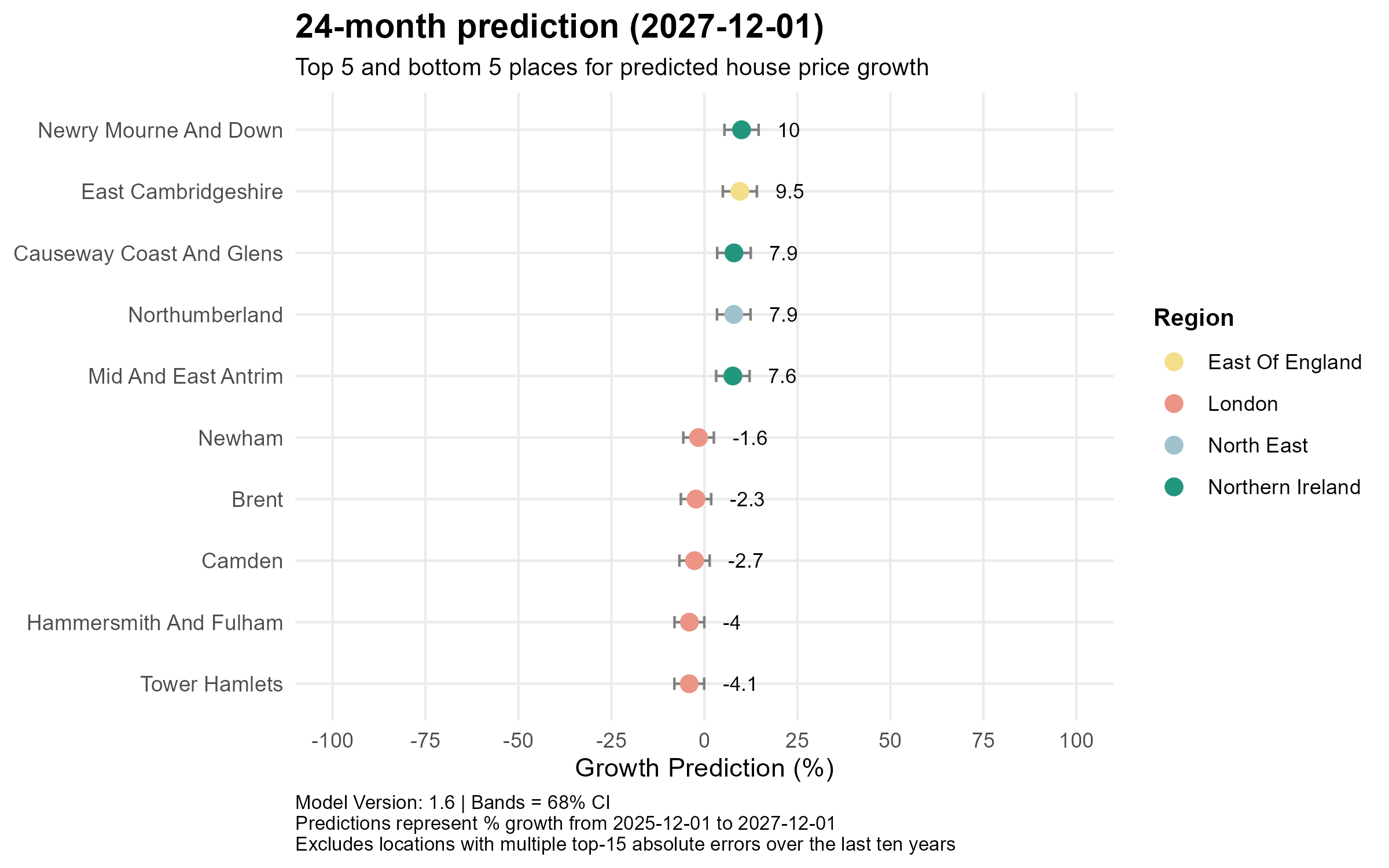

By the two-year horizon the composition shifts towards the South and East. Pendle (+10.5%) still leads, but Vale of White Horse in Oxfordshire (+8.5%), Broadland in Norfolk (+8.3%) and Welwyn Hatfield (+8.0%) climb into the top five alongside Rhondda Cynon Taf (+7.8%). The laggards are moderating rather than deepening: Tower Hamlets (−6.4%) remains the weakest, joined by City of Aberdeen (−3.6%), Camden (−3.6%), Cotswold in Gloucestershire (−3.6%) and City of Dundee (−3.2%) — with Scotland now supplying half the bottom five.

