Economic summary

News

In the past month, UK inflation eased slightly, with the Consumer Prices Index rising by 3.4% year-on-year in May, down from 3.5% in April. Meanwhile, the Bank of England held Bank Rate at 4.25% in June following a 25-basis-point cut in May, though policymakers such as Alan Taylor and Andrew Bailey have signalled a cautious path to cuts amid a weakening labour market and global uncertainty. Economic output painted a mixed picture: gross domestic product grew by 0.7% in Q1—the fastest among G7 economies—yet contracted by 0.3% in April, driven largely by a services slowdown. The services sector subsequently rebounded in June, with the PMI rising to 52.8—the strongest growth in ten months—suggesting modest Q2 expansion. Household finances remained under pressure, as real disposable income per head fell by 1% and the savings ratio dropped to 10.9%, offsetting pay growth and dampening spending capacity.

On financial markets, the FTSE 100 hit a record closing high of 8,884.92 on 12 June before easing to 8,805.51 amid fiscal worries and looming tariff deadlines, reflecting investor sensitivity to domestic policy and global trade tensions. Energy bills offered a rare reprieve, with Ofgem cutting the price cap by 7% from July to £1,720 a year for a typical dual-fuel household—a saving of around £129 annually—despite bills remaining elevated compared to pre-crisis levels.

Overall, the UK economy displayed both resilient pockets and persistent headwinds, framing a complex backdrop for the housing market.

Indicators

- Average house prices fell to £265k in June

- Mortgage rates for both 60 % and 95 % LTV mortgages have continued their downward trajectory, now at approximately 4.09 % and 5.09% respectively.

Predictions

Overall

The model suggests only modest nominal growth, with average UK house prices rising from roughly £265k today to about £281k in one year and £288k in two years, before reaching around £303 000 five years out.

Regional

Short-term (1 year): projected first-year gains vary sharply—from barely 0.9 % in London and the South West to around 8.8 % in the North West, 7.9 % in the West Midlands and 7.5 % in the North East—highlighting stronger momentum in more affordable regions. London flats and South West terraces remain the weakest performers sub-1 %, underlining the challenges in already high-priced markets.

Medium-term (3 years): by year three most regions converge into solid double digits—terraced homes in the North West, North East and Yorkshire all exceed 13 %, while overall growth in Wales and the South West also approaches 14–15 %. London, by contrast, still languishes at roughly 2 %, so regional disparities remain pronounced even as growth broadens beyond traditional northern hot spots.

Long-term (5 years): over five years cumulative gains peak at about 21 % in the North West and 20 % in Yorkshire & the Humber, with the North East, Wales and the West Midlands all posting c. 17–18 %. London’s modest 3 % rise underscores that, in the long run, lower-priced regional markets are expected to deliver the most substantial returns.

Local

In the next year, Camden (London) leads growth at around 10.7 %, closely followed by the Cotswolds (South West) at 10.7 % and three Northern Ireland districts – Ards & North Down (9.6 %), Lisburn & Castlereagh (9.5 %) and Antrim & Newtownabbey (9.2 %). At the other extreme, Hackney (London 0.4 %), Surrey (South East 0.0 %), Hertsmere (East of England –0.2 %), Elmbridge (South East –0.9 %) and the City of Aberdeen (Scotland –1.0 %) are forecast flat or in slight decline. This wide split highlights brisk demand in undervalued rural and Northern Irish markets versus very modest near-term prospects for certain expensive urban and commuter-belt locations.

By April 2027 the Cotswolds (South West) again tops the chart at about 15.1 %, with four Northern Ireland councils (Ards & North Down 14.2 %, Lisburn & Castlereagh 14.0 %, Antrim & Newtownabbey 13.7 %, Newry, Mourne & Down 12.9 %) close behind. In contrast, core London boroughs – City of Westminster (–1.6 %), Southwark (–1.8 %) and Tower Hamlets (–4.9 %) – together with Elmbridge (–1.9 %) and Aberdeen (–5.9 %) fall into negative territory. The roughly 20 percentage-point gap between top and bottom underscores a sustained divergence between buoyant peripheral markets and cooling prime city and commuter zones.