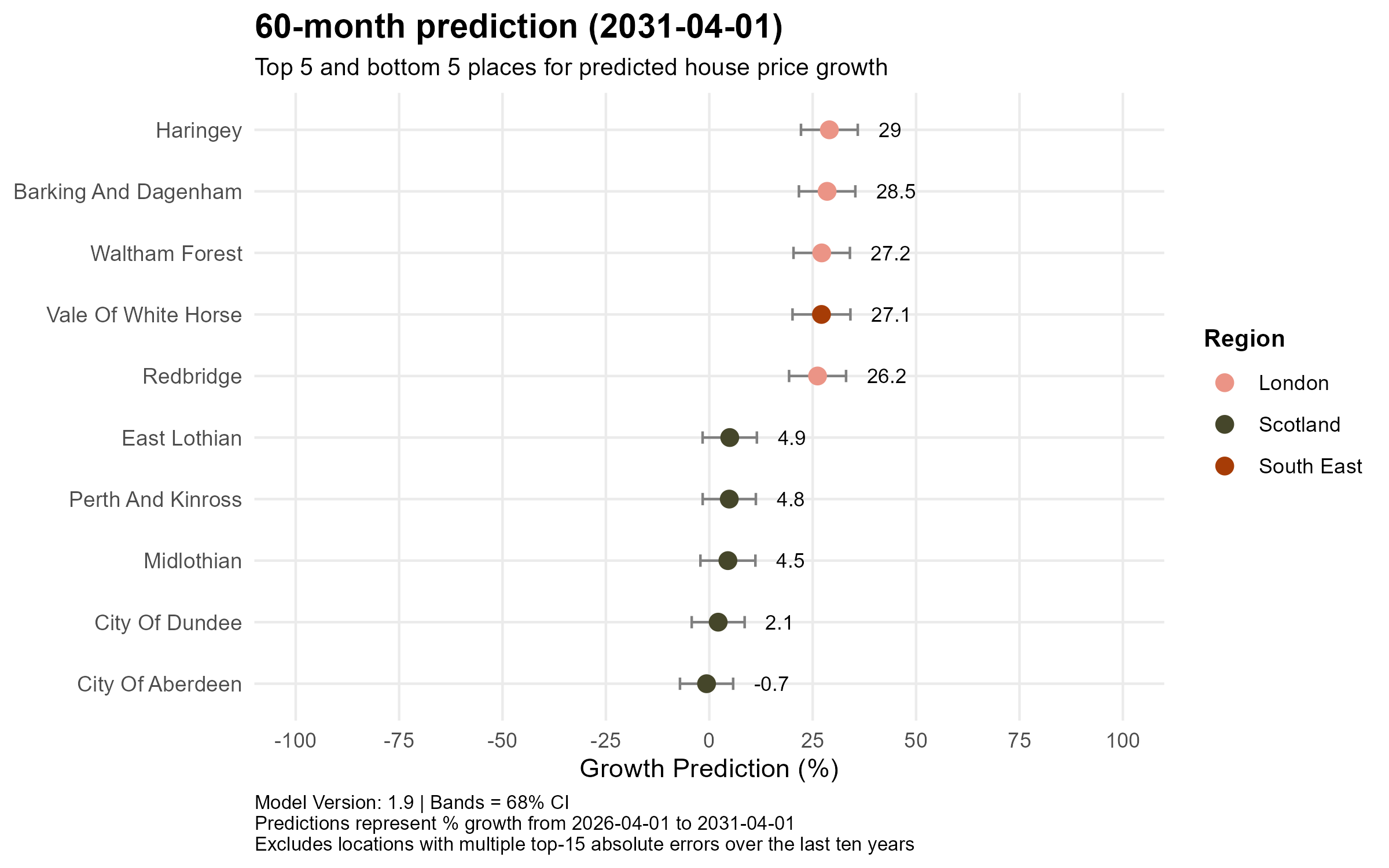

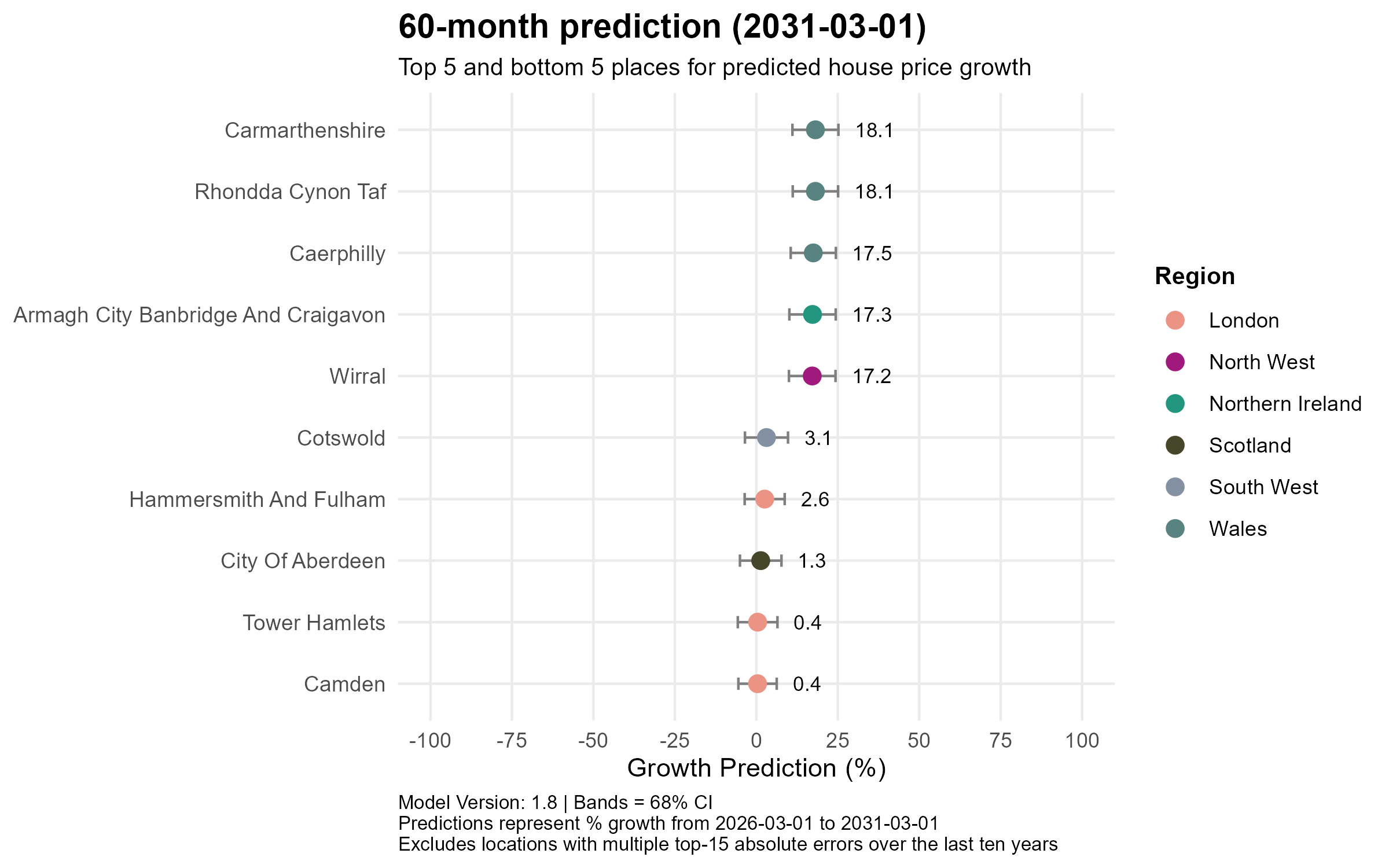

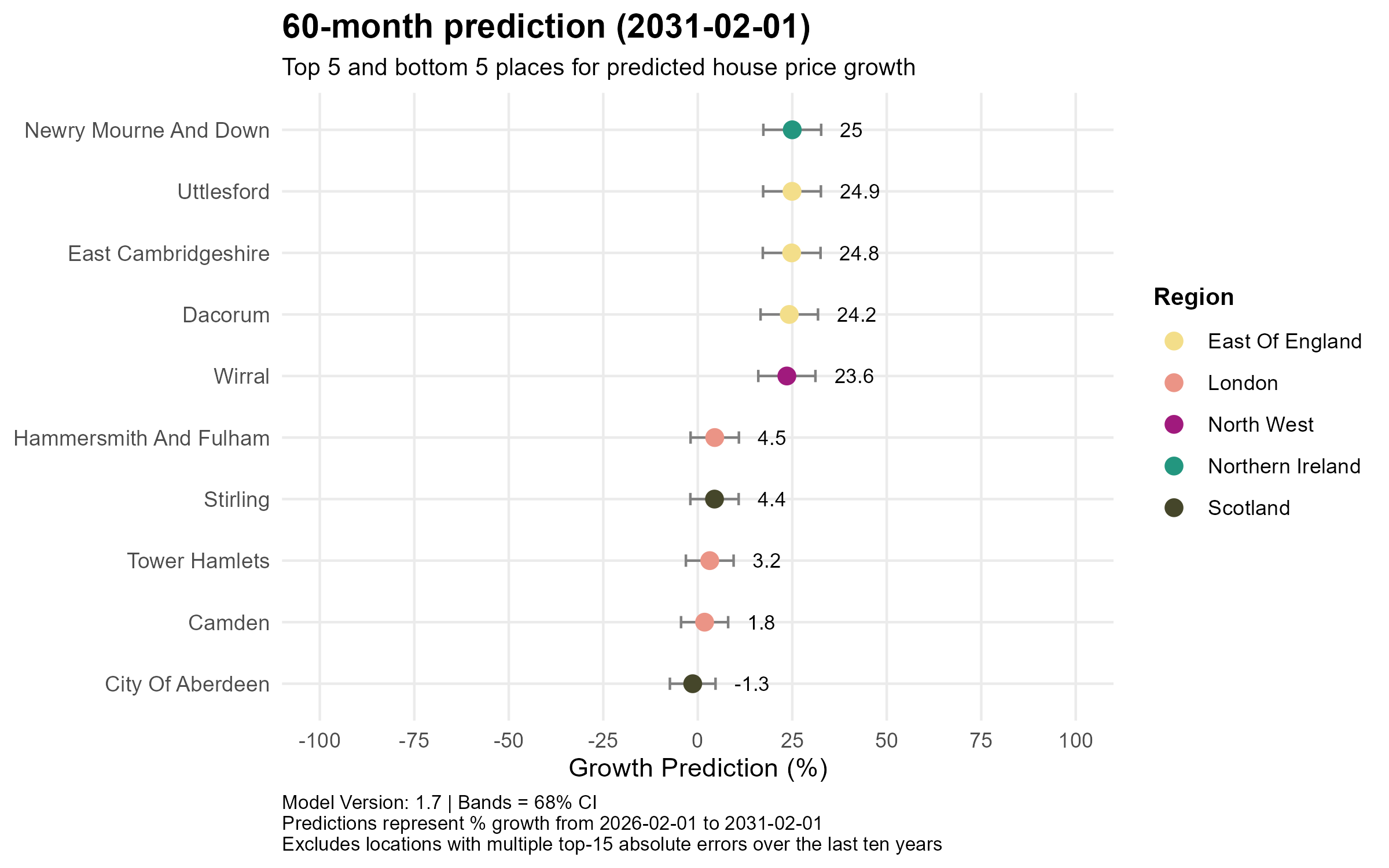

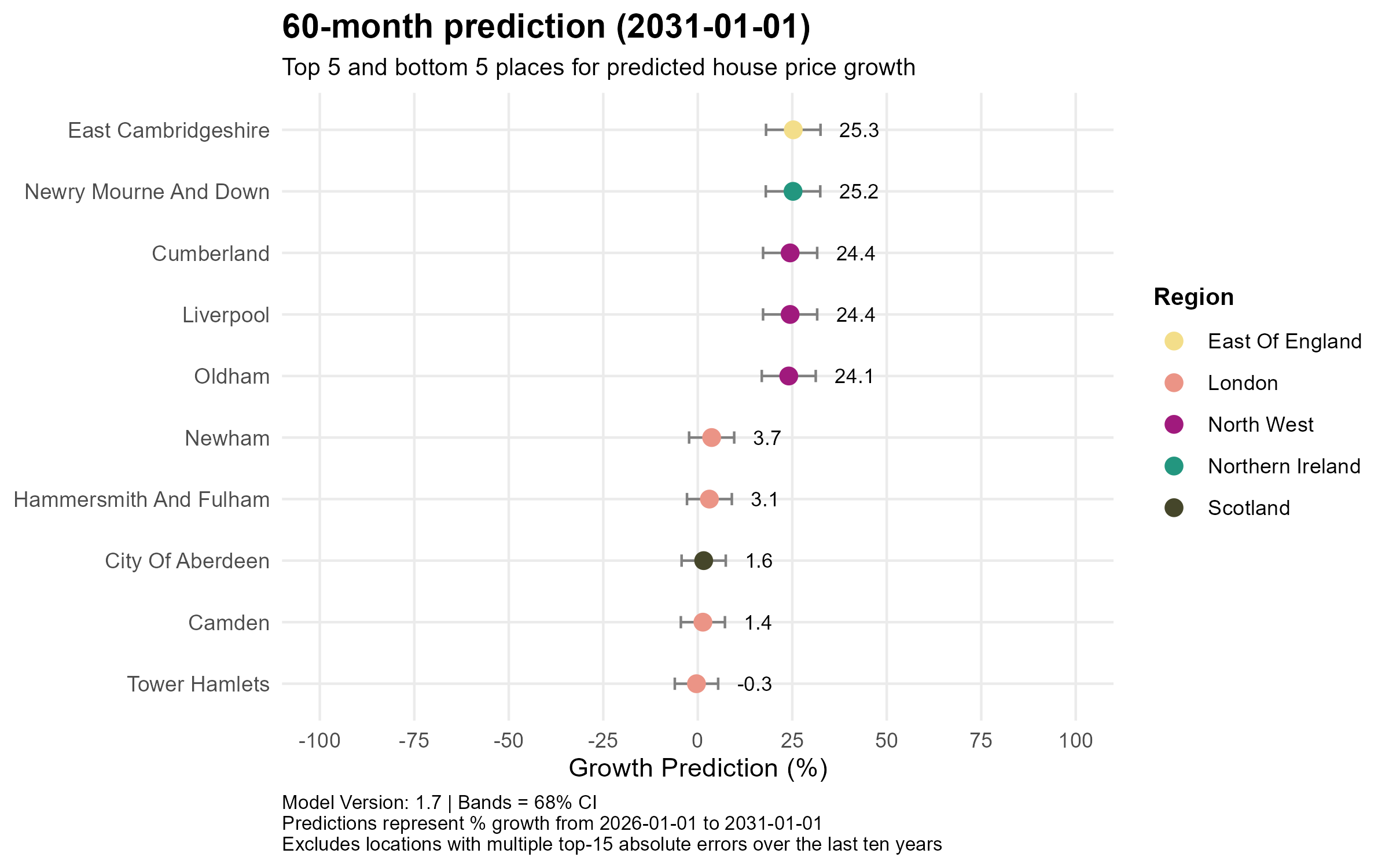

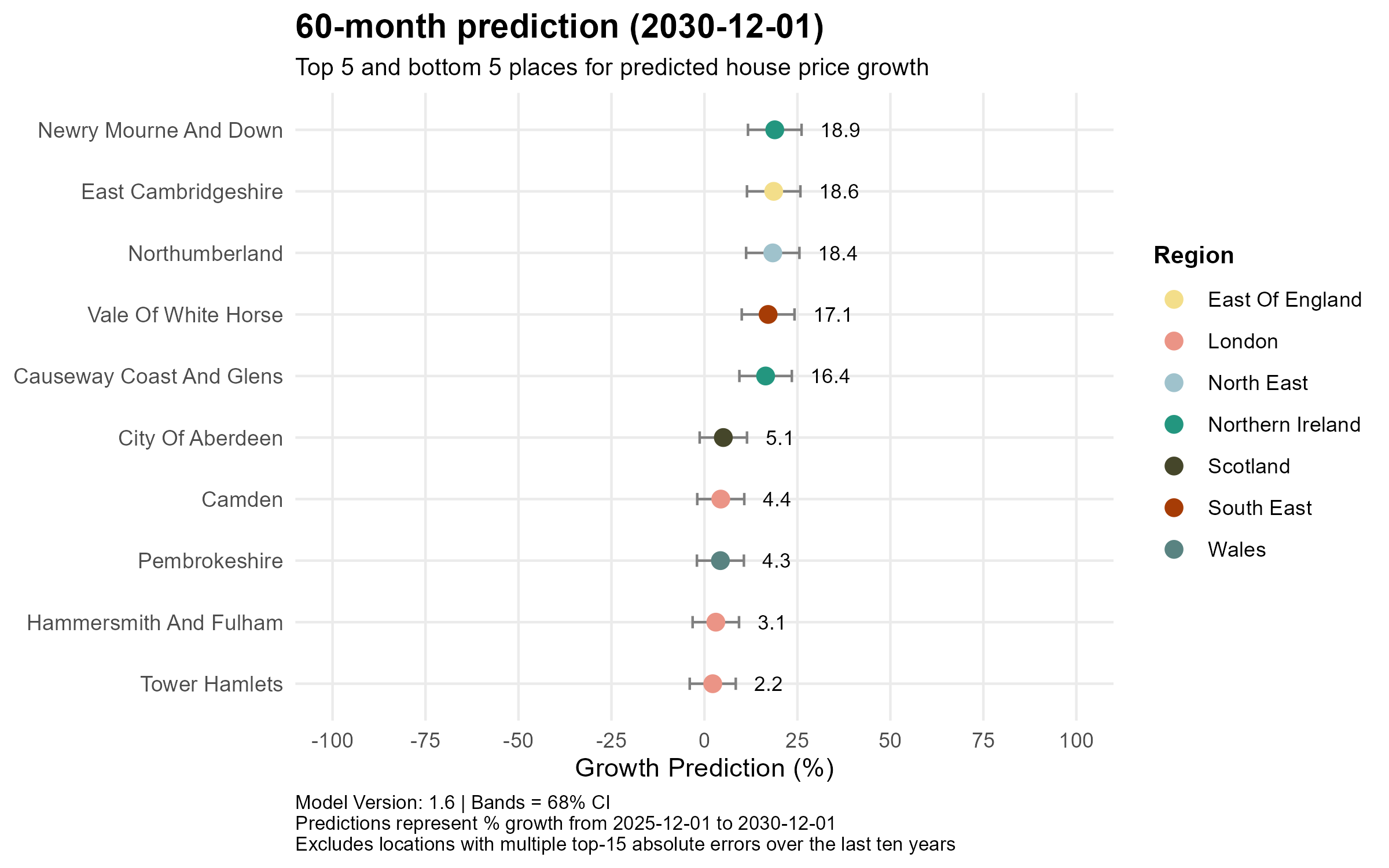

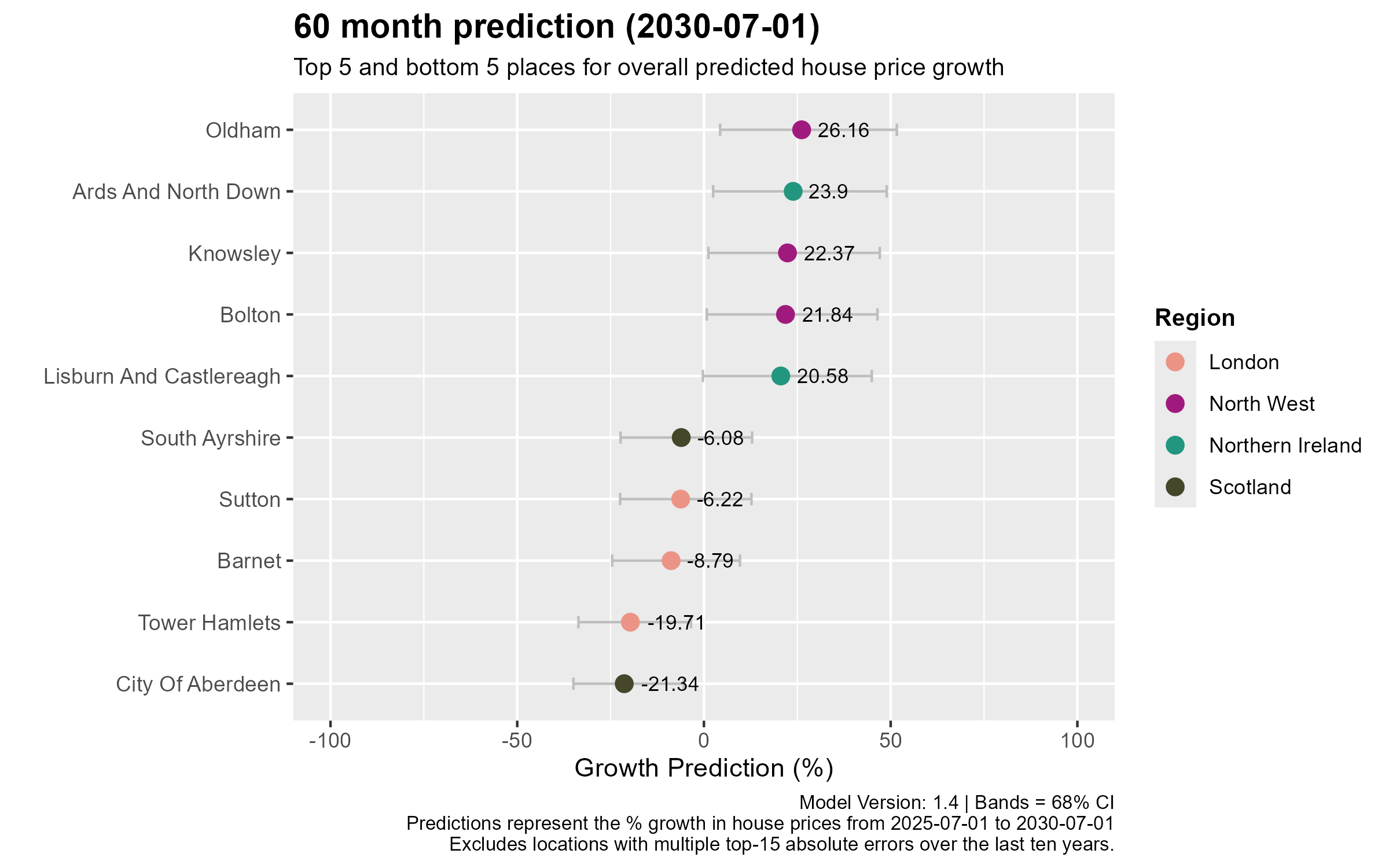

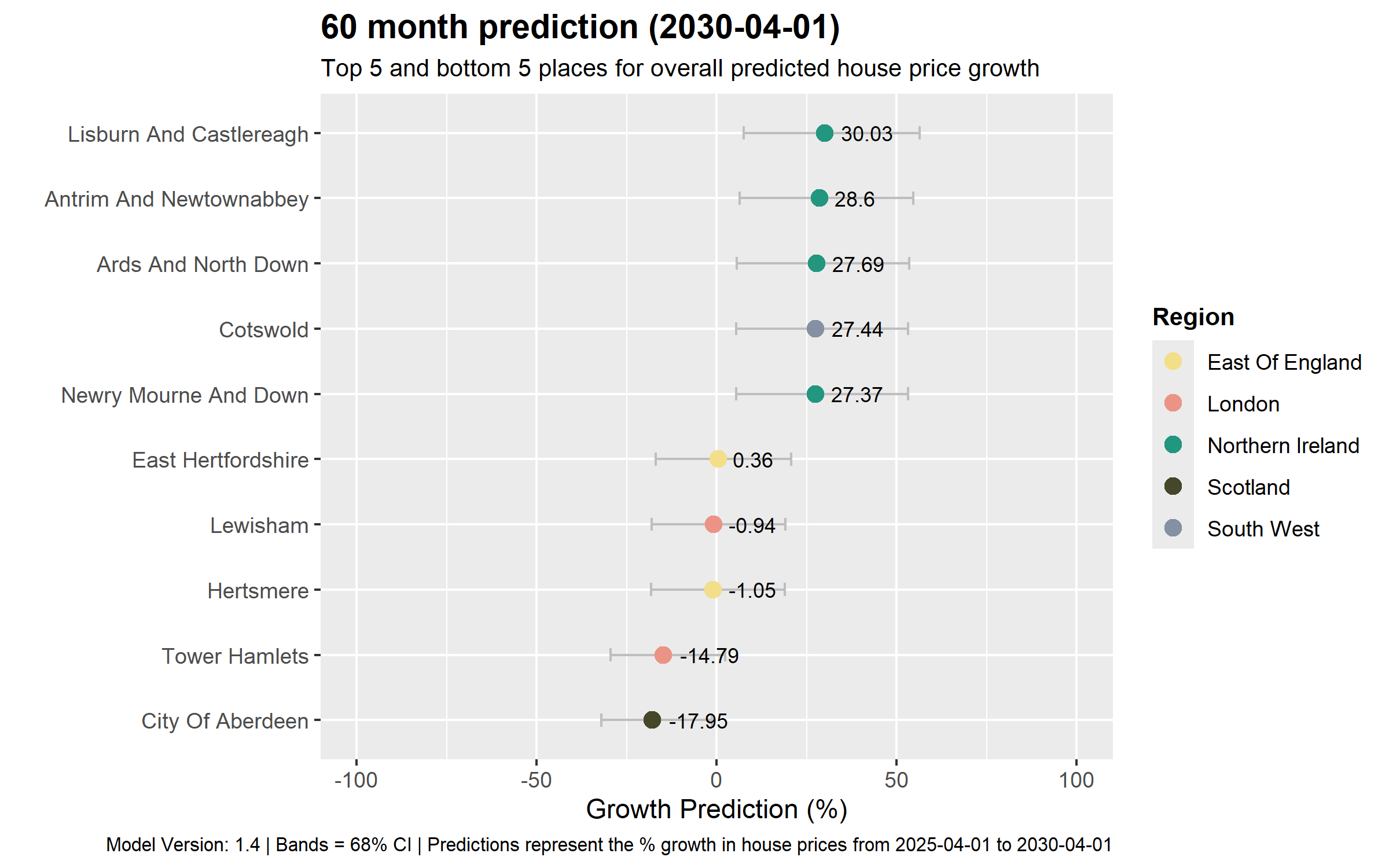

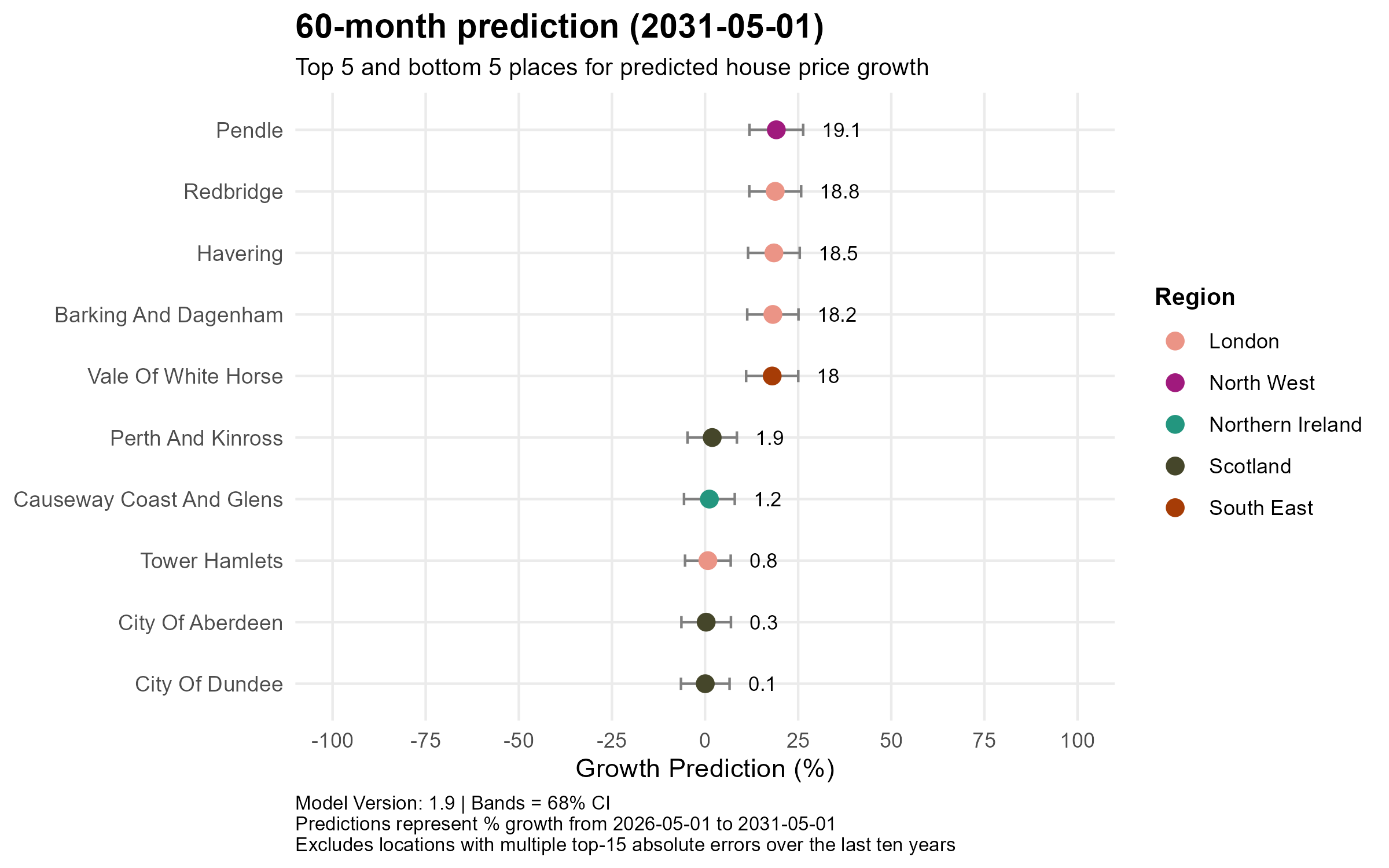

60-month prediction (to May 2031)

The five-year view is a London story with a Lancashire outlier. Pendle just holds the top spot at +19.1%, but three outer London boroughs follow immediately behind — Redbridge (+18.8%), Havering (+18.5%) and Barking and Dagenham (+18.2%) — with Vale of White Horse (+18.0%) rounding out the top five. Crucially, no area is forecast to be negative over the full horizon: the weakest are City of Dundee (+0.1%), City of Aberdeen (+0.3%), Tower Hamlets (+0.8%), Causeway Coast and Glens in Northern Ireland (+1.2%) and Perth and Kinross (+1.9%), confirming that Scotland’s north-east, not London, is the model’s persistent structural laggard.

Conclusion

The rebalancing story now runs in two directions at once. In the here and now the affordable North, Northern Ireland and Wales continue to lead while London and the South East absorb the correction — Tower Hamlets alone is down almost 15% over the year. But from year three onwards the model flips: London and the wider South East top the five-year rankings, the early leaders settle mid-table, and Scotland’s oil-exposed north-east emerges as the only genuinely persistent laggard. As last month’s post noted, the direction of travel is steady rather than dramatic, though the national path has been trimmed to £297k by 2031 — around 9.5% over five years. No boom, and no crash either.