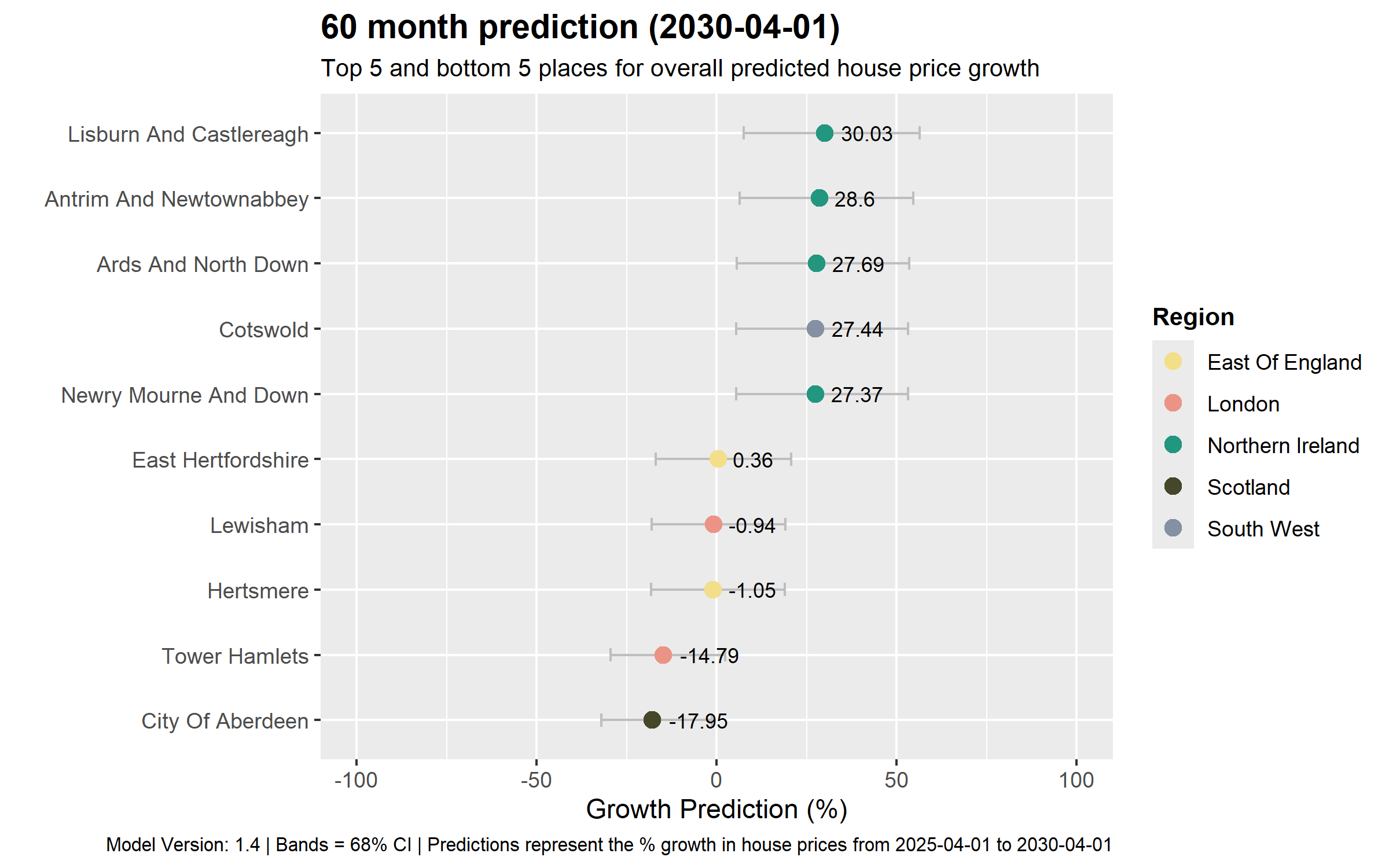

Over five years Northern Ireland districts dominate: Lisburn & Castlereagh leads at 30.0 %, followed by Antrim & Newtownabbey 28.6 %, Ards & North Down 27.7 % and Newry, Mourne & Down 27.4 %, with the Cotswolds (South West) also posting 27.4 %. At the bottom, East Hertfordshire (East of England +0.4 %), Lewisham (London –0.9 %), Hertsmere (East of England –1.1 %), Tower Hamlets (London –14.8 %) and Aberdeen (Scotland –17.9 %) show minimal to steep declines. The nearly 50 percentage-point gulf highlights a long-term realignment in favour of more affordable or recovering regions over high-price urban centres.

Conclusion

Taken together, these forecasts paint a picture of an increasingly bifurcated UK housing market, in which long-run gains are concentrated in undervalued and non-urban districts—especially in Northern Ireland and certain South West rural areas—while many high-priced London boroughs and southern commuter belts struggle to keep pace, or even register small falls. In the short term, Camden and the Cotswolds outshine most regions with double-digit growth, but by year two and beyond the top spots are dominated by Northern Irish councils posting mid-teens to low-thirties-percent gains over five years. Meanwhile, places such as Tower Hamlets, Aberdeen and parts of the South East show flat or negative returns, reinforcing the scale of regional divergence. For buyers and investors, this underscores the importance of looking beyond traditional city hotspots: peripheral and lower-cost markets offer the strongest compounded returns, whereas prime urban locations may underperform or deliver only modest uplift.

Leave a comment